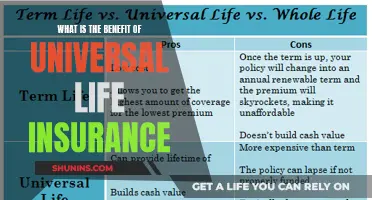

Whole life insurance is a type of permanent life insurance that offers a range of benefits to help individuals and their loved ones. One of the biggest advantages is the financial security it provides, including a guaranteed death benefit, which is a fixed sum of money paid to beneficiaries upon the policyholder's death. This death benefit is generally tax-free and can be used to cover funeral expenses, replace lost income, pay off debts, or support the financial needs of surviving family members. Whole life insurance also offers the potential to accumulate cash value, which is tax-deferred, meaning you don't pay taxes on it until you withdraw the funds. This combination of benefits makes whole life insurance a valuable tool for financial planning and wealth building.

| Characteristics | Values |

|---|---|

| Financial security | Provides a death benefit to beneficiaries |

| Offers lifetime protection | |

| Potential to accumulate cash value | |

| Fixed premiums | |

| Cash value and death benefit protected from creditors and bankruptcy proceedings |

Explore related products

What You'll Learn

![]()

Financial security

Whole life insurance is a type of permanent life insurance that offers financial security to the policyholder and their loved ones. It provides a guaranteed death benefit, which is a fixed sum of money paid to beneficiaries upon the policyholder's passing. This benefit is generally tax-free and can be used to cover funeral expenses, replace lost income, pay off debts, or support the financial needs of surviving family members. The death benefit offers a financial cushion to loved ones during a difficult time and provides peace of mind to the policyholder, knowing that their family will be taken care of financially.

In addition to the death benefit, whole life insurance offers the potential to accumulate cash value over time. This cash value growth is tax-deferred, meaning taxes are not paid until funds are withdrawn. This feature makes whole life insurance an attractive option for individuals seeking a safe and predictable way to build wealth. The fixed premiums associated with whole life insurance policies further contribute to financial security by providing predictability and ease of budgeting over the long term.

Whole life insurance is particularly valuable for young families seeking financial stability and protection against life's unpredictability. It ensures that loved ones are financially safeguarded, regardless of unexpected events or changes in health status. This type of insurance can also play a crucial role in estate planning, helping to preserve wealth and provide for beneficiaries, especially when it comes to covering estate taxes.

The combination of guaranteed death benefits, potential cash value accumulation, and fixed premiums makes whole life insurance a powerful tool for comprehensive financial security and long-term planning. It offers a sense of confidence and protection, knowing that loved ones will be financially supported in the event of the policyholder's death. By assessing their needs, goals, and wealth-building objectives, individuals can determine if whole life insurance aligns with their financial security priorities.

Life Insurance for Felons: Is It Possible?

You may want to see also

Explore related products

![]()

Lifetime protection

Whole life insurance is a type of permanent life insurance that offers lifetime protection. It provides a guaranteed death benefit to your beneficiaries, which is a fixed sum of money paid to them upon your passing. This death benefit is generally tax-free and can be used to cover funeral expenses, replace lost income, pay off debts or support the financial needs of surviving family members. Whole life insurance also offers the potential to accumulate cash value, which can be a safe and predictable way to build wealth over time. This combination of benefits makes whole life insurance a valuable tool for financial planning and estate planning.

One of the biggest advantages of whole life insurance is the financial security it offers. It provides peace of mind, knowing that your loved ones will be taken care of financially, no matter what the future holds. This is especially important for young families, who may be facing unpredictable life events, and for individuals seeking a comprehensive approach to financial security and wealth building.

In addition to the death benefit, the cash value growth of a whole life insurance policy is also tax-deferred. This means you don't pay taxes on the growth until you withdraw the funds, providing an added financial benefit. The cash value and death benefit of a whole life insurance policy are also protected from creditors and bankruptcy proceedings in many states, offering an extra layer of asset protection.

Whole life insurance policies typically have fixed premiums, which means your premiums remain the same throughout the policy, regardless of your age or health status. This predictability allows for easier budgeting and financial planning over the long term.

Overall, whole life insurance offers lifetime protection and financial security for you and your loved ones. It provides a guaranteed death benefit, the potential to accumulate cash value, and fixed premiums, making it a valuable tool for financial planning and protecting your family's future.

Life Insurance vs. Assurance: What's the Real Difference?

You may want to see also

Explore related products

![]()

Fixed premiums

Whole life insurance is a type of permanent life insurance that offers a range of benefits, including financial security and wealth-building opportunities. One of the key advantages of whole life insurance is the guaranteed death benefit, which provides a fixed sum of money to beneficiaries upon the policyholder's passing. This benefit is generally tax-free and can be used to cover funeral expenses, replace lost income, pay off debts, or support the financial needs of surviving family members.

