Pure insurance, also known as pure risk insurance, refers to coverage designed to protect against financial losses resulting from events that are entirely beyond the policyholder's control, such as natural disasters, accidents, or theft. Unlike speculative risks, which involve potential for both gain and loss, pure risks only carry the possibility of loss or no loss. This type of insurance is fundamental to risk management, as it provides individuals and businesses with financial security by transferring the risk of unforeseen events to an insurer in exchange for premiums. Pure insurance policies are typically straightforward, focusing on indemnifying the policyholder for actual losses incurred, without any profit motive for the insured. Examples include home, auto, and life insurance, which aim to restore the policyholder to their pre-loss financial state rather than providing an opportunity for gain.

| Characteristics | Values |

|---|---|

| Definition | A type of insurance where the insurer agrees to pay a specified amount upon the occurrence of a defined event, without any savings or investment component. |

| Purpose | To provide financial protection against specific risks, ensuring policyholders receive a predetermined benefit if the insured event occurs. |

| Examples | Term life insurance, accidental death and dismemberment insurance, and certain types of property insurance. |

| Premium Structure | Premiums are calculated based on the likelihood of the insured event occurring and the cost of providing the coverage. |

| Benefit Payment | Fixed amount paid upon the occurrence of the insured event, as outlined in the policy. |

| Duration | Typically for a specified term or until the insured event occurs, with no cash value accumulation. |

| Risk Transfer | Transfers the financial risk of the insured event from the policyholder to the insurer. |

| No Investment Component | Does not include any savings or investment features, focusing solely on risk coverage. |

| Tax Treatment | Premiums are generally not tax-deductible, and benefits paid are usually tax-free. |

| Regulatory Environment | Subject to insurance regulations, ensuring consumer protection and solvency of insurers. |

| Common Misconception | Often confused with investment-linked insurance products, but pure insurance is strictly risk-based. |

Explore related products

$15.95

$12.99 $14.95

$109.76

What You'll Learn

- Definition of Pure Insurance: Coverage for specific risks with no savings or investment component included

- Purpose of Pure Insurance: Protects against financial loss from defined events, ensuring risk mitigation

- Types of Pure Insurance: Includes term life, liability, property, and health insurance policies

- Key Features: Fixed premiums, defined coverage limits, and no cash value accumulation

- Examples of Pure Insurance: Auto liability, renters insurance, and catastrophic health plans

![]()

Definition of Pure Insurance: Coverage for specific risks with no savings or investment component included

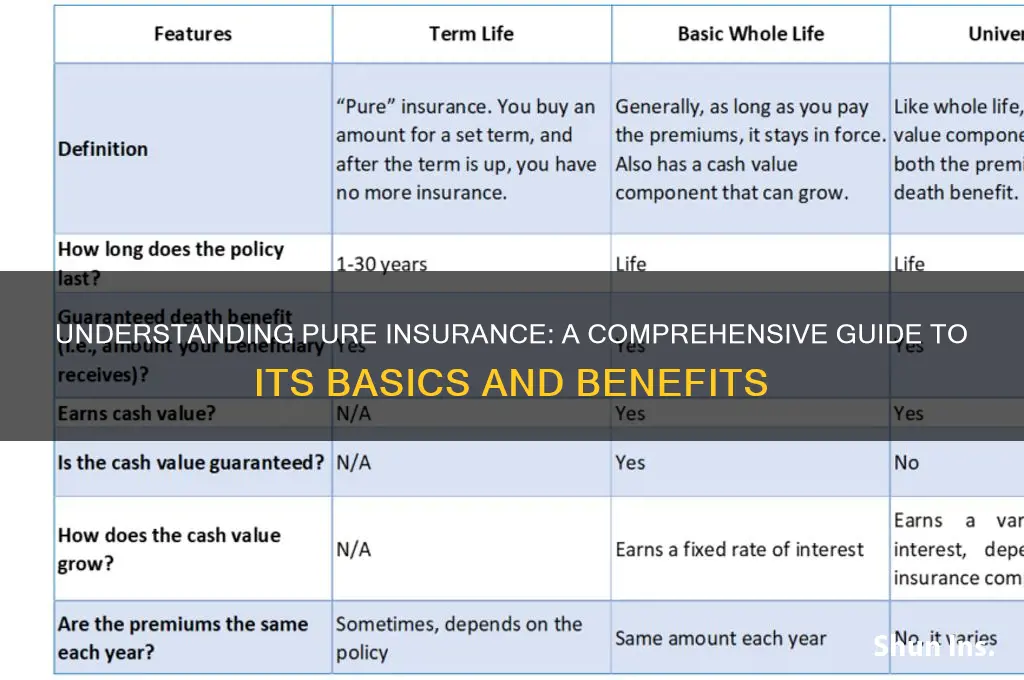

Pure insurance, often referred to as "pure risk insurance," is a type of coverage designed solely to protect against specific, defined risks without incorporating any savings or investment elements. Unlike other insurance products that may include a savings or investment component, such as whole life insurance or annuities, pure insurance focuses exclusively on providing financial protection in the event of a covered loss. This means that the policyholder pays premiums in exchange for the insurer’s promise to compensate for losses resulting from the specified risks, with no expectation of accumulating cash value or earning investment returns over time.

