Endowment life insurance is a type of life insurance that combines a death benefit with a savings plan. It allows the policyholder to pay premiums and receive a lump sum payment or instalment payments if the insured outlives the policy. The amount you pay depends on how much you want to accumulate and how soon you want the money. Endowment life insurance policies can fit with any life stage and financial goals, and are often available when you're between the ages of 18 and 60.

| Characteristics | Values |

|---|---|

| Type of insurance | Endowment life insurance |

| Who is it for? | People between the ages of 18 and 60 |

| What does it combine? | Temporary life insurance with a savings plan |

| What is the endowment? | A specific amount of money you fund after a certain number of years if you're still living |

| What happens if you die before the policy matures? | The insurance company pays out the policy amount to your loved ones |

| How do you fund the endowment? | By paying premiums into a policy |

| How does the policy work? | The policy's value grows over time |

| How much do you pay? | The amount you pay depends on how much you want to accumulate and how soon you want the money |

| What are the benefits? | Endowment life insurance policies can fit with any life stage and financial goals |

Explore related products

What You'll Learn

![]()

Endowment insurance combines a death benefit with a savings plan

Endowment insurance is a type of life insurance that combines a death benefit with a savings plan. It allows the policyholder to pay premiums and receive a lump sum payment or instalment payments if the insured outlives the policy. The "endowment" is a specific amount of money you fund after a certain number of years if you're still living. However, if you die before the policy matures, the insurance company pays out the policy amount to your loved ones.

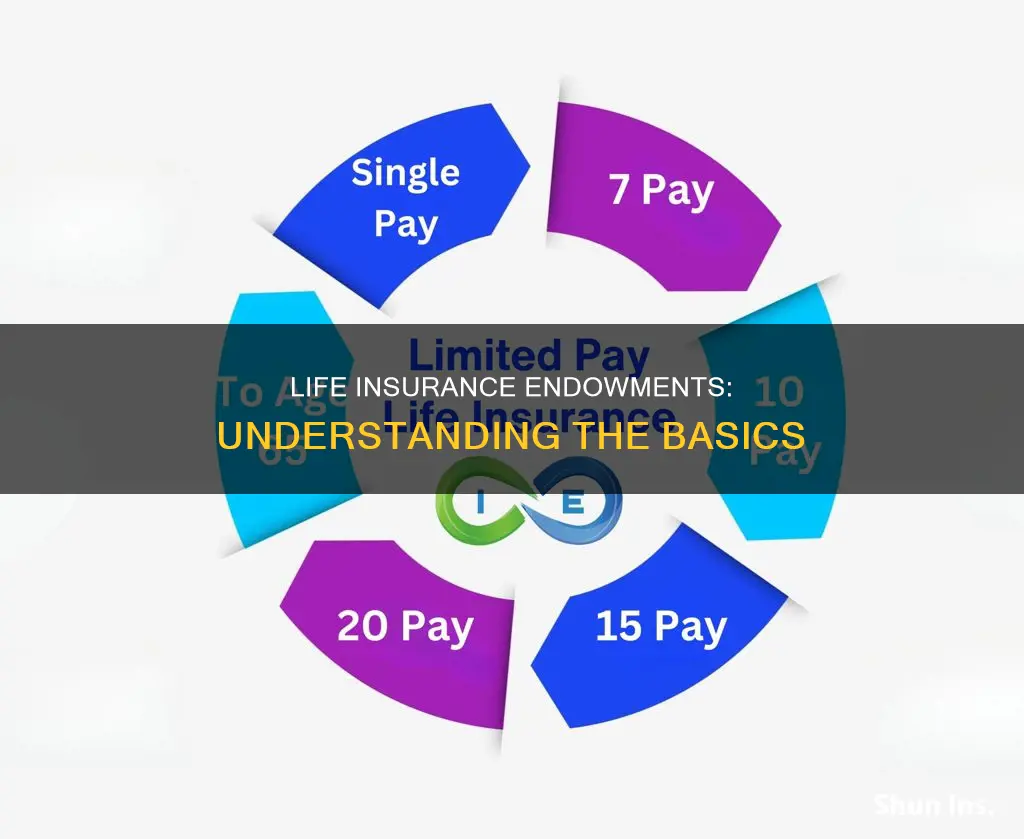

The amount you pay depends on how much you want to accumulate and how soon you want the money. You can spread out the payments with a long-term goal, helping to keep premiums low. Endowment life insurance policies can fit with any life stage and financial goals. Coverage is often available when you're between the ages of 18 and 60 (check with your insurance provider for details).

