The life insurance market is a collection of companies and endeavours engaged in purchasing, selling, and managing life insurance policies. These policies are agreements between an insurance company and a policyholder, where the company agrees to pay premiums in exchange for the policyholder's beneficiary designation upon the covered person's death. The life insurance market is experiencing significant growth due to factors such as increasing awareness of financial security, technological advancements, and the expansion of the middle class. The market size is projected to reach USD 18.03 trillion by 2034, making it a lucrative industry for future investments.

| Characteristics | Values |

|---|---|

| Definition | A collection of companies and endeavours engaged in purchasing, selling, and managing life insurance policies. |

| Companies | Insurance companies |

| Customers | Policyholders |

| Agreement | Insurance company agrees to pay premiums in exchange for the policyholder's beneficiary designation upon the covered person's death. |

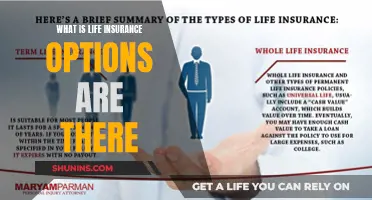

| Plans | Whole life, variable life, universal life, and term life insurance. |

| Purpose | To offer beneficiaries, typically family members, financial security in the event of the policyholder's death. |

| Financial security | Covers living expenses, debts, school tuition, and other financial commitments |

| Market size | USD 8.25 trillion in 2025, forecasted to reach USD 18.03 trillion by 2034. |

| Market growth | Driven by the expansion of the middle class in emerging markets, technological advancements, and evolving consumer demand. |

Explore related products

What You'll Learn

![]()

Life insurance policies

The life insurance market is a collection of companies and endeavours engaged in purchasing, selling, and managing life insurance policies. These policies are agreements between an insurance company and a policyholder. The insurance company agrees to pay premiums in exchange for the policyholder's beneficiary designation upon the covered person's death.

There are various types of life insurance plans available on the market, each addressing distinct financial needs and objectives. Whole life insurance provides coverage for the entire life of the insured, while variable life insurance offers flexible premiums and death benefits. Universal life insurance combines protection with a savings component, and term life insurance provides coverage for a specified period.

The demand for life insurance products is driven by several factors, including the growing awareness of financial security and long-term planning, the expansion of the middle class, and the increase in disposable income. Technological advancements, such as AI-driven underwriting and digital policy administration, have also improved the customer experience and market penetration, contributing to the significant growth of the life insurance market.

Overall, life insurance policies play a crucial role in safeguarding families and guaranteeing financial stability during difficult times. By providing peace of mind and financial protection, these policies ensure that loved ones are taken care of, even in the absence of the policyholder.

Smokers' Life Insurance: Is It Possible?

You may want to see also

Explore related products

![Life and Health Insurance Study Cards: Life Health Insurance License Exam Prep with Practice Test Questions [Full Color]](https://m.media-amazon.com/images/I/51Pox87Z5lL._AC_UY218_.jpg)

![]()

Financial security

The life insurance market is a collection of companies and endeavours engaged in purchasing, selling, and managing life insurance policies. These policies are agreements between an insurance company and a policyholder. The insurance company agrees to pay premiums in exchange for the policyholder's beneficiary designation upon the covered person's death.

Life insurance is deeply engrained in culture as a vital financial tool for safeguarding families and guaranteeing financial stability in the event of an insured person's passing. Various plans on the market address distinct financial needs and objectives, including whole life, variable life, universal life, and term life insurance. In the case of the policyholder's passing, life insurance offers beneficiaries, typically family members, financial security. This can cover living expenses, debts, school tuition, and other financial commitments.

The life insurance market is experiencing substantial growth as a result of the growing awareness of financial security and long-term planning. The demand for life coverage products is being driven by the increasing middle-class population and the increase in disposable income. Furthermore, the customer experience and market penetration are being improved by technological advancements such as AI-driven underwriting, digital policy administration, and automated claims processing.

The integration of digital technologies, such as AI and IoT, is also optimising operational workflows and enhancing product capabilities. Government initiatives promoting sustainable solutions and industry-standard regulations are also playing a crucial role in the market's growth. The increasing investment in research and development by key market players is fostering new product innovations and expanding market opportunities. Overall, these factors collectively contribute to the steady rise of the life insurance market, making it a lucrative industry for future investments.

