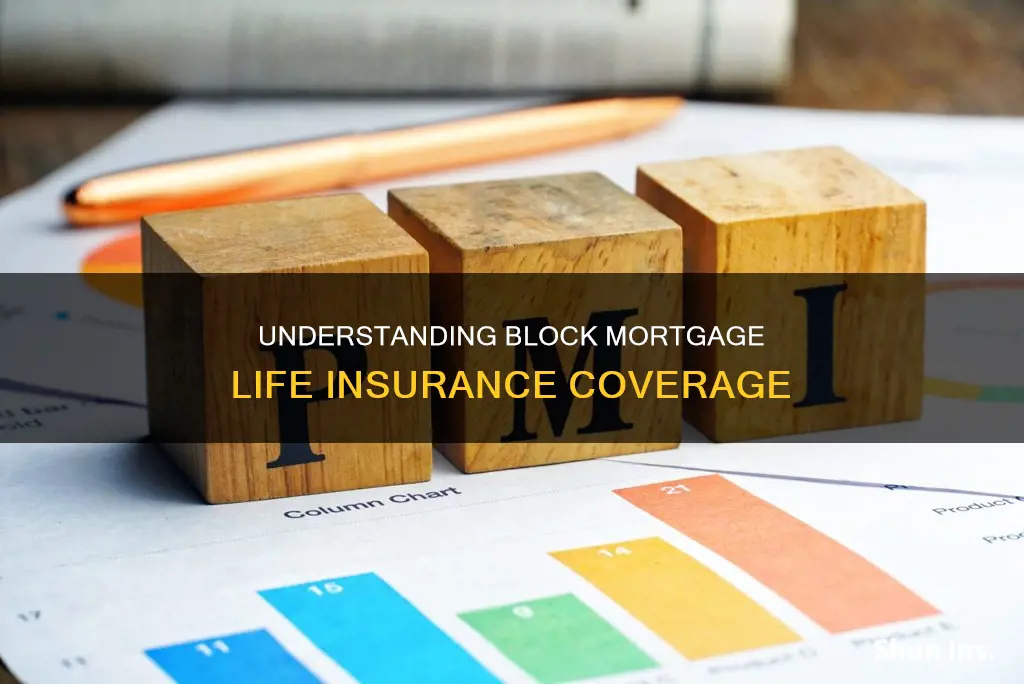

Block mortgage life insurance is a type of life insurance that pays off the remaining balance on a mortgage in the event of the policyholder's death. It is designed to protect the policyholder's loved ones from inheriting a large financial burden and ensure that they can retain ownership of the property. The death benefit payout from a block mortgage life insurance policy goes directly to the lender to cover the outstanding mortgage balance, rather than to the policyholder's beneficiaries. This type of insurance is typically purchased in addition to traditional life insurance and offers peace of mind that the policyholder's family will not be left with debt or lose their home.

Explore related products

What You'll Learn

![]()

Block mortgage life insurance is a type of credit life insurance

Credit life insurance is typically offered when a borrower takes out a significant loan, such as a mortgage. The policy pays off the loan in the event that the borrower dies. This type of insurance is especially important if a spouse or someone else is a co-signer on the loan, as it can protect them from having to repay the debt. Credit life insurance can also be useful if the borrower has dependents who rely on the underlying asset, such as a family home.

The face value of a credit life insurance policy decreases over time as the loan is paid off, until both values reach zero. This means that the death benefit of the policy decreases as the policyholder's debt decreases. Credit life insurance policies often have less stringent underwriting requirements, and may not require a medical exam.

Credit life insurance is optional and is not required by lenders. It is illegal for an entity to require credit life insurance for a loan, and lenders may not base their lending decisions on whether or not the borrower accepts credit life insurance. However, in some cases, credit life insurance may be built into a loan, which would increase the monthly payments.

