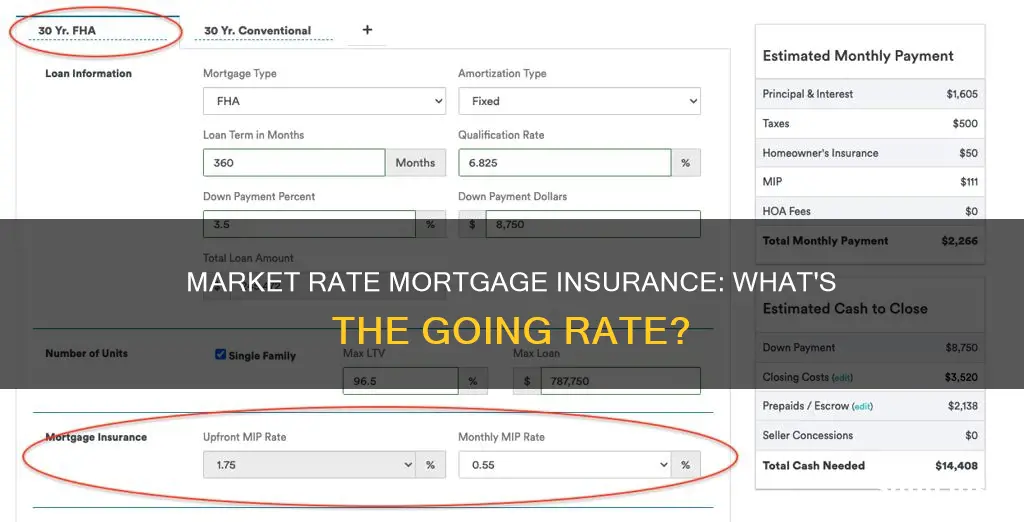

Private mortgage insurance (PMI) is an extra fee for a conventional mortgage for borrowers putting less than 20% down. The amount you pay for PMI depends on several factors, including the size of your loan, your down payment amount, debt-to-income ratio, credit score, and loan type. The average cost of PMI for a conventional home loan ranges from 0.46% to 1.5% of the original loan amount per year, but the mortgage insurance rate can be anywhere from 0.2% to 2% of the loan amount per year. PMI can be paid monthly with your mortgage payment, upfront as a full premium amount for the year, or a combination of both. Lender-paid mortgage insurance is when the lender covers the cost of PMI, but this usually results in a higher interest rate on the loan.

| Characteristics | Values |

|---|---|

| Definition | Private mortgage insurance (PMI) is an extra fee for a conventional mortgage for borrowers putting less than 20% down. |

| Who pays for it? | Borrower-paid PMI is the typical type of PMI. With lender-paid PMI, the lender pays the premiums, but you'll pay a higher interest rate on the loan. |

| Cost | The average cost of PMI for a conventional home loan ranges from 0.46% to 1.5% of the original loan amount per year, according to the Urban Institute's Housing Finance Policy Center. |

| Factors affecting cost | The amount you'll pay for PMI depends on several factors, including the size of your loan, your down payment amount, debt-to-income ratio, loan type, and credit score. |

| Avoiding PMI | You can avoid PMI by putting 20% down on a conventional mortgage, choosing a single premium PMI, or requesting its removal once your mortgage balance is 80% of the value of your home. |

Explore related products

What You'll Learn

![]()

Lender-paid mortgage insurance

LPMI is advantageous for homebuyers who plan to live in their home for a short period of time. If you only plan to live in your new home for a few years, you likely won't reach the 20% equity mark needed to cancel the monthly PMI. It is also beneficial for high-income earners as mortgage interest is deductible on federal taxes.

LPMI is also a good option for buyers who don't have enough savings to cover a 20% down payment. By choosing LPMI, borrowers can keep their monthly payments affordable and get into a challenging housing market even if they haven't amassed a large amount of cash.

There are a few ways to avoid paying mortgage insurance altogether. One option is to put 20% down on a conventional mortgage, as this will eliminate the need for mortgage insurance. Another option is to choose a single premium PMI, which allows you to make a single payment to remove the PMI from a conventional mortgage. You can also request the removal of PMI once your mortgage balance reaches 80% of your home's value.

It's important to note that LPMI may not always be the most cost-effective option. While it can lower your monthly payments, it may cost you more in the long run due to the higher interest rate. It's essential to compare different lenders and loan programs to find the most suitable option for your financial situation.

Switching Lanes: Exploring the Impact of Auto Insurance Company Changes on Rates

You may want to see also

Explore related products

![]()

Borrower-paid mortgage insurance

BPMI is paid monthly as part of the borrower's mortgage payment. The monthly cost of BPMI varies depending on several factors, including the size of the loan, the down payment amount, the debt-to-income ratio, and the borrower's credit score. On average, BPMI costs $30 to $70 per month for every $100,000 borrowed. For example, for a $300,000 mortgage, BPMI would cost $1,380 to $4,500 per year, or $115 to $375 per month.

Borrowers can request to cancel BPMI when they have achieved 20% equity in their home. BPMI can also be cancelled under the Homeowners Protection Act of 1998 (HPA). Additionally, borrowers can qualify for BPMI cancellation sooner by making extra payments that reduce the mortgage balance or by making home improvements that increase the appraised value of the property.

