Life insurance is a way to financially assist your loved ones after you pass away. The average cost of a $250,000 life insurance policy is $23 per month for a 10-year term and $29 for a 20-year term. However, this can vary depending on a range of factors, including age, gender, health status, lifestyle and the specifics of the policy you choose, including term length and coverage amount. For example, a 30-year-old could pay an average of $16 a month for a 10-year term, whereas a 50-year-old would be looking at a monthly rate of $45 for the same coverage.

| Characteristics | Values |

|---|---|

| Average cost of a $250,000 term life insurance policy | $23 per month |

| Average cost of a $250,000 term life insurance policy for a 30-year-old | $130 per year |

| Average cost of a $250,000 term life insurance policy for a 30-year-old for a 10-year term | $16 per month |

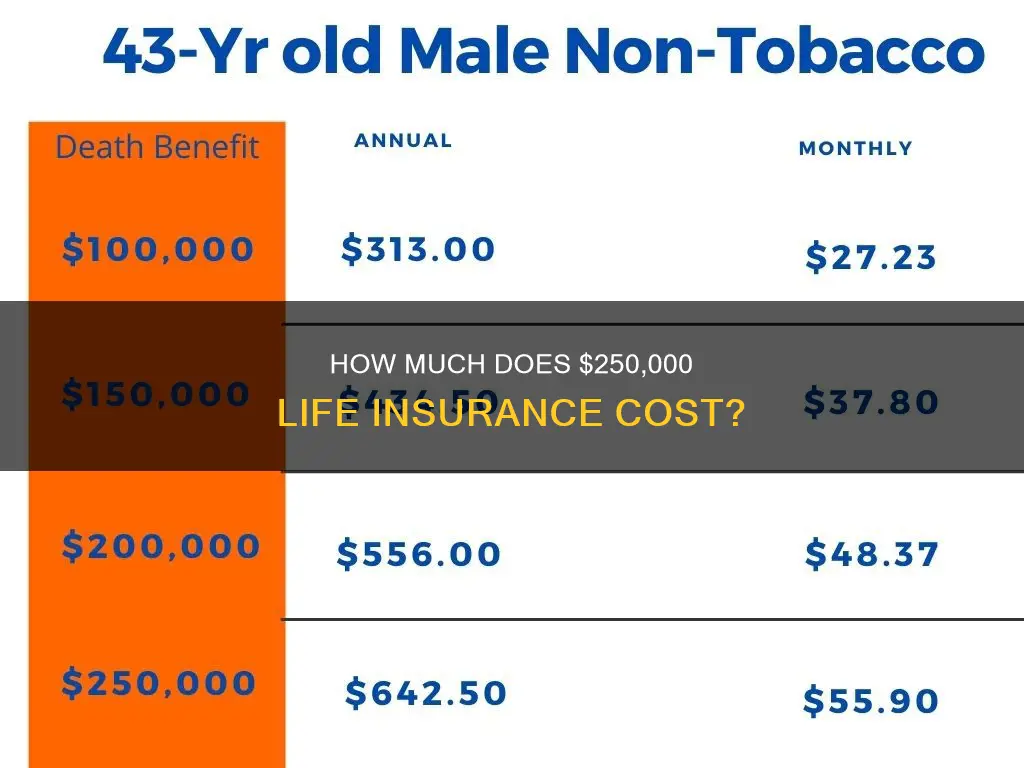

| Average cost of a $250,000 term life insurance policy for a 40-year-old male in excellent health for a 10-year term | $23 per month |

| Average cost of a $250,000 term life insurance policy for a 50-year-old for a 10-year term | $45 per month |

| Average cost of a $250,000 term life insurance policy for a 30-year-old for a 20-year term | $20 per month |

| Average cost of a $250,000 term life insurance policy for a 40-year-old male in excellent health for a 20-year term | $29 per month |

Explore related products

![Life and Health Insurance Study Cards: Life Health Insurance License Exam Prep with Practice Test Questions [Full Color]](https://m.media-amazon.com/images/I/51Pox87Z5lL._AC_UY218_.jpg)

![Life and Health Insurance License Exam Secrets Study Guide - Full-Length Practice Test, Detailed Answer Explanations: [2nd Edition]](https://m.media-amazon.com/images/I/71PdYCnP8ML._AC_UY218_.jpg)

What You'll Learn

- The average cost of a $250,000 life insurance policy is $23 per month for a 10-year term

- The average cost of a $250,000 life insurance policy is $29 per month for a 20-year term

- The average cost of a $250,000 life insurance policy for a 30-year-old is $130 a year for a 10-year term

- The average cost of a $250,000 life insurance policy for a 30-year-old is $180 a year for a 20-year term

- The average cost of a $250,000 life insurance policy for a 30-year-old is $16 a month for a 10-year term

![]()

The average cost of a $250,000 life insurance policy is $23 per month for a 10-year term

Age is one of the main factors that insurance companies consider when determining premiums. The younger you are, the cheaper your life insurance will be. For example, a 30-year-old could pay an average of $16 a month for a 10-year term, whereas a 50-year-old would pay around $45 for the same coverage.