The beneficiary of a credit life insurance policy is the lender, not the heirs of the policyholder. The payout goes directly to the lender to pay off the outstanding loan balance. This is in contrast to term life insurance, where the payout goes to the beneficiary, who can then choose how to use the money.

Asurea and Globe Life Insurance: What's the Connection?

You may want to see also

Explore related products

![]()

It pays out to the lender, not the beneficiaries

Block mortgage life insurance is a type of life insurance designed to pay off the policyholder's mortgage if they pass away during the policy term. This type of insurance is often purchased to protect a repayment mortgage, which reduces over time.

One key feature of block mortgage life insurance is that the death benefit goes directly to the lender to pay off the outstanding mortgage balance. In other words, it pays out to the lender, not the policyholder's beneficiaries. This is a significant distinction from traditional life insurance policies, where the death benefit is typically paid to the policyholder's chosen beneficiaries, such as family members.

The fact that block mortgage life insurance pays out to the lender has several implications. Firstly, it ensures that the mortgage will be paid off in the event of the policyholder's death, providing peace of mind that their loved ones will not be burdened with the debt. Secondly, it means that the beneficiaries do not receive the proceeds directly and, therefore, cannot use the money for other purposes. This lack of flexibility can be considered a drawback, as the beneficiaries may have other financial needs or expenses that require immediate attention.

While block mortgage life insurance pays out to the lender, it is important to note that the policyholder's beneficiaries still play a role in the process. In the event of the policyholder's death, the beneficiaries must file a claim to initiate the payout to the lender. This ensures that the appropriate procedures are followed and that the lender receives the funds to settle the outstanding mortgage balance.

Overall, the fact that block mortgage life insurance pays out to the lender has both advantages and disadvantages. On the one hand, it guarantees that the mortgage will be settled, protecting the policyholder's loved ones from the burden of debt. On the other hand, it limits the flexibility of the beneficiaries, who may have other financial priorities or needs that require immediate attention. As such, it is essential for individuals to carefully consider their specific circumstances and financial goals when deciding whether to opt for block mortgage life insurance or other forms of insurance, such as traditional life insurance policies.

How to Insure Your Girlfriend's Life: All You Need to Know

You may want to see also

Explore related products

![]()

It is not a legal requirement

Block mortgage life insurance is not a legal requirement. While it can be a useful option for those who want to ensure their mortgage is paid off in the event of their death, it is not mandatory. There are no legal consequences for cancelling this type of insurance, and it is up to the individual to decide whether they want or need this type of coverage.

The decision to purchase block mortgage life insurance depends on an individual's financial situation and their dependents' ability to cope with the mortgage payments in the event of their death. If you already have sufficient life insurance or other financial means to cover the mortgage, then you may not need additional block mortgage life insurance.

It is important to note that lenders often require borrowers to have mortgage protection insurance, which is different from block mortgage life insurance. Mortgage protection insurance, also known as private mortgage insurance or mortgage insurance premium, is typically required if the down payment on a home loan is less than a certain percentage, usually 20%. This type of insurance protects the lender in case the borrower defaults on their loan.

Additionally, it is worth considering the pros and cons of block mortgage life insurance before purchasing it. While it can provide peace of mind and ensure that your loved ones will not be burdened with mortgage payments, it also has drawbacks. The payout from block mortgage life insurance decreases over time as you pay down your mortgage, while the premiums remain the same. This means that you are paying the same amount for a lower level of coverage. Furthermore, the money from block mortgage life insurance goes directly to the lender, and your beneficiaries do not have the flexibility to use it for other expenses.

Overall, while block mortgage life insurance can be a valuable tool for some, it is not a legal requirement. Individuals should carefully consider their financial situation, the needs of their dependents, and the pros and cons of the insurance before deciding whether to purchase it.

AAA Life Insurance: Is It Worth the Hype?

