Life insurance is a contract between an insurance company and a policyholder. The purpose of life insurance is to provide financial security to the policyholder's loved ones after their death. However, some life insurance policies also offer living benefits, which can be used to pay for chronic illnesses or to help achieve financial goals.

| Characteristics | Values |

|---|---|

| Purpose | To provide financial security to your loved ones upon your death |

| To protect your family | |

| To achieve your financial goals | |

| To pay off debts | |

| To pay living expenses | |

| To pay medical or final expenses | |

| To pay for chronic illnesses | |

| To purchase coverage for your children |

Explore related products

What You'll Learn

![]()

Financial security for your loved ones

Life insurance is a contract between an insurance company and a policyholder. In exchange for a premium, the life insurance company agrees to pay a sum of money to one or more named beneficiaries upon the death of the policyholder. The purpose of life insurance is to help provide financial security to your loved ones upon your death. This can help to pay off debts, living expenses, and medical or final expenses.

Some life insurance policies also offer living benefits, which means they can pay a part of the policy's death benefit while you're still alive. These policies can be a financial resource if you're diagnosed with a covered illness that's considered chronic, critical, or terminal. For an additional cost, you can also purchase additional protection to pay your premiums if you become disabled, to use some of your face amount to pay for chronic illnesses, or to purchase coverage for your children.

Universal life insurance provides a lifetime of coverage and can build cash value over time. This type of policy also gives flexibility when it comes to making payments. For example, if you have enough cash value in your policy, you can use that money to skip a premium payment. Variable life is another type of permanent life insurance that can build cash value and has the potential to increase the value of certain subaccounts within the policy for even greater growth potential over time.

Ladder's Whole Life Insurance: Is It Worth the Climb?

You may want to see also

Explore related products

![]()

Protection for your family

Life insurance is a contract between an insurance company and a policyholder. In exchange for a premium, the insurance company agrees to pay a sum of money to one or more named beneficiaries upon the death of the policyholder. The purpose of life insurance is to provide financial security to your loved ones upon your death. This can help to pay off debts, living expenses, and medical or final expenses.

Life insurance can also offer living benefits. This means that they can pay a part of the policy's death benefit while you're still alive. These policies can be a financial resource if you're diagnosed with a covered illness that's considered chronic, critical, or terminal.

You can also purchase additional protection to pay your premiums if you become disabled, to use some of your face amount to pay for chronic illnesses, or to purchase coverage for your children.

Aflac Life Insurance: Is It Worth the Cost?

You may want to see also

Explore related products

![]()

Paying off debts

Life insurance is a contract between an insurance company and a policyholder. In exchange for a premium, the insurance company agrees to pay a sum of money to one or more named beneficiaries upon the death of the policyholder. The purpose of life insurance is to provide financial security to your loved ones upon your death. This can help to pay off debts, living expenses, and medical or final expenses.

Life insurance can be used to pay off debts after the policyholder's death. This can include credit card debt, mortgage payments, or other loans. By naming a beneficiary, such as a spouse or child, the policyholder can ensure that their loved ones are not burdened with these debts.

Life insurance can also help to pay off debts while the policyholder is still alive. Some policies offer living benefits, which means they can pay a part of the policy's death benefit while the policyholder is still alive. These benefits can be used to pay off debts or cover living expenses.

Additionally, riders can be purchased for an additional cost to provide further protection. For example, a rider can be used to pay premiums if the policyholder becomes disabled or to cover chronic illnesses. This can help to reduce financial strain and ensure that debts are paid off.

Universal life insurance policies can also provide flexibility when it comes to making payments. If there is enough cash value in the policy, the money can be used to skip a premium payment. This can free up funds to pay off debts or cover other expenses.

Overall, life insurance can be a valuable tool to help pay off debts and provide financial security for loved ones. By naming beneficiaries and taking advantage of living benefits, riders, and flexible payment options, policyholders can ensure that their debts are covered in the event of their death or disability.

Do E-Cigs Affect Your Life Insurance Premiums?

You may want to see also

Explore related products

![]()

Living expenses

Life insurance is a contract between an insurance company and a policyholder. In exchange for a premium, the life insurance company agrees to pay a sum of money to one or more named beneficiaries upon the death of the policyholder. The purpose of life insurance is to provide financial security to your loved ones upon your death. However, some life policies also offer living benefits. This means they can pay a part of the policy's death benefit while you're still alive. These policies can be a financial resource you can use if you're diagnosed with a covered illness that's considered chronic, critical, or terminal.

