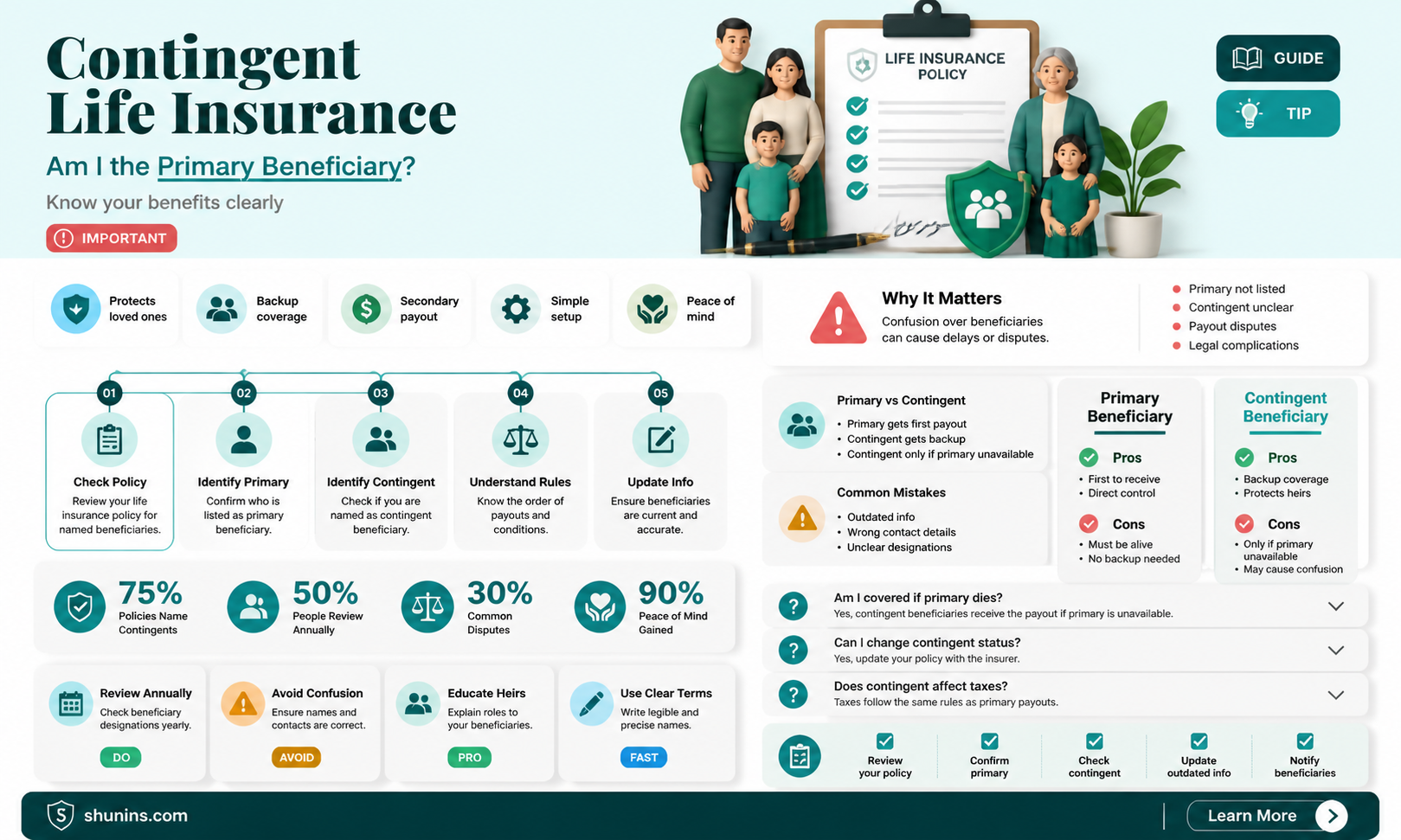

A contingent beneficiary is a person chosen to inherit some or all of the policyholder's assets, but only if the primary beneficiary cannot accept them. The primary beneficiary is the first in line to receive the death benefit. The contingent beneficiary is the second in line to receive the benefit if the primary beneficiary is not alive at the time of the policyholder's death. It is important to have both types of beneficiaries. If the primary beneficiary cannot receive the death benefit, it reverts to the policyholder's estate, even if they both die at the same time.

| Characteristics | Values |

|---|---|

| Definition | A contingent beneficiary is a person or organisation chosen to inherit some or all of your assets if the primary beneficiary cannot accept them. |

| Importance | It is vital to have both primary and contingent beneficiaries. Without a contingent beneficiary, your assets could enter probate if your primary beneficiary is unable to claim them. |

| Who to choose | Typically, a spouse or partner is chosen as the primary beneficiary, and children, other family members, or philanthropic organisations are chosen as contingent beneficiaries. |

| Number of beneficiaries | You can have as many contingent beneficiaries as you want, as long as their portions of the estate add up to 100%. |

| Inheritance criteria | You can establish criteria around your contingent beneficiary's inheritance, e.g. the beneficiary must finish college before inheriting. |

| Trustee | If you name minor children as contingent beneficiaries, you will need to select a trustee to manage the inheritance until the children come of age. |

Explore related products

$90.85 $111

What You'll Learn

![]()

Who can be a primary beneficiary?