Whole Life Insurance: Maximizing Benefits for You and Your Family

You may want to see also

Explore related products

![]()

Technological advancements

The life insurance market is a collection of companies and endeavours engaged in purchasing, selling, and managing life insurance policies. These policies are agreements between an insurance company and a policyholder, whereby the insurance company agrees to pay premiums in exchange for the policyholder's beneficiary designation upon the covered person's death. Technological advancements have played a significant role in the expansion of the life insurance market.

AI and IoT integration have optimised operational workflows and enhanced product capabilities. For example, AI-driven underwriting, digital policy administration, and automated claims processing have improved the customer experience and market penetration.

Additionally, the increasing middle-class population and their increase in disposable income have driven the demand for life coverage products. This has resulted in substantial growth in the life insurance market, as people view life insurance as a vital financial tool for safeguarding their families and guaranteeing financial stability in the event of their passing.

Government initiatives promoting sustainable solutions and industry-standard regulations have also contributed to the market growth. The life insurance market is expected to witness significant growth from 2025 to 2032, driven by market dynamics, technological advancements, and evolving consumer demand.

Child Life Insurance: Employer-Provided Coverage Explained

You may want to see also

Explore related products

![]()

Market growth

The life insurance market is a collection of companies and endeavours engaged in purchasing, selling, and managing life insurance policies. These policies are agreements between an insurance company and a policyholder, with the insurance company agreeing to pay premiums in exchange for the policyholder's beneficiary designation upon the covered person's death.

The life insurance market is experiencing significant growth, with the global market size projected to reach USD 18.03 trillion by 2034, up from USD 8.25 trillion in 2025, representing a CAGR of 9.10% during this period. This growth is driven by several factors, including:

- Rising awareness about the benefits of life insurance: People are increasingly recognising the importance of life insurance as a vital financial tool for safeguarding families and guaranteeing financial stability in the event of an insured person's passing. This shift in perception is driving more individuals to purchase life insurance policies.

- Expanding applications across sectors: Life insurance is no longer limited to traditional sectors but is finding applications in diverse industries such as healthcare, automotive, and electronics. This expansion into new sectors is contributing to the overall growth of the life insurance market.

- Technological advancements: The integration of digital technologies, such as AI, IoT, and automated claims processing, is optimising operational workflows, enhancing product capabilities, and improving customer experiences. These advancements are attracting new customers and increasing market penetration, leading to market growth.

- Government initiatives: Government policies promoting sustainable solutions and industry-standard regulations are also playing a crucial role in market expansion. These initiatives provide a supportive framework for the life insurance industry to thrive and attract investments.

- Middle-class expansion and increasing disposable income: The growth of the middle class, particularly in emerging markets, is a key driver of life insurance demand. As more individuals enter the middle class, they seek financial security and long-term planning, making life insurance an attractive option. Additionally, increasing disposable income enables more people to afford life insurance policies, further boosting market growth.

Life Insurance: Understanding Payout Timelines and Delays

You may want to see also

Explore related products

![]()

Government initiatives

The life insurance market is a collection of companies and endeavours engaged in purchasing, selling, and managing life insurance policies. These policies are agreements between an insurance company and a policyholder, whereby the company agrees to pay premiums in exchange for the policyholder's beneficiary designation upon the covered person's death.

Additionally, the life insurance market is experiencing substantial growth due to the growing awareness of financial security and long-term planning. The demand for life coverage products is being driven by the increasing middle-class population and the increase in disposable income. Technological advancements, such as AI-driven underwriting, digital policy administration, and automated claims processing, are also improving customer experience and market penetration.

The global life insurance market size is forecasted to reach USD 18.03 trillion by 2034, with a CAGR of 9.10% from 2025 to 2034. This growth is attributed to the expansion of the middle class in emerging markets and the increasing investment in research and development by key market players, fostering new product innovations and expanding market opportunities.

Life Insurance and Medicare: Retirement's Dynamic Duo

You may want to see also

Frequently asked questions

The life insurance market is a collection of companies and endeavours engaged in purchasing, selling, and managing life insurance policies.

The global life insurance market size is projected to reach USD 18.03 trillion by 2034.

The life insurance market is experiencing substantial growth due to the growing awareness of financial security and long-term planning. The demand for life coverage products is being driven by the increasing middle-class population and the increase in disposable income.

Various plans on the market address distinct financial needs and objectives, including whole life, variable life, universal life, and term life insurance.

Life insurance policies are agreements between an insurance company and a policyholder. The insurance company agrees to pay premiums in exchange for the policyholder's beneficiary designation upon the covered person's death. Life insurance offers beneficiaries, typically family members, financial security by covering living expenses, debts, school tuition, and other financial commitments.