You may want to see also

Explore related products

![NMLS Study Guide 2024-2025: 5 Full-Length MLO Practice Exams, SAFE Mortgage Loan Originator Test Prep Secrets Book with Detailed Answer Explanations: [3rd Edition]](https://m.media-amazon.com/images/I/61zi0BJms+L._AC_UL320_.jpg)

![]()

It is often sold through banks and mortgage lenders

Banks and mortgage lenders sell mortgage protection insurance (MPI) to their customers. MPI is a type of insurance policy that helps your family make your monthly mortgage payments if you, the policyholder and mortgage borrower, die before your mortgage is fully paid off. Certain MPI policies also offer coverage for a limited time if you lose your job or become disabled after an accident.

MPI is often called mortgage life insurance because most policies only pay out when the policyholder passes away. However, MPI is not the same as private mortgage insurance (PMI), which safeguards the owners of your home loan if you stop making payments.

MPI is typically offered to customers by their mortgage lender when they close their loan. However, if the lender does not offer MPI policies, they may be able to provide a referral to a company that does.

MPI is also available from private insurance companies, many of which specialise in MPI policies, and from life insurance providers.

Gerber Life Insurance: Cash Value and Policy Benefits Explained

You may want to see also

Explore related products

![]()

It is more expensive than term life insurance

Block mortgage life insurance, also known as mortgage protection life insurance, is designed with a single goal in mind: to pay off the remaining balance on a home loan in the event of the policyholder's death. While this type of insurance can provide peace of mind and ensure that loved ones are not burdened with mortgage debt, it is important to consider its limitations and cost compared to other options, such as term life insurance.

One of the main drawbacks of block mortgage life insurance is its cost. The premiums for this type of insurance are often much higher than those of term life insurance. This is because the coverage amount decreases over time as the loan is paid down, while the premiums typically remain the same. This means that the cost per dollar of coverage increases over time. Additionally, block mortgage life insurance lacks the cash value growth component of permanent life insurance, so it cannot be used as a wealth-building vehicle while the policy is active.

Term life insurance, on the other hand, usually has lower premiums for the same initial coverage amount. This is because term life insurance provides a fixed amount of coverage for a specific period, typically 10 to 30 years, and the coverage amount does not decrease over time. The beneficiaries of a term life insurance policy can also use the payout for any purpose, not just paying off the mortgage. This flexibility is a significant advantage over block mortgage life insurance, where the payout goes directly to the lender.

Another factor contributing to the higher cost of block mortgage life insurance is the lack of a medical exam requirement. Since these policies do not consider the policyholder's health, they can be more expensive for individuals in good health. Term life insurance, on the other hand, takes into account various factors such as age, gender, health, smoking status, and occupation when determining premiums, resulting in lower costs for healthier individuals.

While block mortgage life insurance may be appealing due to its convenience and ease of qualification, it is important to consider the long-term costs and limitations. Term life insurance often provides more value and flexibility, allowing beneficiaries to use the payout for a range of expenses, not just the mortgage. By comparing the features and costs of both options, individuals can make an informed decision that best suits their needs and budget.

Understanding Military Life Insurance: Spouse Benefits Explained

You may want to see also

Frequently asked questions

Block mortgage life insurance is a type of insurance that covers the remaining balance on a mortgage in the event of the policyholder's death.

In the event of the policyholder's death, the insurance company will pay out a sum of money to the beneficiaries, who can then use this money to pay off the remaining mortgage.

Block mortgage life insurance provides peace of mind and financial stability for the policyholder, ensuring that their loved ones will not be burdened with mortgage debt in the event of their death. It also gives beneficiaries access to more equity in the home, which they can borrow against or gain proceeds from if they sell it.

Yes, one alternative is to take out a separate life insurance policy, which can also be used to pay off a mortgage in the event of the policyholder's death. Another option is mortgage protection insurance, which covers monthly mortgage costs if the policyholder is temporarily unable to work due to accident, sickness, or unemployment.

Block mortgage life insurance is typically purchased through an insurance company, bank, or mortgage lender. It is not a legal requirement, but it may be stipulated in the mortgage contract.