Brokers and Life Insurance Rates: Do They Vary?

You may want to see also

Explore related products

![]()

Medical or final expenses

Life insurance is a contract between an insurance company and a policyholder. In exchange for a premium, the insurance company agrees to pay a sum of money to one or more named beneficiaries upon the death of the policyholder. The purpose of life insurance is to provide financial security to your loved ones upon your death.

Life insurance can also be used to help with medical or final expenses. This means that if you are diagnosed with a covered illness that is considered chronic, critical, or terminal, your policy can pay out a part of the death benefit while you are still alive. This can be used to help with the cost of medical treatment and other living expenses.

Some life insurance policies also offer additional protection for an extra cost. This can include coverage for chronic illnesses or disabilities, which can help to pay for medical expenses. You can also purchase coverage for your children, which can provide financial security for them in the event of your death.

Life insurance can provide peace of mind, knowing that your loved ones will be taken care of financially if something happens to you. It can help to pay off debts, living expenses, and any other final expenses that may arise.

Independent Life Insurance Agents: What You Need to Know

You may want to see also

Frequently asked questions

Life insurance is used to provide financial security to your loved ones upon your death.

Yes, some life insurance policies also offer living benefits. This means they can pay out a part of the policy's death benefit while you're still alive. These policies can be a financial resource if you're diagnosed with a covered illness that's considered chronic, critical, or terminal.

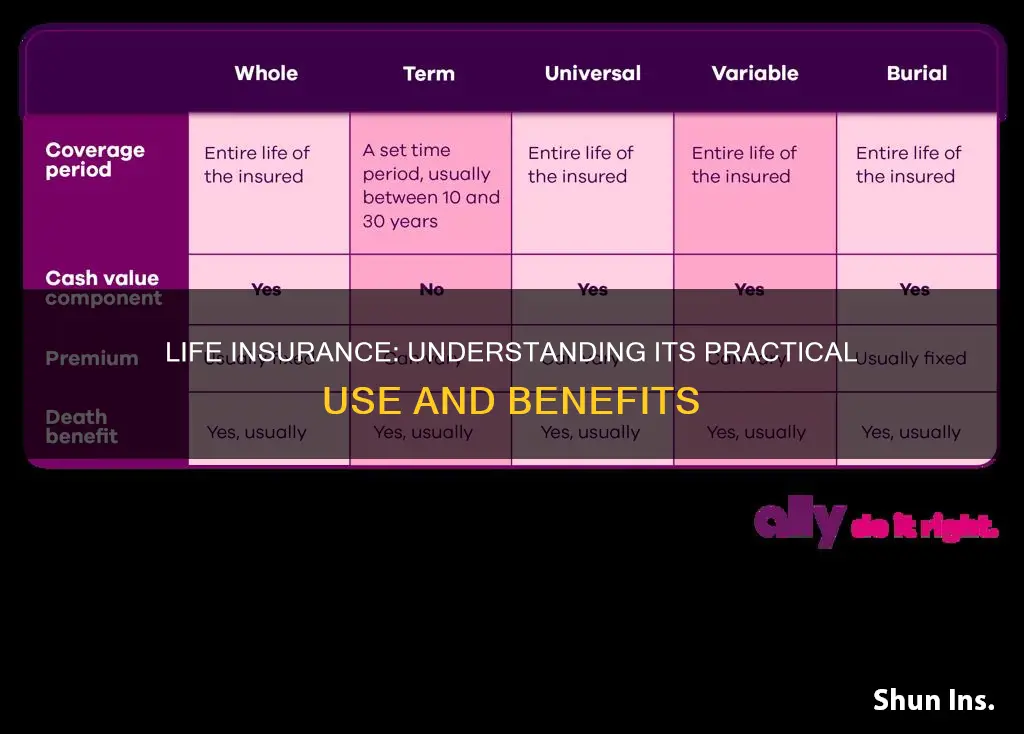

There are several types of life insurance, including whole life, universal life, and variable life. Whole life insurance provides a lifetime of coverage and can build cash value over time. Universal life insurance offers the same benefits as whole life but with more flexibility when it comes to making payments. Variable life insurance has the potential to increase the value of certain subaccounts within the policy for greater growth potential over time.