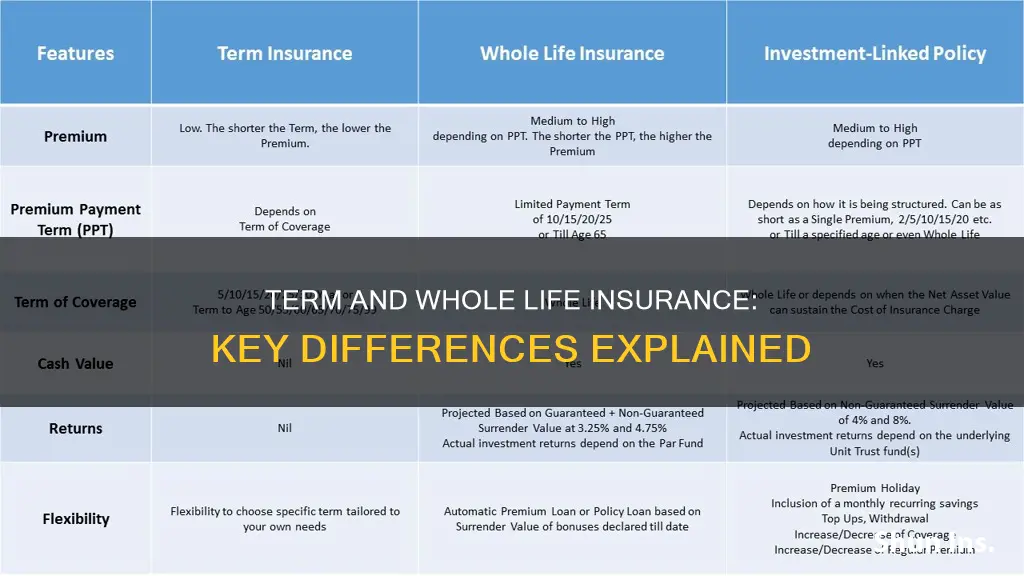

Term life insurance is a cheaper option that covers you for a set period of time, which is ideal if you need income replacement for a specific time, such as while raising children or paying off a mortgage. Whole life insurance, on the other hand, is more expensive but provides lifelong coverage and builds cash value over time, making it a good option for those who want coverage for life and the ability to build retirement wealth.

| Characteristics | Values |

|---|---|

| Coverage | Term life insurance covers a predetermined period (the term) |

| Whole life insurance offers lifelong coverage | |

| Affordability | Term life insurance is more affordable |

| Whole life insurance is more expensive | |

| Complexity | Term life insurance is simpler |

| Whole life insurance is more complex | |

| Cash value | Term life insurance does not accumulate cash value |

| Whole life insurance includes an investment component that grows over time |

Explore related products

What You'll Learn

- Term life insurance is cheaper and covers you for a set period of time

- Whole life insurance is more expensive but lasts your entire life

- Term life insurance does not accumulate cash value

- Whole life insurance includes an investment component that grows over time

- Whole life insurance can act like a tax-advantaged retirement savings plan

![]()

Term life insurance is cheaper and covers you for a set period of time

Term life insurance is more affordable than whole life insurance, but it only covers you for a set period of time. This makes it ideal for those who only need coverage for a finite period, such as while raising children or paying off a mortgage. Term life insurance is also simpler than whole life insurance, as it does not include a cash value feature. This means that you cannot withdraw or borrow against the policy while you are alive.

Whole life insurance, on the other hand, offers lifelong coverage as long as you continue paying your premiums. It also includes an investment component that grows over time, allowing you to build retirement wealth and income through the policy's cash value account. However, this type of insurance is significantly more expensive than term life insurance.

When choosing between term and whole life insurance, it is important to consider your specific needs and financial situation. If you only need financial protection for a certain number of years, term life insurance may be a more affordable option. However, if you are looking for lifelong coverage and the ability to build retirement wealth, whole life insurance may be a better choice.

Ultimately, the decision between term and whole life insurance comes down to your personal preferences, budget, and how long you want coverage for. By understanding the differences between these two types of insurance, you can choose a policy that best suits your needs and lifestyle.

Understanding Tax Implications on Life Insurance Payouts

You may want to see also

Explore related products

![]()

Whole life insurance is more expensive but lasts your entire life

Term life insurance is more affordable but only covers you for a set period of time. Whole life insurance, on the other hand, is more expensive but lasts your entire life. It also includes an investment component that grows over time, allowing you to build retirement wealth and income through the policy's cash value account. This makes whole life insurance a good option for those who want coverage for life and are looking for a way to build retirement wealth.

Term life insurance is ideal if you only need coverage for a finite period, such as while raising children or paying off a mortgage. It is simpler and may be a good option if you mainly need income replacement for a specific time. Whole life insurance, on the other hand, is more complex and provides lifelong coverage. It can also act as a tax-advantaged retirement savings plan with a guaranteed rate of return.

The choice between term and whole life insurance depends on your specific needs and financial situation. If you are looking for low-cost coverage, term life insurance may be a better option. However, if you need lifelong coverage and can afford the higher premiums, whole life insurance may be a better fit. It is important to consider your lifestyle and financial goals when choosing between term and whole life insurance.

