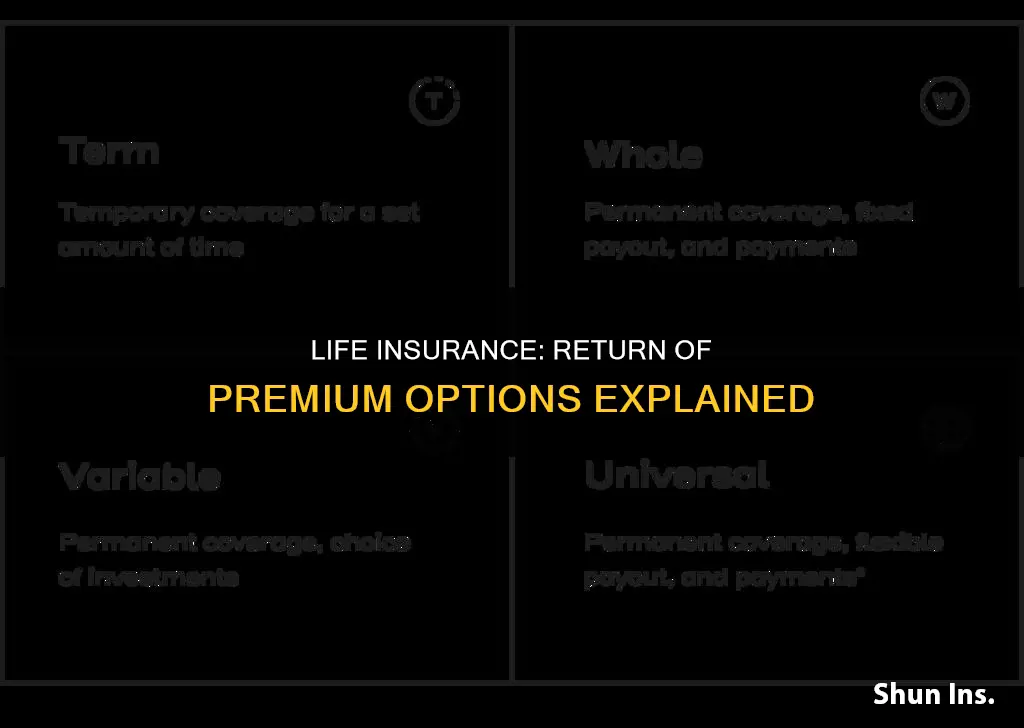

Return of premium (ROP) life insurance is a type of term life insurance that allows you to claim back your premium payments if you outlive the term of your policy. This type of policy is more expensive than traditional term life insurance, as the insurance company must refund the premiums at the end of the term if no claim is made. ROP policies can be attractive to those who want the security of life insurance with the potential to get their money back if they outlive the term.

| Characteristics | Values |

|---|---|

| Type | Term life insurance |

| Coverage period | 5, 10, 20, 30 years |

| Premium refund | Full or partial |

| Tax on refund | None |

| Premium refund conditions | Outlive the policy term |

| Premium refund timing | End of term |

| Premium refund format | Lump sum |

| Premium refund eligibility | Policyholder only |

| Premium refund eligibility conditions | Active policy |

| Premium refund eligibility conditions | On-time premium payments |

| Premium refund eligibility conditions | Policy not cancelled early |

Explore related products

![Report Of The Royal Commission On Life Insurance [and Supplementary Return]](https://m.media-amazon.com/images/I/51KUkhWivPL._AC_UY218_.jpg)

What You'll Learn

- Return of premium life insurance is a type of term life insurance that allows you to collect your premium payments if you outlive your selected term

- Return of premium life insurance functions as a savings account with a bonus life insurance add-on

- Returns generated from this type of plan are generally not taxed

- Return of premium life insurance is more expensive than a traditional term life insurance plan

- You can receive a refund of some or all of your premium payments

![]()

Return of premium life insurance is a type of term life insurance that allows you to collect your premium payments if you outlive your selected term

Return of premium (ROP) life insurance is a type of term life insurance that allows you to reclaim your premium payments if you outlive the length of your policy. This type of policy is more expensive than traditional term life insurance, as the additional cost covers the insurance company's promise to refund your premium payments.

