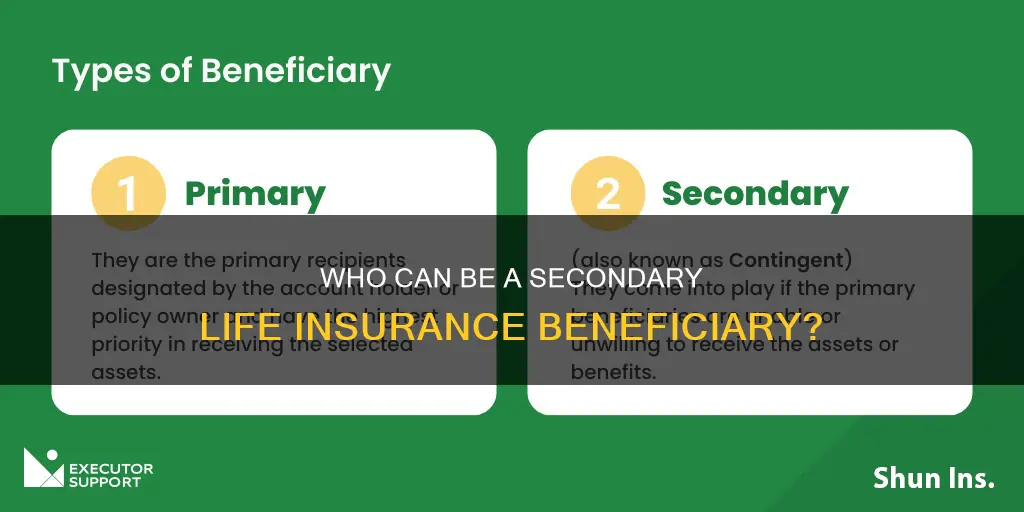

When you take out a life insurance policy, you will be asked to name a primary beneficiary, who is first in line to receive the death benefit from your policy. However, you may also want to name a secondary beneficiary, also known as a contingent beneficiary, who will inherit the benefit if the primary beneficiary is no longer alive or disclaims their inheritance. This is a very personal decision, and it's important to keep your beneficiary designations up to date as your life changes.

| Characteristics | Values |

|---|---|

| Other names | Contingent beneficiary |

| Who can be a secondary beneficiary? | Person, charity, trust or other entity |

| Who inherits assets? | The primary beneficiary, unless they die before the grantor, disclaim their inheritance, or are directed to provide for the secondary beneficiary |

| Who inherits assets after? | The secondary beneficiary |

| Who inherits assets if no secondary beneficiary? | The assets are paid to the estate and are subject to estate taxes |

| Who inherits assets if no primary beneficiary? | The secondary beneficiary |

| Who inherits assets if both primary and secondary beneficiaries are deceased? | The assets are paid to the estate |

| Who inherits assets if primary beneficiary cannot be located? | The secondary beneficiary |

| Who is first in line to receive the death benefit? | Primary beneficiary |

| Who is next in line to receive the death benefit? | Secondary beneficiary |

Explore related products

What You'll Learn

![]()

Who can be a secondary beneficiary?

A secondary beneficiary, also known as a contingent beneficiary, is a person or entity that inherits assets from a grantor after the death of the primary beneficiary or if the primary beneficiary decides to disclaim their inheritance. The secondary beneficiary inherits assets only when certain conditions are met.

When choosing a secondary beneficiary, it is essential to consider individuals or organisations you trust with your payout. While primary beneficiaries are typically those closest to you, contingent beneficiaries might be less close to you. However, it is still crucial to select people or organisations you believe will utilise the payout as per your wishes.

When designating beneficiaries, you have the final say over the distribution of your death benefit. You can choose one or more people as your secondary beneficiaries. It is also possible to name a trust you've set up, with the proceeds administered by a trustee.

In the case of minor children, it is essential to appoint an adult guardian for them in your will or consider setting up a trust. This ensures that the death benefit is used for their benefit while they are still minors.

Additionally, it is worth noting that your state of residence or insurance provider may have specific rules regarding who can be named as a secondary beneficiary. For example, in some states, a spouse may need to sign a waiver before you can name someone else as the beneficiary. Therefore, it is important to review your state's laws and insurance regulations before finalising your choice of secondary beneficiary.

Understanding Tax Implications of Life Insurance Cash Surrender

You may want to see also

Explore related products

![]()

How to choose a secondary beneficiary?

A secondary beneficiary, also known as a contingent beneficiary, is a person or entity that inherits assets from a grantor after the primary beneficiary's rights are considered and satisfied. The primary beneficiary is the person or entity first in line to receive the death benefit from your life insurance policy.

- Understand the role of a secondary beneficiary: A secondary beneficiary inherits assets only when certain conditions are met, such as the death of the primary beneficiary, the primary beneficiary's decision to disclaim their inheritance, or if the primary beneficiary is directed via a will or estate to provide for the secondary beneficiary.

- Consider your relationship with potential secondary beneficiaries: Typically, individuals choose close relatives, such as a spouse, children, or other family members, as their primary beneficiaries. When selecting a secondary beneficiary, consider individuals who are financially dependent on you or those who will suffer financial loss due to your death.

- Evaluate the needs of potential secondary beneficiaries: Consider individuals who may have financial needs that are not currently being met or who may require additional support in the future.

