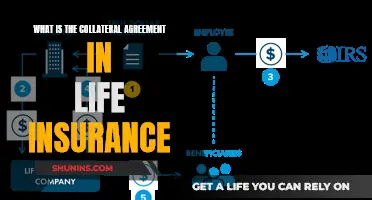

Life insurance policies are contracts that cover a person's life for a set number of years or a lifetime. The insured person pays premiums to maintain their coverage, and the life insurer pays out a sum of money to their beneficiaries when they die. The cost of life insurance depends on factors such as age, state of health, coverage type, and coverage amount. The biggest life insurance company in the United States is Northwestern Mutual, with 10.71% of the market share. New York Life Group is the largest life insurance company by direct premiums written, with a 6.86% market share.

| Characteristics | Values |

|---|---|

| Maximum life insurance cover | $500,000 |

| Type of policy | Set number of years or lifetime |

| Biggest life insurance company in the US | Northwestern Mutual |

| Market share of the biggest US life insurance company | 10.71% |

| Biggest life insurance company by direct premiums written | New York Life Group |

| Market share of the biggest life insurance company by direct premiums written | 6.86% |

Explore related products

$11.25 $15.95

What You'll Learn

- The cost of life insurance depends on factors like age, health, coverage type, and more

- Life insurance companies issue policies that cover a person's life for a set number of years or a lifetime

- The insured person pays premiums to maintain their coverage

- The life insurer pays out a sum of money to beneficiaries when the insured person dies

- Northwestern Mutual is the biggest life insurance company in the US

![]()

The cost of life insurance depends on factors like age, health, coverage type, and more

The cost of life insurance depends on a variety of factors, including age, health, coverage type, and more. Life insurance companies issue policies that cover a person's life for a set number of years or for a lifetime. These policies are contracts: the insured person pays premiums to maintain their coverage, and the life insurer pays out a sum of money to the beneficiaries upon the person's death.

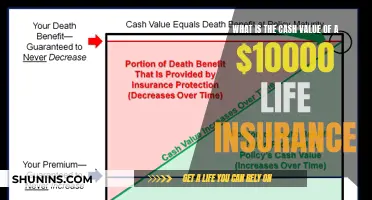

The cost of life insurance varies depending on the age and health of the insured person. For example, a $500,000 30-year term life policy for a person in excellent health would range from $25 to $125 per month, depending on their age and sex. Permanent life policies, which offer a guaranteed death benefit and a cash value component, are typically more expensive than term life policies.

The type of coverage also affects the cost of life insurance. For instance, a policy with a higher coverage amount will generally be more expensive than one with a lower coverage amount. Additionally, the length of the policy can impact the cost, with longer policies typically costing more than shorter ones.

Other factors, such as the financial strength of the insurance company and the level of personalisation offered, can also influence the cost of life insurance. It is important to compare quotes from different insurers to find the best price and ensure that the policy meets your specific needs.

Changing Union Fidelity Life Insurance Beneficiaries: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Life insurance companies issue policies that cover a person's life for a set number of years or a lifetime

The biggest life insurance company in the United States is Northwestern Mutual, with 10.71% of the market share. However, the largest life insurance company by direct premiums written is New York Life Group, which currently holds a 6.86% market share.

HSBC Life Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

The insured person pays premiums to maintain their coverage

Life insurance companies issue policies that cover a person’s life, either for a set number of years or for a lifetime. These policies are contracts: the insured person pays premiums to maintain their coverage, and the life insurer pays out a sum of money to their beneficiaries when they die. The cost of life insurance depends on various factors such as your age, state of health, coverage type, and coverage amount. On average, a $500,000, 30-year term life policy for a person in excellent health would range from $25 to $125 per month, depending on their age and sex, according to quotes from Quotacy. Permanent life policies are significantly more expensive than term life policies as they typically offer a guaranteed death benefit and a cash value component.

It's important to note that the premium amount may also vary depending on the insured person's age and health status at the time of purchasing the policy. Generally, younger and healthier individuals will pay lower premiums than older individuals or those with pre-existing health conditions. This is because the insurer assesses the risk of paying out a claim during the policy term and sets the premium accordingly.

Additionally, the type of policy can also impact the premium amount. For example, term life insurance policies, which provide coverage for a specific period, tend to have lower premiums than permanent life insurance policies, which offer lifetime coverage. This is because term life insurance does not accumulate cash value and only pays out if the insured person dies within the policy term. On the other hand, permanent life insurance policies often include a savings component, allowing them to accumulate cash value over time, which increases the overall cost.

To maintain their coverage, the insured person must continue paying the premiums on time and as agreed upon in the policy contract. Failure to do so may result in the policy being cancelled or the benefits being reduced. It is crucial for individuals to carefully consider their financial situation and long-term goals when selecting a life insurance policy to ensure they can afford the premiums and maintain their coverage over the desired period.

Life Insurance: Opting Out Anytime, Is It Possible?

You may want to see also

Explore related products

![]()

The life insurer pays out a sum of money to beneficiaries when the insured person dies

Life insurance companies issue policies that cover a person’s life for a set number of years or for a lifetime. These policies are contracts: the insured person pays premiums to maintain their coverage, and the life insurer pays out a sum of money to their beneficiaries when they die. The cost of life insurance depends on various factors such as your age, state of health, coverage type, and coverage amount. On average, a $500,000, 30-year term life policy for a person in excellent health would range from $25 to $125 per month, depending on their age and sex. Permanent life policies are significantly more expensive than term life policies as they typically offer a guaranteed death benefit and a cash value component.

Farmers Term Life Insurance: Double Indemnity Protection?

You may want to see also

Explore related products

![]()

Northwestern Mutual is the biggest life insurance company in the US

The size of a person's life insurance policy depends on their personal preference, age, state of health, coverage type, and more. On average, a $500,000, 30-year term life policy for a person in excellent health would range from $25 to $125 per month, depending on their age and sex. Permanent life policies are significantly more expensive than term life policies as they typically offer a guaranteed death benefit and a cash value component.

Life Insurance: An Investment or a Safety Net?

You may want to see also

Frequently asked questions

The biggest life insurance policy a person can have depends on their age, state of health, coverage type, and coverage amount. On average, a $500,000, 30-year term life policy for a person in excellent health would range from $25 to $125 per month, depending on their age and sex.

The cost of life insurance depends on various factors such as your age, state of health, coverage type, coverage amount, and more.

Term life policies are significantly less expensive than permanent life policies as they do not typically offer a guaranteed death benefit or a cash value component.