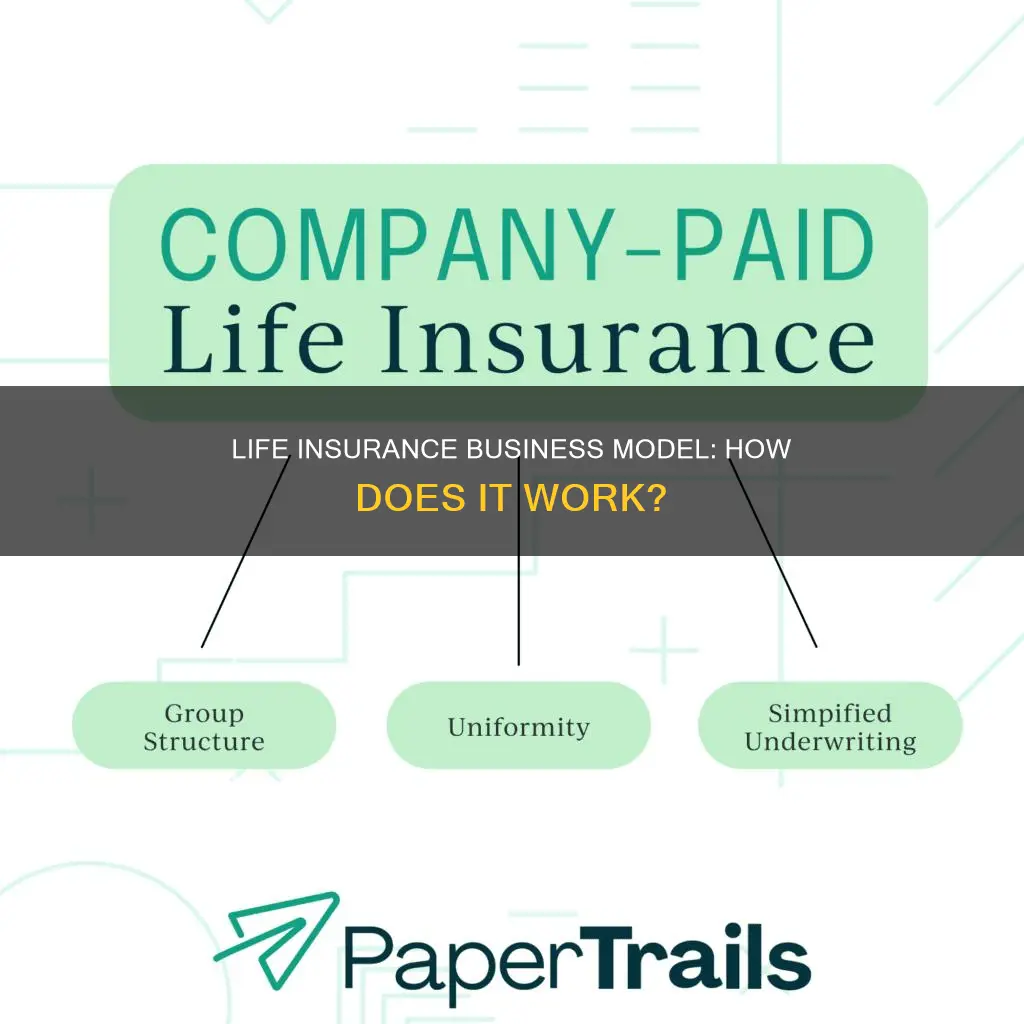

Life insurance is a financial product that provides security to families in the event of a sudden death. It is a contract that ensures financial stability in the form of compensation for losses other than death, such as health, travel, and property damage. The business model of life insurance companies revolves around generating revenue by taking on risk. They charge premiums to policyholders, which they then reinvest in other assets to generate interest. Additionally, life insurance companies may increase premiums for high-risk customers, such as those in dangerous professions or with critical illnesses, to make extra profits. Tax benefits are also offered in life insurance plans, providing an added incentive for customers.

| Characteristics | Values |

|---|---|

| Premium loading | Insurance companies make a profit or extra income through premium loading. They raise the premium for high-risk customers, such as those in risky work or with critical illnesses. |

| Tax benefits | Life insurance plans offer tax benefits, with the premium paid by the policyholder being tax-deductible. Maturity insurance plans are also tax-free. |

| Revenue generation | Insurance companies generate revenue by putting money at risk. They bet on the risk that their policyholders will not die or suffer losses, and then redistribute that risk across a broader portfolio. |

| Financial security | Life insurance provides financial security for families in the event of the sudden death of a family member. |

Explore related products

What You'll Learn

- Premium loading: insurance companies make a profit by raising the premium for high-risk customers

- Tax benefits: life insurance plans offer tax savings to policyholders

- General insurance: financial security in the form of compensation for losses other than death

- Risk pooling: insurance companies redistribute risk across a broader portfolio

- Revenue generation: insurance companies make money by charging premiums and reinvesting in other assets

![]()

Premium loading: insurance companies make a profit by raising the premium for high-risk customers

Life insurance companies make a profit by charging premiums for offering insurance coverage and reinvesting those premium amounts in other assets that generate interest. They bet on the risk that their policyholders will not die, and their vehicles will not be damaged, and their property will not be destroyed.

Some policyholders are considered high-risk customers, for example, those in risky work such as the army, or those with critical illnesses. In such cases, insurance companies may raise the premium for policyholders, and this increased premium is considered premium loading.

Life insurance companies also offer tax benefits to their customers. The premium paid by the policyholder comes under the tax deduction of section 80C in the Income Tax Act. Up to Rs. 1.5 lakh annual premium is a deductible amount from gross income that lowers the tax outgo. Moreover, the maturity insurance plans are totally tax-free.