Endowment insurance is a temporary type of life insurance. These policies do not last your entire life. While there are benefits of using an endowment policy, it's wise to explore all of the alternatives and choose the option that best suits your needs. For example, if you're saving for retirement, evaluate how retirement accounts like 401(k) plans and individual retirement accounts (IRAs) might help you accomplish that.

Cash Value Life Insurance: Benefits and Their Trade-Offs

You may want to see also

Explore related products

![Pelican Offices, Lombard Street, and Spring Gardens; for Insurance on Lives, Granting Annuities, and Endowments for Children 1828 [Leather Bound]](https://m.media-amazon.com/images/I/617DLHXyzlL._AC_UY218_.jpg)

![]()

Endowment insurance pays out a lump sum

Endowment insurance is a type of life insurance that combines a death benefit with a savings plan. The policyholder pays premiums into a policy, and the policy's value grows over time. The amount paid depends on how much the policyholder wants to accumulate and how soon they want the money. The policyholder can then receive a lump sum payment or instalment payments if they outlive the policy.

The "endowment" is a specific amount of money that the policyholder funds after a certain number of years if they are still living. If the policyholder dies before the policy matures, the insurance company pays out the policy amount to their loved ones.

Endowment insurance policies can fit with any life stage and financial goals. Coverage is often available when the policyholder is between the ages of 18 and 60. The endowment coverage term can last a set number of years or until the policyholder reaches a target age.

Endowment life insurance is a temporary type of life insurance. These policies do not last the policyholder's entire life, and the return is not as high as other accounts provide.

Ohio Life and Health Insurance Exam: Challenging or Easy?

You may want to see also

Explore related products

$45.16 $55

$68.07 $91.99

![]()

Endowment insurance is temporary

Endowment insurance is a temporary type of life insurance that combines a death benefit with a savings plan. The policyholder pays premiums and, if they outlive the policy, they receive a lump sum payment or instalment payments. The policy term can last a set number of years or until the policyholder reaches a target age. The amount paid in premiums depends on how much the policyholder wants to accumulate and how soon they want the money. Endowment insurance policies can fit with any life stage and financial goals, but it is wise to explore all the alternatives and choose the option that is best for you.

KeyBank's Life Insurance Offerings: What You Need to Know

You may want to see also

Explore related products

![]()

Endowment insurance can fit with any life stage and financial goals

The flexibility of endowment insurance means that it can be used for a variety of financial goals, such as saving for college or retirement. For example, if you are saving for retirement, you can evaluate how endowment insurance compares to other retirement accounts like 401(k) plans and individual retirement accounts (IRAs). Alternatively, if you want to maximise the death benefit and minimise monthly premiums, a basic term policy might be more appropriate.

Endowment insurance is typically available to those aged between 18 and 60, although this may vary depending on the insurance provider. The policy's value grows over time, and you can spread out the payments with a long-term goal to keep premiums low. This makes endowment insurance a good option for those who want to save for the future while also having the peace of mind that comes with life insurance.

Life Insurance for Astronauts: Is It Possible?

You may want to see also

Explore related products

![]()

Endowment insurance can be used for college savings or retirement

Endowment insurance is a type of life insurance that combines a death benefit with a savings plan. The policyholder pays premiums into a policy, and the policy's value grows over time. The amount you pay depends on how much you want to accumulate and how soon you need the money. The policy term can last a set number of years or until you reach a target age. If you die before the maturity date, your heirs will receive the insurance death benefit. If you live until the maturity date, you will receive a large payout with a guaranteed return.

Endowment insurance can also be used to save for college. The guaranteed lump sum payout at the end of the policy term can help cover the cost of tuition and other expenses. This can be a good option for those who want to ensure they have a set amount of money available when their children reach college age.

Endowment life insurance policies can fit with any life stage and financial goals. However, it is important to explore all the alternatives and choose the option that is best for your individual needs. For example, if you are saving for retirement, you may want to consider retirement accounts such as 401(k) plans or individual retirement accounts (IRAs).

Canceling Ladder Life Insurance: A Step-by-Step Guide

You may want to see also

Frequently asked questions

Endowment life insurance is a type of life insurance that combines a death benefit with a savings plan.

Endowment insurance allows the policyholder to pay premiums and receive a lump sum payment or instalment payments if the insured outlives the policy.

If you die before the maturity date, the insurance company will pay out the policy amount to your loved ones.

The amount you pay depends on how much you want to accumulate and how soon you want the money. You can spread out the payments with a long-term goal, helping to keep premiums low.

Endowment life insurance policies can fit with any life stage and financial goals. They are also a good option if you want to maximise the death benefit and minimise monthly premiums.