BPMI single premium options are available for borrowers who want to keep their monthly payments low. With this option, the borrower or another party, such as the seller or builder, pays the full premium upfront at closing or finances it into the loan. The BPMI single premium option can be refundable or non-refundable, with partial refunds available under certain conditions.

Overall, BPMI provides borrowers with the flexibility to secure a loan with a smaller down payment, but it comes at an additional cost that varies depending on various factors. It is important for borrowers to carefully consider their financial situation and seek professional advice before committing to BPMI or any other type of mortgage insurance.

Nevada License, California Insurance: Legal?

You may want to see also

Explore related products

$29.99 $29.99

$12.33 $12.99

![]()

Mortgage rate locks

A mortgage rate lock is a commitment or guarantee from a lender to hold a specific interest rate for a set period, usually during the loan application process. This ensures that even if market rates increase before your loan closes, you will still get the lower, locked rate. Rate locks typically last between 30 and 60 days, but longer periods of up to 90 or 120 days may be available for an additional cost.

The lock period is the duration during which a mortgage rate is secured against fluctuations in interest rates. If the lock period expires before closing, the borrower might need to manage costs or re-lock at a new rate. A rate lock does not ensure that your loan will be approved, and it may be expensive to extend if more time is needed. Your rate lock agreement should be long enough to cover the time until you close on your loan.

A standard rate lock does not allow you to take advantage of falling rates. However, some lenders offer a ""float down" option, which allows you to secure a lower rate if rates fall during your lock period. This option often comes with a fee or a higher initial rate.

Understanding when and how to lock your rate can save you money over the life of your loan. Your mortgage professional can provide insights on market trends and optimal timing.

Best Auto Insurance Companies for Easy Claims

You may want to see also

Explore related products

![]()

Factors influencing insurance rates

Private mortgage insurance (PMI) is an extra fee for a conventional mortgage for borrowers who put down less than 20% of the total home price. The amount paid for PMI depends on several factors, which influence insurance rates. These factors include the size of the loan, the down payment amount, the type of loan, and the borrower's credit score.

The size of the down payment is inversely proportional to the PMI cost. A larger down payment results in a lower PMI, and borrowers can avoid the PMI expense altogether if they put down 20% of the home price. The type of loan also impacts the PMI, with adjustable-rate mortgages (ARMs) typically carrying a higher PMI than fixed-rate loans due to the increased risk for lenders.

The borrower's credit score is another critical factor. Those with higher credit scores tend to pay lower PMI rates, while lower credit scores result in higher rates. This is because a higher credit score indicates lower risk for the lender. Additionally, the borrower's debt-to-income ratio plays a role, with lower ratios corresponding to lower PMI rates.

Lender-paid mortgage insurance is an alternative where the lender covers the PMI, but this usually results in a higher interest rate on the loan. This option may be beneficial for buyers who cannot afford a 20% down payment. Overall, these factors, including the loan characteristics and the borrower's financial profile, influence the insurance rates for PMI.

Illinois Auto Insurance: What's the Cost?

You may want to see also

Explore related products

![]()

Mortgage protection insurance

MPI is not as flexible as other types of insurance like disability insurance and life insurance. This is because the payment goes directly to your mortgage lender to pay off the loan, rather than to your beneficiaries. MPI policies can often be purchased from banks and mortgage lenders, and they cover only the principal and interest portion of a mortgage payment. The amount you pay for MPI depends on factors including the insurer and the current balance of your mortgage.

MPI can be a good choice if you have unstable employment and may need assistance paying your mortgage in the future. It is also an option for those who do not qualify for or cannot afford a traditional life insurance policy, as it does not require a medical evaluation for approval. However, MPI premiums are often much higher than term life insurance premiums.

There are several alternatives to MPI. If your mortgage has a low-interest rate and your loved ones can afford to live without your income, a traditional life insurance policy may be preferable. This is because the payout goes directly to your beneficiaries, who can then choose how to allocate the money. Additionally, your loved ones may be able to take advantage of mortgage-related tax advantages, such as the mortgage interest deduction, if they do not have a mortgage protection policy.

Understanding Auto Insurance Medical Coverage

You may want to see also

Frequently asked questions

Mortgage insurance, also known as private mortgage insurance (PMI), is an extra fee for a conventional mortgage for borrowers putting less than 20% down. It protects the lender in case the buyer defaults on their loan.

The average cost of PMI for a conventional home loan ranges from 0.46% to 1.5% of the original loan amount per year, according to the Urban Institute's Housing Finance Policy Center. The amount varies depending on factors such as the size of your loan, your down payment amount, debt-to-income ratio, and credit score.

Borrower-paid mortgage insurance (BPMI) is the typical type of PMI, where the cost of PMI is added to the borrower's monthly payment. Lender-paid mortgage insurance, also known as a no-PMI loan, is when the lender covers the cost of PMI, but the borrower pays a higher interest rate on the loan.

Yes, if you put at least 20% down on a conventional mortgage, you won't have to pay for mortgage insurance. You can also request to cancel PMI when your mortgage balance reaches 80% of your home's value.

You can use a PMI calculator to estimate the cost of PMI. Factors such as your loan type, down payment amount, credit score, and interest rate will impact your PMI payments.