The core purpose of pure insurance is to transfer the financial burden of potential losses from the policyholder to the insurer. This is achieved by pooling risks among a large number of policyholders, allowing the insurer to spread the cost of individual claims across the group. Common examples of pure insurance include term life insurance, which provides death benefit coverage for a specified period, and property insurance, which protects against damage or loss of physical assets like homes or vehicles. In both cases, the coverage is straightforward: it addresses specific risks without offering additional financial benefits beyond the protection itself.

One key characteristic of pure insurance is its focus on "pure risks," which are events that carry only the possibility of loss or no loss, with no opportunity for gain. Examples of pure risks include natural disasters, accidents, or premature death. Pure insurance does not cover speculative risks, where there is a chance of gain or profit, such as investments in stocks or real estate. By limiting coverage to pure risks, pure insurance maintains its simplicity and clarity, ensuring that policyholders understand exactly what is covered and what is not.

Another important aspect of pure insurance is its transparency in terms of costs and benefits. Since there is no savings or investment component, premiums are calculated based solely on the likelihood and potential severity of the covered risks. This makes pure insurance generally more affordable than products that include savings or investment features. Policyholders pay for the protection they need without contributing to additional financial goals, making it an efficient option for those seeking straightforward risk mitigation.

In summary, the definition of pure insurance centers on its role as a financial tool that provides coverage for specific risks without including any savings or investment component. It is designed to address pure risks—events that offer only the possibility of loss—and operates by transferring the financial impact of these risks from the policyholder to the insurer. By focusing exclusively on risk protection, pure insurance offers clarity, affordability, and efficiency, making it a valuable option for individuals and businesses seeking targeted financial security.

Cancer and Life Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

Purpose of Pure Insurance: Protects against financial loss from defined events, ensuring risk mitigation

Pure insurance, also known as "pure risk insurance," serves a fundamental purpose in the realm of risk management: it protects individuals and businesses against financial loss arising from specific, defined events. Unlike speculative risks, which involve potential for both gain and loss, pure risks are those that only carry the possibility of loss or no loss at all. Examples include natural disasters, accidents, theft, or death. The primary objective of pure insurance is to transfer the financial burden of these unforeseen events from the policyholder to the insurer, ensuring that the insured party can maintain financial stability in the face of adversity. By doing so, pure insurance acts as a critical tool for risk mitigation, providing a safety net that allows individuals and organizations to operate with greater confidence and security.

The purpose of pure insurance is deeply rooted in its ability to provide financial protection against events that are beyond human control. For instance, a homeowner’s insurance policy covers losses from fire, storms, or burglary, ensuring that the policyholder is not left financially devastated by such events. Similarly, life insurance protects a policyholder’s dependents by providing a financial payout in the event of the insured’s death. This protection is essential because these events, while unpredictable, can have catastrophic financial consequences. Pure insurance ensures that the insured party can recover from such losses without facing long-term financial hardship, thereby preserving their economic well-being.

Another key aspect of pure insurance is its role in fostering economic stability and continuity. For businesses, pure insurance policies such as property insurance, liability insurance, or business interruption insurance safeguard against disruptions that could otherwise lead to significant financial losses or even bankruptcy. By mitigating these risks, businesses can focus on their core operations without the constant fear of unforeseen events derailing their progress. This stability extends to the broader economy, as insured businesses are better equipped to withstand shocks and continue contributing to economic growth. In this way, pure insurance not only protects individual entities but also plays a vital role in maintaining the resilience of entire industries and economies.

Pure insurance is also designed to be straightforward and transparent, focusing solely on providing coverage for pure risks without incorporating investment or savings components. This clarity ensures that policyholders understand the exact nature of the protection they are purchasing, allowing them to make informed decisions about their risk management strategies. Unlike other financial products that may combine insurance with investment features, pure insurance remains focused on its core purpose: risk mitigation. This simplicity makes it an accessible and effective tool for individuals and businesses alike, enabling them to tailor their coverage to specific needs and potential threats.

In summary, the purpose of pure insurance is to protect against financial loss from defined events, ensuring effective risk mitigation. By transferring the financial burden of pure risks to insurers, pure insurance provides a critical safety net for individuals and businesses, allowing them to navigate uncertainties with greater confidence. Its focus on specific, uncontrollable events, combined with its transparency and simplicity, makes it an indispensable component of personal and corporate risk management strategies. Through pure insurance, policyholders can safeguard their financial future, maintain stability, and focus on their long-term goals without being unduly hindered by the potential for loss.