- Consult with professionals: Speak with a financial advisor or attorney to ensure that your beneficiary designations align with your estate plan and that all necessary legal requirements are met. They can also guide you in structuring your designations to avoid probate and minimize taxes.

- Keep beneficiary designations up to date: Life changes, such as marriage, divorce, or the birth of a child, may impact your choice of secondary beneficiary. Regularly review and update your beneficiary designations to ensure they reflect your current wishes and life circumstances.

- Consider multiple secondary beneficiaries: You can designate multiple secondary beneficiaries if you wish. If you choose to do so, decide how you want the payout to be split among them, typically by percentage.

Life Insurance Beneficiaries and Tax: What's the Verdict?

You may want to see also

Explore related products

$18.55 $19.95

![]()

When to change a secondary beneficiary?

A secondary beneficiary, also known as a contingent beneficiary, is a person or entity that inherits assets from a grantor if the primary beneficiary is no longer alive or disclaims their inheritance. It is important to keep your beneficiary designations up to date as your life changes. Here are some scenarios that may prompt you to change your secondary beneficiary:

- Marriage or Divorce: Life insurance policies typically require the spouse's consent if they are not named as the primary beneficiary. In the case of divorce, you may need to update the designation to reflect your new relationship status.

- Birth of a Child: The arrival of a new family member may influence your decision to add or change a secondary beneficiary, especially if you want to provide for their future.

- Death of a Loved One: If one of your designated beneficiaries passes away, you may want to review and update your beneficiary designations accordingly.

- Major Life Changes: Other significant life events, such as moving out of your parents' house or experiencing a change in financial circumstances, may prompt you to reconsider your choice of secondary beneficiary.

- Regular Review: It is a good practice to review your beneficiary designations periodically, such as during your employer's annual benefits enrollment or on a specific date you set for yourself each year. This ensures that your designations remain current and align with your evolving life circumstances.

- Legal Requirements: Some states have specific laws regarding beneficiary designations. For example, in certain states, you may be required to list your spouse as your primary beneficiary, and they must receive a certain percentage of the benefit. Be sure to review your state's laws before making any changes.

Primerica Life Insurance: Borrowing Options and Benefits

You may want to see also

Explore related products

$43.99 $54.99

![]()

How to change a secondary beneficiary?

A secondary beneficiary, also known as a contingent beneficiary, is a person or entity that inherits assets from a grantor after the primary beneficiary's rights are considered and satisfied. A secondary beneficiary inherits assets only when certain conditions are met, such as the death of the primary beneficiary or the primary beneficiary's decision to disclaim their inheritance.

To change a secondary beneficiary, the policyholder should contact their insurance company. The process for changing a beneficiary may vary depending on the provider. Generally, the policyholder will need to fill out a change of beneficiary form, which includes information such as the policyholder's name, the new beneficiary's name, and the reason for the change. In some cases, a copy of the policyholder's death certificate may be required if the beneficiary is being changed due to their death. Once the form is completed, it must be submitted to the insurance company for approval. It is important to keep beneficiary information up to date, especially when life circumstances change, such as marriage, divorce, or the birth of a child.

It is worth noting that there are instances when approval may be required to change the beneficiary name. These include giving power of attorney to someone, living in a community property state, or naming an irrevocable beneficiary. Additionally, if the policy has been transferred to someone else, the original policyholder can no longer change the beneficiary.

IBS and Life Insurance: What You Need to Know

You may want to see also

Explore related products

$16.13 $19.99

![]()

What happens if there is no secondary beneficiary?

A secondary beneficiary, also known as a contingent beneficiary, is a person or entity that inherits assets from a grantor after the primary beneficiary's rights are considered and satisfied. The secondary beneficiary inherits assets only when certain conditions are met, such as the death of the primary beneficiary, or if the primary beneficiary decides to disclaim their inheritance.

If there is no secondary beneficiary, the life insurance policy's payout goes into the insured's estate, where it can be subject to estate taxes and claims by creditors. The insured's heirs may ultimately receive less than the policy's original death benefit, and it will take longer for them to receive it. The payout may be subject to a lengthy probate process, and it is recommended to consult a financial or tax advisor to understand the specific details of the situation.

To avoid this, policyholders should regularly review and update their primary and contingent beneficiaries. It is important to keep the policy and named beneficiaries up to date to have the most control over who receives the life insurance proceeds.

Additionally, it is worth noting that state laws may differ in scenarios where the primary beneficiary and the insured die simultaneously. In some states, the Uniform Simultaneous Death Act is adopted, which presumes that the insured person outlived the primary beneficiary in cases where there is no way to determine who passed away first. In states without this Act, even a few minutes might make a difference in determining the distribution of the death benefit.

Cholesterol and Life Insurance Blood Tests: What's the Link?

You may want to see also

Frequently asked questions

A secondary beneficiary, also known as a contingent beneficiary, is a person or entity that inherits assets from a grantor after the primary beneficiary.

The primary beneficiary is first in line to receive the death benefit from a life insurance policy. The secondary beneficiary inherits the assets only if the primary beneficiary is deceased, disclaims their inheritance, or is incapacitated.

If you don’t designate a secondary beneficiary, and your primary beneficiary is deceased, your death benefit will be paid to your estate instead of the people or organisations you may have selected.

A secondary beneficiary can be a person, a charity, a trust, or your estate.