Life insurance secures families by providing financial security in the event of the sudden death of a family member.

Understanding Investment-Linked Life Insurance: Maximizing Your Money

You may want to see also

Explore related products

![]()

Tax benefits: life insurance plans offer tax savings to policyholders

Life insurance companies make a profit by pooling risk from a payer and then redistributing that risk across a broader portfolio. They bet on the risk that their policyholders will not die, or their vehicles will not entirely smash, or their property will not get scorched. They make money by charging premiums for offering insurance coverage and reinvesting those premium amounts in other assets that generate interest.

Some policyholders are considered high-risk customers, for example, those in risky work such as the army, or those with critical illnesses. In these cases, insurance companies may raise the premium for policyholders, and this increased premium is considered as premium loading.

Life insurance plans also offer tax savings to policyholders. The premium paid by the policyholder comes under the tax deduction of section 80C in the Income Tax Act. So, up to Rs. 1.5 lakh annual premium is a deductible amount from gross income that lowers the tax outgo. Moreover, the maturity insurance plans are totally tax-free.

Life insurance secures families by providing financial security in the event of the sudden death of a family member.

Military Life Insurance: Discharge and Your Coverage

You may want to see also

Explore related products

![]()

General insurance: financial security in the form of compensation for losses other than death

Life insurance companies make a profit through premium loading, where they charge higher premiums to customers who are considered high-risk. This includes people in risky professions, such as the military, or those with critical illnesses or unhealthy habits like smoking or drinking. Life insurance companies also offer tax benefits to policyholders, allowing them to deduct their premium payments from their taxable income.

General insurance provides financial security in the form of compensation for losses other than death. It covers a range of liabilities, including travel, health, vehicle, and house-related issues. For example, if a person has general insurance and their vehicle is damaged, their insurance company is liable to pay for the repairs. Similarly, if a person suffers a financial loss while travelling, their insurance company may cover the financial loss. General insurance also provides protection against medical expenses and financial losses due to fire, theft, or natural disasters. By purchasing general insurance, individuals can gain peace of mind knowing that they will receive financial support in the event of unexpected losses or damages.

Heart Disease: USAA Life Insurance Underwriting Process and Duration

You may want to see also

Explore related products

$9.95 $19.95

$28.99 $44.99

![]()

Risk pooling: insurance companies redistribute risk across a broader portfolio

Life insurance companies make a profit by redistributing risk across a broader portfolio. This is known as risk pooling. Insurance companies bet that their policyholders will not die, that their vehicles will not be damaged, or that their property will not be destroyed. They agree to pay a specific amount of money for the loss of assets faced by the insured individual. In the process, they make money by charging premiums for offering insurance coverage and reinvesting those premium amounts in many other assets that generate interest.

Some policyholders are considered high-risk customers, such as those in risky work (e.g. the army, air force, etc.), people with critical illnesses, or those with unhealthy habits such as smoking or drinking. In these cases, insurance companies may raise the premium for policyholders, and this increased premium is considered premium loading.

Life insurance companies also offer tax benefits to their customers. The premium paid by the policyholder comes under the tax deduction of section 80C in the Income Tax Act. Up to Rs. 1.5 lakh annual premium is a deductible amount from gross income that lowers the tax outgo. Moreover, the maturity insurance plans are totally tax-free.

Life Insurance and Chronic Illness: What's Covered?

You may want to see also

Explore related products

![]()

Revenue generation: insurance companies make money by charging premiums and reinvesting in other assets

Life insurance companies make money by charging premiums and reinvesting in other assets. They bet on the risk that their policyholders will not die, or their vehicles will not be damaged, or their property will not be destroyed. The business model of insurance companies works by pooling risk from a payer and then redistributing that risk across a broader portfolio. In this, the insurance company agrees to pay a specific amount of money for the loss (mainly because of illness, damage, or death) of the assets faced by the insured individual.

Life insurance companies also make a profit or extra income through premium loading. Some insurance policyholders are considered high-risk customers, such as those in risky work (e.g. the army, pilots, air force) or people suffering from critical diseases or who are heavy smokers or drinkers. In such cases, insurance companies may raise the premium for policyholders, and this increased premium is considered premium loading.

Tax benefits are also offered in life insurance plans by insurance companies. The premium paid by the policyholder comes under the tax deduction of section 80C in the Income Tax Act. So, up to Rs. 1.5 lakh annual premium is a deductible amount from gross income that lowers the tax outgo. Moreover, the maturity insurance plans are totally tax-free.

Life insurance secures families by providing financial security even in the sudden death of a family member. It is a contract that provides financial security in the form of compensation for losses other than death. These financial losses can be related to different liabilities like travel, health, vehicles, and houses. Through this, insurance companies are liable to pay a sum assured of the compensation that covers vehicle damage, financial loss at the time of travel, medical expenses while taking treatment for health issues, and financial loss due to fire or theft or natural disasters.

Liquidity in Life Insurance: Understanding Cash Value and Options

You may want to see also

Frequently asked questions

Life insurance companies make money by charging premiums for offering insurance coverage and reinvesting those premium amounts in other assets that generate interest. They bet on the risk that their policyholders will not die, or their vehicles will not entirely smash, or their property will not get scorched.

Life insurance companies make a profit or extra income through premium loading. Some insurance policyholders are considered high-risk customers, such as those in risky work (e.g. the army, air force, etc.), people with critical illnesses, or chain smokers. In such cases, insurance companies may raise the premium for policyholders, and this increased premium is considered premium loading.

Life insurance provides financial security in the event of a sudden death in the family. It also offers tax benefits, as the premium paid by the policyholder is tax-deductible, and maturity insurance plans are tax-free.

More than half of European life policies guarantee an investment return to policyholders that exceeds the yield on the local ten-year government bond.