Whole life insurance is a good option for those who want the peace of mind of knowing that they have coverage for their entire life. It is also a good choice for those who want to build retirement wealth and income through the policy's cash value account. However, it is important to note that whole life insurance is more complex and may not be suitable for everyone. It is always a good idea to consult with a financial advisor to determine which type of insurance is the best fit for your specific needs and goals.

Life Insurance After Retirement: What FERS Employees Need to Know

You may want to see also

Explore related products

![Life and Health Insurance Study Cards: Life Health Insurance License Exam Prep with Practice Test Questions [Full Color]](https://m.media-amazon.com/images/I/51Pox87Z5lL._AC_UL320_.jpg)

![]()

Term life insurance does not accumulate cash value

Term life insurance is more affordable than whole life insurance, but it only provides coverage for a set period of time. This means that it does not accumulate cash value, so you cannot withdraw or borrow against the policy while you are alive. Term life insurance is ideal if you only need coverage for a finite period, such as while raising children or paying off a mortgage. It is also simpler than whole life insurance.

Whole life insurance, on the other hand, offers lifelong coverage as long as you continue paying your premiums. It also includes an investment component that grows over time, allowing you to build retirement wealth and income through the policy's cash value account. However, whole life insurance is significantly more expensive than term life insurance.

The choice between term and whole life insurance depends on your specific needs and financial situation. If you only need financial protection for a certain number of years, term life insurance may be a good option. However, if you want coverage for your entire life and are willing to pay higher premiums, whole life insurance may be a better choice.

Term life insurance is a straightforward and cost-effective option for those who need income replacement for a specific period. It is important to note that term life insurance does not build cash value, so it should not be viewed as a long-term investment or savings plan. Instead, it provides peace of mind and financial security during the specified term of the policy.

Life Insurance vs Assurance: What's the Real Difference?

You may want to see also

Explore related products

![]()

Whole life insurance includes an investment component that grows over time

Term life insurance is more affordable than whole life insurance, but it only provides coverage for a set period of time. Whole life insurance, on the other hand, offers lifelong coverage and includes an investment component that grows over time. This means that the policy can act as a tax-advantaged retirement savings plan, providing a guaranteed rate of return. While whole life insurance is more expensive, it can be a good option for those who want coverage for life and are looking to build retirement wealth through the policy's cash value account.

Term life insurance is a good option for those who only need coverage for a finite period, such as while raising children or paying off a mortgage. It is simpler and may be more suitable for those who mainly need income replacement for a specific time. Whole life insurance, on the other hand, is more complex and may be a better fit for those who want lifelong coverage and the ability to build cash value over time.

The decision between term and whole life insurance ultimately depends on an individual's specific needs and financial situation. Term life insurance typically offers lower premiums, making it a more budget-friendly option. However, whole life insurance provides the security of lifelong coverage and the potential for retirement savings.

Whole life insurance, with its investment component, can be a valuable tool for those seeking long-term financial security. The policy's cash value grows over time, providing a source of retirement income or wealth accumulation. This feature sets whole life insurance apart from term life insurance, which does not accumulate cash value. By investing in whole life insurance, individuals can not only protect their loved ones but also build a nest egg for their future.

How to Get Life Insurance for Your Boyfriend

You may want to see also

Explore related products

![]()

Whole life insurance can act like a tax-advantaged retirement savings plan

Term life insurance is more affordable but only covers you for a set period of time. Whole life insurance is more expensive but lasts your entire life and includes an investment component that grows over time. Whole life insurance can act like a tax-advantaged retirement savings plan with a guaranteed rate of return. This means that you can build retirement wealth and income through the policy's cash value account.

Term life insurance is ideal if you only need coverage for a finite period, such as while raising children or paying off a mortgage. It is also simpler and may be suitable if you mainly need income replacement for a specific time. Whole life insurance is better for those who want coverage for life and the ability to build retirement wealth and income. It is more complex and may not be the best option if you are on a budget.

The main difference between term and whole life insurance is the length of coverage. Term life insurance typically lasts from 10 to 30 years, depending on how long you want coverage. Whole life insurance, on the other hand, offers lifelong coverage as long as you continue paying your premiums. This makes it a good option for those who want coverage for life and are willing to pay higher premiums.

When choosing between term and whole life insurance, it is important to consider your specific needs and financial situation. Term life insurance may be a good choice if you are looking for low-cost coverage and only need financial protection for a certain number of years. Whole life insurance, on the other hand, may be a better option if you want lifelong coverage and the ability to build retirement wealth. It is important to weigh the pros and cons of each type of insurance before making a decision.

Risk-Based Capital: Selling Life Insurance with Confidence

You may want to see also

Frequently asked questions

Term insurance is a type of life insurance that covers you for a set period of time, typically 10 to 30 years. It is more affordable than whole life insurance but does not accumulate cash value, meaning you cannot withdraw or borrow against the policy while you are alive.

Whole life insurance provides lifelong coverage as long as you continue paying your premiums. It includes an investment component that grows over time and can act as a tax-advantaged retirement savings plan. However, whole life insurance is significantly more expensive than term life insurance.

Term insurance is simpler and more affordable than whole life insurance. It is ideal if you only need coverage for a finite period, such as while raising children or paying off a mortgage.

Whole life insurance provides lifelong coverage and allows you to build retirement wealth and income through the policy's cash value account. It is suitable for those who want coverage for life and the ability to accumulate wealth through their insurance policy.