Insurance Simplified: A-Win Insurance Bonnyville

You may want to see also

Explore related products

![]()

Types of Pure Insurance: Includes term life, liability, property, and health insurance policies

Pure insurance, also known as "pure risk" insurance, is designed to protect against financial losses resulting from events that are beyond the policyholder's control and do not provide any opportunity for gain. Unlike speculative risks, which involve the possibility of both profit and loss, pure risks only involve the potential for loss. The primary purpose of pure insurance is to provide financial security and peace of mind by transferring the risk from the individual to the insurer. Below are the key types of pure insurance policies, including term life, liability, property, and health insurance, each serving distinct purposes and addressing specific risks.

Term Life Insurance is a type of pure insurance that provides coverage for a specified period, typically 10, 20, or 30 years. It is designed to offer a death benefit to the policyholder's beneficiaries if the insured passes away during the term. Term life insurance is straightforward and affordable, making it an ideal choice for individuals seeking temporary coverage to protect their loved ones from financial hardship. Unlike whole life insurance, it does not accumulate cash value, focusing solely on providing a safety net in the event of premature death. This policy is particularly useful for covering debts, mortgage payments, or future expenses like education.

Liability Insurance protects individuals and businesses from financial loss due to claims of negligence or harm caused to others. This type of pure insurance covers legal costs, medical expenses, and damages awarded in lawsuits. Personal liability insurance, often included in homeowners or renters policies, safeguards against accidents that occur on your property. Auto liability insurance, on the other hand, covers bodily injury and property damage caused by the policyholder while driving. For businesses, general liability insurance protects against claims related to operations, products, or services. Liability insurance is essential for mitigating the financial impact of lawsuits and ensuring compliance with legal requirements.

Property Insurance is designed to protect physical assets, such as homes, vehicles, and personal belongings, from damage or loss due to perils like fire, theft, or natural disasters. Homeowners insurance, for instance, covers the structure of the home and personal property, while also providing liability protection. Renters insurance protects tenants' belongings and offers liability coverage. Auto insurance safeguards vehicles against accidents, theft, and damage. Property insurance policies typically include both replacement cost and actual cash value options, allowing policyholders to choose the level of coverage that best suits their needs. This type of pure insurance ensures that individuals can recover financially from unexpected events that damage or destroy their assets.

Health Insurance is a critical form of pure insurance that covers medical expenses incurred due to illness, injury, or preventive care. Policies vary widely, ranging from comprehensive plans that cover a broad range of services to more limited plans focused on specific needs. Health insurance can include coverage for doctor visits, hospital stays, prescription medications, and specialized treatments. Many policies also offer preventive care benefits, such as vaccinations and screenings, to promote long-term health. With the rising cost of healthcare, health insurance is essential for protecting individuals and families from exorbitant medical bills. It ensures access to necessary care while providing financial stability during health-related crises.

In summary, pure insurance encompasses term life, liability, property, and health insurance policies, each tailored to address specific risks and provide financial protection. Term life insurance offers temporary coverage for death benefits, liability insurance shields against legal claims, property insurance safeguards physical assets, and health insurance covers medical expenses. Together, these types of pure insurance form a comprehensive safety net, helping individuals and businesses manage risks effectively and achieve peace of mind. Understanding the distinctions between these policies allows policyholders to make informed decisions and select the coverage that best meets their needs.

JLo's Legs: Insured Assets or Natural Beauty?

You may want to see also

Explore related products

![]()

Key Features: Fixed premiums, defined coverage limits, and no cash value accumulation

Pure insurance, often referred to as term insurance, is a straightforward and essential financial tool designed to provide protection without additional investment components. One of its key features is fixed premiums, which means policyholders pay a consistent amount throughout the term of the policy. This predictability allows individuals to budget effectively, knowing their insurance costs will not fluctuate unexpectedly. Fixed premiums are typically lower compared to other types of insurance, such as whole life or universal life policies, because they are solely focused on providing coverage rather than building cash value. This makes pure insurance an affordable option for those seeking temporary or specific coverage needs.

Another critical aspect of pure insurance is defined coverage limits. The policy clearly outlines the maximum amount the insurer will pay in the event of a claim. This transparency ensures policyholders understand the extent of their protection and can align it with their specific risks or financial obligations. For example, a pure insurance policy might cover a specific liability amount or provide a predetermined death benefit. Defined coverage limits help avoid misunderstandings and ensure that both the insurer and the insured are on the same page regarding the scope of protection.