With ROP life insurance, you can expect to pay higher monthly premiums to keep your policy active. If you pass away within the coverage period, your beneficiaries will receive the death benefit, as with a standard term policy. However, if you outlive the term, you will be refunded either all or some of the money you spent on premium payments. This refund is typically tax-free, although it may not include fees and other riders on the policy.

The length of the term can vary, with common options including 15, 20, or 30 years of coverage. At the end of the term, the policy expires, and the policyholder may renew or convert it into another type of life insurance policy. If no action is taken, the coverage ends.

The main advantage of ROP life insurance is the ability to reclaim past premium payments. This can be particularly beneficial if you have new expenditures to cover later in life, such as a mortgage or retirement plan. ROP life insurance can function as a savings account, providing financial peace of mind.

However, there are also disadvantages to consider. The cost of ROP life insurance is significantly higher than traditional term life insurance. You may be better off purchasing a less expensive traditional policy and investing the difference. Additionally, if you allow your policy to lapse or cancel it early, you will likely not receive a refund of your premiums.

Ultimately, the decision to choose ROP life insurance depends on your financial situation and goals. It offers the advantage of a guaranteed payout if you outlive the term, but it comes with higher premiums. It is important to carefully consider the pros and cons and consult with a financial advisor before making a decision.

Selling P&C and Life Insurance: Can You Do Both?

You may want to see also

Explore related products

![]()

Return of premium life insurance functions as a savings account with a bonus life insurance add-on

Return of premium (ROP) life insurance is a type of term life insurance that allows you to collect your premium payments if you outlive your selected term. This type of insurance plan can be more expensive than a traditional term life insurance plan.

In a standard term life insurance plan, premium payments are usually non-refundable and owned by the insurance company. However, in a return of premium life insurance plan, you may be able to recover these payments if you outlive your policy term. For example, if you buy a 20-year return of premium term life insurance plan and survive the 20-year term, you will be able to get a refund of your premium payments.

The biggest pro of return of premium life insurance is the ability to reclaim past premium payments. If you outlive your term, you will typically receive a lump-sum payment combining all previous premiums that were paid. This can be particularly helpful if you have new expenditures to cover later in life, such as a mortgage or retirement plan. In this respect, return of premium life insurance can function as a savings account with a bonus life insurance add-on. Additionally, any returns generated from this type of plan generally won't be taxed, so you may be able to receive your lump-sum premium payment tax-free.

However, there are also some cons to return of premium life insurance. One of the biggest cons is the cost. Return of premium life insurance is usually much more expensive than traditional term life insurance. You may be able to get some or all of your money back, but you will have to budget for higher premiums. If you cannot afford a costly policy, this might not be a good option for you.

Another thing to consider is that if you allow your policy to lapse or you cancel this type of policy early, you likely won't receive a refund of your premiums. Additionally, premium refunds typically don't include the money paid for riders or any additional fees.

Selling Life Insurance in Canada: Is It Possible?

You may want to see also

Explore related products

![]()

Returns generated from this type of plan are generally not taxed

In most cases, money paid out from a life insurance policy is not taxable. However, there are some exceptions. For example, if the contract changes ownership for cash or other valuable consideration, the life insurance payout may be subject to taxation. Additionally, if the death benefit is paid to the estate of the insured or if the deceased person owns the policy on the date of death, the life insurance death benefits may also be taxed.

It is important to note that while the return of premium on a life insurance policy is generally not taxed, there may be other fees or riders associated with the policy that could be taxable. Therefore, it is always a good idea to carefully review the terms and conditions of any life insurance policy before purchasing it.

Overall, the tax-free nature of returns generated from return-of-premium life insurance policies can be a significant advantage for individuals looking to protect their loved ones financially while also planning for their own future financial needs.

Life Insurance Proceeds: When to Report and Why

You may want to see also

Explore related products

![]()

Return of premium life insurance is more expensive than a traditional term life insurance plan

Return of premium (ROP) life insurance is a type of term life insurance that allows you to reclaim your premium payments if you outlive the length of your policy. This type of insurance plan can be more expensive than traditional term life insurance.