Your health status and lifestyle choices also impact the cost of life insurance. For healthy non-smokers in their thirties, the average price for a 10-year, $250,000 term life policy is about $130 a year.

It's important to note that life insurance premiums are calculated based on a range of factors, including age, gender, health status, lifestyle, term length, and coverage amount. When considering life insurance, it's essential to shop around and compare quotes from different insurance companies to find the best policy for your needs.

Life Insurance Annuity Product: How Does It Work?

You may want to see also

Explore related products

![]()

The average cost of a $250,000 life insurance policy is $29 per month for a 20-year term

The cost of life insurance varies depending on a range of factors, including age, gender, health status, lifestyle and the specifics of the policy. For example, a 30-year-old could pay an average of $16 a month for a 10-year term, whereas a 50-year-old would be looking at a monthly rate of $45 for the same coverage. It is generally cheaper to buy life insurance when you are younger, as you can lock in lower rates.

The term length also affects the price. A 30-year-old would pay an average of $16 per month for a 10-year term but could expect to pay $20 per month for a 20-year term. A 40-year-old male in excellent health can expect to pay around $23 per month for a 10-year term and $29 per month for a 20-year term.

It is important to consider your own personal circumstances when choosing a life insurance policy. The right coverage is generally considered to be around 10 to 20 times your monthly income.

Understanding Indemnification in Life Insurance Policies

You may want to see also

Explore related products

![]()

The average cost of a $250,000 life insurance policy for a 30-year-old is $130 a year for a 10-year term

The average cost of a $250,000 life insurance policy is $23 per month for a 10-year term and $29 for a 20-year term. However, the cost of life insurance varies depending on a number of factors, including age, gender, health status, lifestyle and the specifics of the policy. For example, a 30-year-old could pay an average of $16 a month for a 10-year term, whereas a 50-year-old would be looking at a monthly rate of $45 for the same coverage.

Age is one of the main factors that insurance companies consider when determining premiums because it significantly impacts risk. While the 40s are a common age to buy life insurance, getting a policy earlier can result in lower monthly premiums. For a 40-year-old male in excellent health, the average monthly premium for a $250,000 policy with a 10-year term is about $23.

Selling Life Insurance: Phone Calls and Policies

You may want to see also

Explore related products

![]()

The average cost of a $250,000 life insurance policy for a 30-year-old is $180 a year for a 20-year term

The average cost of a $250,000 life insurance policy is $23 per month for a 10-year term and $29 for a 20-year term. However, the cost of life insurance varies depending on several factors, including age, gender, health status, lifestyle, and the specifics of the policy chosen, such as term length and coverage amount.

Age is one of the main factors that insurance companies consider when determining premiums. The younger you are, the lower your monthly premiums are likely to be. For example, a 30-year-old could pay an average of $16 a month for a 10-year term, while a 50-year-old would pay around $45 for the same coverage.

Similarly, the length of the term affects the price. A 30-year-old would pay an average of $16 per month for a 10-year term but could expect to pay $20 per month for a 20-year term. According to Forbes Advisor, the average cost of a 20-year term life insurance policy worth $250,000 for a 30-year-old is $180 per year. This assumes the individual is a healthy non-smoker.

It's worth noting that insurance companies offer a range of policies, and the $250,000 life insurance policy is the most common coverage amount. When choosing a life insurance policy, it's essential to consider your specific needs and circumstances, as well as the potential financial assistance you want to provide for your loved ones after your passing.

Life Insurance Proceeds: Taxable in Ireland?

You may want to see also

Explore related products

![]()

The average cost of a $250,000 life insurance policy for a 30-year-old is $16 a month for a 10-year term

The average cost of a $250,000 life insurance policy is $23 per month for a 10-year term and $29 for a 20-year term. However, this figure varies depending on the age of the person taking out the policy. For example, a 30-year-old can expect to pay an average of $16 a month for a 10-year term, whereas a 50-year-old would be looking at a monthly rate of $45 for the same coverage.

Age is one of the main factors that insurance companies consider when determining premiums because it significantly impacts risk. While the 40s are a common age to buy life insurance, getting a policy earlier can result in lower monthly premiums. A 20-year-old non-smoker can expect to pay around $130 a year for a 10-year term, whereas a 60-year-old would struggle to find a 30-year term life insurance policy at all.

Other factors that can influence the cost of life insurance include gender and lifestyle choices such as smoking or participating in risky activities.

Postal Life Insurance: Steps to Close Your Policy

You may want to see also

Frequently asked questions

A $250,000 term life insurance policy costs around $23 per month on average.

Age is one of the main factors insurance companies consider when determining premiums. A 30-year-old could pay an average of $16 a month for a 10-year term, whereas a 50-year-old would be looking at a monthly rate of $45 for the same coverage.

The term length also affects the price. A 30-year-old would pay an average of $16 per month for a 10-year term but could expect to pay around $20 per month for a 20-year term.

The average price for a 10-year, $250,000 term life policy is about $130 a year for a healthy 30-year-old nonsmoker.

Life insurance premiums are calculated based on a range of factors such as gender. For a 40-year-old male in excellent health, the average monthly premium for a $250,000 policy with a 10-year term is about $23.