A distinguishing feature of pure insurance is no cash value accumulation. Unlike permanent life insurance policies, which include an investment component that builds cash value over time, pure insurance is purely protective. This means that the policy does not accumulate any monetary value beyond the coverage it provides. At the end of the term, if no claims have been made, the policy simply expires, and no cash is returned to the policyholder. This absence of cash value accumulation keeps the premiums lower and the product focused on its primary purpose: providing financial protection against specific risks.

The combination of fixed premiums, defined coverage limits, and no cash value accumulation makes pure insurance a highly efficient and cost-effective solution for individuals and businesses. It is particularly suited for those who need coverage for a specific period, such as to protect a mortgage, cover a business loan, or provide for dependents until they become financially independent. By eliminating the investment component, pure insurance ensures that policyholders pay only for the protection they need, without unnecessary additional costs.

In summary, pure insurance stands out for its simplicity and focus on core protection. Its fixed premiums offer financial stability, defined coverage limits provide clarity, and no cash value accumulation ensures affordability and purpose-driven functionality. These features make it an ideal choice for those seeking straightforward, temporary, and cost-effective insurance solutions. Understanding these key aspects helps individuals make informed decisions about whether pure insurance aligns with their financial goals and risk management needs.

Life Insurance: Longest-Term Policies and Their Benefits

You may want to see also

Explore related products

![]()

Examples of Pure Insurance: Auto liability, renters insurance, and catastrophic health plans

Pure insurance, also known as "true insurance," is a type of coverage designed to protect against risks that are purely speculative and not expected to provide any financial gain beyond indemnification. It focuses on safeguarding individuals and businesses from significant, unforeseen losses rather than offering investment opportunities or savings components. Below are detailed examples of pure insurance, including auto liability insurance, renters insurance, and catastrophic health plans, which align with the principles of pure insurance.

Auto liability insurance is a classic example of pure insurance. This coverage is mandatory in most jurisdictions and protects drivers from financial liability in the event they cause an accident resulting in bodily injury or property damage to others. The policy does not provide any direct benefit to the insured unless a covered event occurs. For instance, if a driver rear-ends another vehicle, their auto liability insurance would cover the medical expenses and repair costs of the other party, up to the policy limits. The insured pays premiums solely for this protection, with no expectation of a return on investment. This aligns with the pure insurance concept, as it addresses a specific risk without offering any additional financial benefits.

Renters insurance is another example of pure insurance, designed to protect tenants from financial losses related to their personal belongings and liability. This policy covers risks such as theft, fire, or water damage to the renter's possessions and provides liability coverage if someone is injured in the rented property. For example, if a fire damages a renter's furniture and clothing, the insurance would reimburse the policyholder for the loss. Similarly, if a guest slips and falls in the rented apartment, the liability portion of the policy would cover medical expenses and potential legal fees. Renters insurance is purely risk-focused, offering no savings or investment features, making it a clear example of pure insurance.

Catastrophic health plans also fall under the category of pure insurance, as they are designed to protect individuals from extremely high medical costs associated with severe illnesses or accidents. These plans typically have low premiums and high deductibles, providing coverage only after the insured has paid a significant amount out-of-pocket. For instance, a catastrophic health plan might cover hospitalization, emergency surgery, or other major medical expenses once the deductible is met. This type of insurance is not intended for routine healthcare needs but rather for unexpected, high-cost events. It embodies the principles of pure insurance by focusing solely on protection against catastrophic risks without offering any additional financial benefits or savings components.

In summary, auto liability insurance, renters insurance, and catastrophic health plans are prime examples of pure insurance. Each of these policies is designed to address specific, speculative risks without providing any financial gain beyond indemnification. They serve as essential tools for individuals and businesses to manage potential losses, ensuring financial stability in the face of unforeseen events. Understanding these examples highlights the core purpose of pure insurance: to offer protection against significant risks in a straightforward and focused manner.

New York Life Insurance: AARP Payouts, Quick and Easy?

You may want to see also

Frequently asked questions

Pure insurance, also known as "pure risk insurance," is a type of coverage designed to protect against financial losses resulting from events that are beyond the policyholder's control, such as natural disasters, accidents, or theft. It does not involve speculative risks or potential gains.

Pure insurance differs from other types, like investment-linked insurance, because it focuses solely on risk mitigation without any investment or savings component. Its primary purpose is to provide financial protection against unforeseen events.

Examples of pure insurance policies include homeowners insurance, auto insurance, health insurance, and liability insurance. These policies cover losses from events like fires, accidents, illnesses, or legal claims.

No, pure insurance does not offer returns or benefits beyond the coverage provided. Premiums paid are used to pool risks, and payouts are made only when a covered loss occurs. There is no investment or savings element.

Anyone seeking financial protection against unpredictable and potentially costly events should consider pure insurance. It is particularly important for individuals, families, and businesses looking to safeguard their assets and financial stability.