Return of premium life insurance is a type of term life insurance policy. Like other term life policies, it is written to cover a specified period, which could be 5, 10, 20, or 30 years. If the insured dies during this time, the insurance company pays the death benefit to the beneficiary. At the end of the term, the policy expires. The policyholder may renew the coverage or convert it into another type of life insurance policy. If no action is taken, the coverage ends.

During the period of coverage, the policyholder must pay premiums. If there is no claim made, i.e., if the insured outlives the policy term, then no death benefit is paid. Normally, the insurance company keeps the premiums in this case. However, ROP term life insurance allows the policyholder to receive a refund of the premiums paid.

The pros of return of premium life insurance

The biggest advantage of ROP life insurance is the ability to reclaim past premium payments. If you outlive your term, you will typically be able to receive a lump-sum payment combining all previous premiums paid. This can be helpful if you have new expenditures to cover later in life, such as a mortgage or retirement plan.

Any returns generated from this type of plan are generally not taxed. Thus, you may be able to receive your lump-sum premium payment tax-free.

The cons of return of premium life insurance

The main disadvantage of ROP life insurance is the cost. Regular term life insurance is attractive to many due to its affordability. In contrast, ROP life insurance is more expensive. While you may get some or all of your money back, you will have to budget for higher premiums. If you cannot afford a costly policy, this might not be a suitable option.

Additionally, if you allow your policy to lapse or cancel it early, you will likely not receive a refund of your premiums. The policy terms may also state that you need to keep the policy in force for the entire period to qualify for a return of premium. Therefore, if the policy is cancelled early due to non-payment, you may not be able to get a refund.

A return of premium life insurance policy may be worth it if you can afford the higher premiums. However, if you do not outlive your term, it will have been much more expensive than a traditional term plan while offering the same death benefit. It is important to understand that you are not receiving any additional money with this type of policy, only the money you have previously paid into the policy.

Who Gets Your Life Insurance Payout?

You may want to see also

Explore related products

![]()

You can receive a refund of some or all of your premium payments

Return of premium (ROP) life insurance is a type of term life insurance that allows you to receive a refund of your premium payments if you outlive the length of your policy. This type of policy is often chosen by those who want the security of a payout—either to their loved ones or back to themselves.

If you pass away within the term of your policy, your beneficiaries will receive a death benefit payout, and the premium payments will be kept by the insurer. However, if you outlive the term, you will be refunded either some or all of your premium payments. This refund is typically given as a lump sum and is not subject to tax.

Pros and Cons

The biggest advantage of ROP life insurance is the ability to reclaim past premium payments. This can be particularly beneficial if you have new expenditures to cover later in life, such as a mortgage or retirement plan. ROP life insurance can, therefore, function as a savings account with a bonus life insurance add-on.

However, the main disadvantage of ROP life insurance is the cost. This type of policy is usually much more expensive than traditional term life insurance, and you may be better off investing the difference. Additionally, if you cancel your policy early or allow it to lapse, you will likely not receive a refund of your premiums.

U.S. Military Life Insurance: War Clause Coverage?

You may want to see also

Frequently asked questions

Return of premium (ROP) life insurance is a type of term life insurance policy. It allows policyholders to receive a refund of all or part of their premiums if they outlive the term of the policy.

The biggest pro of ROP life insurance is the ability to reclaim past premium payments. If you outlive your term, you will usually be able to receive a lump-sum payment combining all previous premiums paid. This can be helpful for any new expenditures you'll have to cover later in life, like a mortgage or retirement plan.

The main con of ROP life insurance is the cost. ROP life insurance is usually much more expensive than traditional term life insurance. You may be better off purchasing a less expensive, traditional term life insurance plan and investing the difference.

ROP life insurance is a blend of term life coverage and a refund feature. Traditional term policies simply expire if you outlive the term and offer no money back. ROP life insurance, on the other hand, offers a refund of premiums paid over the policy term. This makes it a hybrid between pure insurance and a form of financial reimbursement.