Additionally, fixed premiums allow policyholders to lock in their coverage at a set rate, protecting them from potential future premium increases. This can be particularly advantageous in the long run, as the cost of insurance tends to rise over time due to factors such as inflation and increasing healthcare costs. By securing a fixed premium, policyholders can mitigate the impact of these rising costs and maintain their financial stability.

Whole life insurance policies with fixed premiums also offer the potential for cash value accumulation. The cash value component of the policy grows over time and can be accessed by the policyholder during their lifetime. This provides an additional financial benefit, as the policyholder can borrow against the cash value or withdraw funds if needed. The cash value growth is also tax-deferred, meaning policyholders do not pay taxes on the growth until they withdraw the funds. This feature further enhances the financial security and flexibility offered by whole life insurance.

Overall, fixed premiums are a significant advantage of whole life insurance, providing policyholders with predictability, financial stability, and peace of mind. By locking in a fixed rate, policyholders can more easily plan for the future, protect their loved ones, and build their wealth over time.

Borrowing Against Life Insurance: A Smart Financial Move?

You may want to see also

Explore related products

![Life and Health Insurance Study Cards: Life Health Insurance License Exam Prep with Practice Test Questions [Full Color]](https://m.media-amazon.com/images/I/51Pox87Z5lL._AC_UL320_.jpg)

![]()

Tax-deferred cash value growth

Whole life insurance is a type of permanent life insurance that offers a range of benefits to those seeking a comprehensive approach to financial security and wealth building. One of the key advantages of whole life insurance is the tax-deferred cash value growth it provides. This means that policyholders can accumulate cash value within their insurance policy without paying taxes on it until they withdraw the funds. This feature makes whole life insurance an attractive option for those seeking to build wealth over time while also enjoying the peace of mind that comes with lifetime protection.

The tax-deferred nature of whole life insurance allows policyholders to maximise their investment returns by deferring taxes on their cash value growth. This can result in significant savings over time, as the cash value accumulates and grows tax-free until withdrawal. This feature is particularly beneficial for long-term financial planning, as it allows policyholders to grow their wealth efficiently and effectively.

In addition to tax-deferred cash value growth, whole life insurance offers a guaranteed death benefit, which provides a fixed sum of money to beneficiaries upon the policyholder's passing. This benefit is generally tax-free and can be used to cover funeral expenses, replace lost income, pay off debts, or support the financial needs of surviving family members. With whole life insurance, premiums typically remain fixed, providing predictability and ease of budgeting for policyholders.

The combination of tax-deferred cash value growth and guaranteed death benefits makes whole life insurance a valuable tool for financial planning and wealth accumulation. It offers a safe and predictable way to build cash value while also providing lifetime protection and financial security for loved ones. For individuals seeking a comprehensive approach to financial planning and wealth building, whole life insurance can be a compelling option to consider.

Spousal Life Insurance: Protecting Your Partner's Future

You may want to see also

Explore related products

![]()

Asset protection

Whole life insurance can be a valuable tool for asset protection. It offers a guaranteed death benefit, which is a fixed sum of money paid to your beneficiaries upon your passing. This provides your loved ones with a financial cushion during a difficult time and can be used to cover funeral expenses, replace lost income, pay off debts, or support the financial needs of surviving family members. The death benefit is generally tax-free, adding to its value as an asset protection tool.

In addition to the death benefit, whole life insurance can also help with wealth building. The cash value of the policy grows over time, and this growth is tax-deferred, meaning you don't pay taxes on it until you withdraw the funds. This can be a significant advantage for individuals seeking a safe and predictable way to accumulate cash value alongside life insurance.

Another aspect of asset protection offered by whole life insurance is the protection of your policy's cash value and death benefit from creditors and bankruptcy proceedings in many states. This provides an added layer of financial security for policyholders, ensuring that their assets are protected even in the event of financial hardship.

Whole life insurance also offers fixed premiums, which means your premiums remain the same throughout the policy, regardless of your age or health status. This predictability allows for easier budgeting and financial planning over the long term. By knowing your exact premium costs, you can more effectively manage your assets and ensure financial stability for yourself and your loved ones.

Overall, whole life insurance provides a comprehensive approach to asset protection. It offers financial security and peace of mind, knowing that your loved ones will be taken care of financially, no matter what the future holds. By combining lifetime protection, guaranteed death benefits, and the potential to accumulate cash value, whole life insurance becomes a valuable tool for financial planning and asset protection.

Life Insurance Agents: A Stressful but Rewarding Career Choice

You may want to see also

Frequently asked questions

Whole life insurance offers financial security and a guaranteed death benefit to your beneficiaries. It also provides the potential to accumulate cash value.

A guaranteed death benefit is a fixed sum of money paid to your beneficiaries upon your passing. This benefit is generally tax-free and can be used to cover funeral expenses, replace lost income, pay off debts or support the financial needs of surviving family members.

Whole life insurance is ideal for individuals seeking a comprehensive approach to financial security and wealth building. It is also suitable for persons seeking lifetime protection with guaranteed benefits for their loved ones and those interested in using life insurance as part of long-term financial planning and estate planning strategies.