A primary beneficiary is the person or persons selected to receive the death benefit from your life insurance policy. Typically, this is a spouse, child, or other family member. However, it can also be a revocable trust (or living trust) or other legal entity.

When selecting a primary beneficiary, you can name one person or multiple people, outlining the percentage of the policy payout each would receive. For example, a parent with a $100,000 life insurance policy can name their son and daughter as the primary beneficiaries, deciding to distribute the assets as $60,000 to the daughter and $40,000 to the son.

It's important to keep your primary beneficiary designations up to date as your life changes (marriage, children, divorce, etc.). For instance, if you have children, you may want to name them as primary beneficiaries. In the case of minors, you can still name them as primary beneficiaries, but you must create a trust and name a guardian to manage it until the child reaches the legal age of consent.

In the event that your primary beneficiary is no longer alive or able to collect, a contingent beneficiary may also be named.

Gerber Life Insurance: Doubling Benefits for Parents

You may want to see also

Explore related products

$49.59 $61.99

![]()

Who can be a contingent beneficiary?

A contingent beneficiary is a person chosen by the policyholder to inherit some or all of their assets if the primary beneficiary is unavailable, unable to be found, or deceased. They are also known as secondary beneficiaries.

The primary beneficiary is the "first in line" to receive the death benefit. The contingent beneficiary is the "second in line" and will only receive the benefit if all primary beneficiaries have passed away, cannot be found, or refuse the benefit.

It is not mandatory to name a contingent beneficiary, but it is highly recommended. If there is no contingent beneficiary, the benefit will be paid to the policyholder's estate and will be subject to estate taxes and probate court.

You can name any person or organisation as your contingent beneficiary. However, if you name a minor child, you will need to select a trustee to manage the payout until the child becomes a legal adult.

You can have multiple contingent beneficiaries and divide your estate among them in any ratio, as long as the total adds up to 100%.

Life Insurance Reinstatement: A Guide for Seniors

You may want to see also

Explore related products

![]()

What happens if there is no primary beneficiary?

If there is no primary beneficiary, the death benefit will be paid out to the insured's estate. This means that the proceeds and the rest of the deceased's property and investments will be distributed according to their will, the insurance contract details, and state law.

The death benefit will be subject to probate, which can take a year or longer, and potentially much longer if the will is contested. The probate process typically involves a court approving an executor of the estate, locating and valuing the assets, paying taxes and other debts, and finally distributing the remaining assets.

During probate, the death benefit may be earmarked to pay down any remaining debts of the deceased before being distributed to heirs. This could leave heirs with less than the original death benefit and not the financial protection the life insurance holder intended.

Therefore, it is important to name both primary and contingent beneficiaries to ensure that the death benefit goes to the intended recipients.

Life Insurance Proceeds: Are Trusts Taxable?

You may want to see also

Explore related products

![]()

What happens if there is no contingent beneficiary?

If there is no contingent beneficiary, the death benefit will be included in the estate of the deceased and will have to go through probate. This means that the court will decide what happens to the benefit, and the process can be lengthy and costly. The value of the benefit will be included as a taxable asset, which may push the estate over the exemption amount. The benefit will also be open to creditors, and the remaining balance will be distributed according to the deceased's will or, in the absence of a will, according to state laws.

To avoid this, it is recommended to name both a primary and a contingent beneficiary when setting up a life insurance policy, retirement account, or living trust. A primary beneficiary is the first person or entity in line to receive the death benefit, while a contingent beneficiary is the second in line and will only receive the benefit if the primary beneficiary has predeceased the policyholder or cannot be located.

Life Insurance for Non-Profits: Funding Peace of Mind

You may want to see also

Explore related products

![]()

How many primary/contingent beneficiaries can there be?

When setting up a life insurance policy, retirement account, or living trust, it is important to name both primary and contingent beneficiaries. The primary beneficiary is the first person or entity in line to receive the assets upon your passing. You can name more than one primary beneficiary and can designate how the assets will be divided among them. For instance, you could name three primary beneficiaries, such as siblings, each receiving a third of the payout.

A contingent beneficiary, on the other hand, is the second in line to inherit the asset. The only way a contingent beneficiary inherits anything from the account or policy is if the primary beneficiary or beneficiaries have predeceased you or otherwise can't be found. You can also name more than one contingent beneficiary and specify how the death benefit should be divided. For example, you could name two contingent beneficiaries, such as your parents, each receiving half of the payout.

Haven Life, for instance, permits up to 10 primary beneficiaries and 10 contingent beneficiaries.

Life Insurance and Suicide in Texas: What's Covered?

You may want to see also

Frequently asked questions

A primary contingent beneficiary is a person chosen by the policyholder to receive the proceeds of the policy if the primary beneficiary is unable to do so. This could be because the primary beneficiary is deceased, cannot be located, or refuses the benefit.

You can name any person or organisation as your primary contingent beneficiary, but you will need to designate a trustee to manage the estate if the beneficiary is a minor.

Yes, you can have multiple primary contingent beneficiaries and divide your estate among them. However, the portions allocated to each beneficiary must add up to 100%.