Life insurance can be an expensive investment, but it doesn't have to be. There are several options for affordable life insurance, but it's important to balance cost and coverage to ensure your loved ones are provided for. Term life insurance is usually the cheapest option because it's only active for a set number of years and doesn't generate cash value. However, it's important to consider the level of coverage provided by a policy, as low-cost policies may not offer sufficient protection.

| Characteristics | Values |

|---|---|

| Type | Term life insurance |

| Coverage | Set period, generally 10 to 30 years |

| Cost | $30 a month for a healthy 30-year-old male, $23 a month for a healthy 30-year-old female |

| Benefits | Covers temporary needs, e.g. parents with young children or people paying off a mortgage |

| Drawbacks | May be insufficient if you have a family, may not meet the needs of your loved ones upon your death |

| Alternatives | Group life insurance provided by employers, whole life insurance, universal life insurance |

Explore related products

What You'll Learn

![]()

Term life insurance

Many employers offer group life insurance, which can be a good starting point but may be insufficient if you have a family. It's important to note that buying low-cost or cheap life insurance isn't always the best choice. Life insurance provides those you love and care about with financial protection upon your death. Given the important role life insurance plays, prioritising cost over quality with a cheap or low-cost life insurance policy can be risky. A low-cost life insurance policy may have low coverage limits that are not enough to meet the needs of your loved ones. To save the most money, consider a life insurance policy that requires a medical exam, which helps the company assess risk.

Life Insurance at 65: What You Need to Know

You may want to see also

Explore related products

![]()

Whole life insurance

Term life insurance is usually the cheapest form of life insurance. It is only active for a set number of years and doesn't generate cash value. However, it is important to note that buying low-cost or cheap life insurance is not always the best choice. Life insurance provides financial protection for your loved ones upon your death, so prioritising cost over quality can be risky.

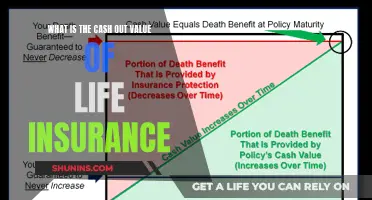

The cash value component of whole life insurance is a unique feature that sets it apart from other types of life insurance. This component allows you to build up cash value over time, which can be used in several ways. You can use it to pay your premiums, which can help ease the financial burden of maintaining the policy. Alternatively, you can make withdrawals from the cash value to use for other purposes, such as funding a child's education or covering unexpected expenses. The cash value can also be used as collateral for a loan, providing you with additional financial flexibility.

When considering whole life insurance, it is important to weigh the benefits against the costs. While it offers more comprehensive coverage than term life insurance, it also comes with higher premiums. Additionally, the cash value component may not be a significant factor if you are primarily concerned with obtaining the lowest possible price. However, for those seeking long-term financial security and peace of mind, whole life insurance can be a valuable investment.

Life Insurance & POA: Can a POA Request Information?

You may want to see also

Explore related products

![Short Term 12 [Blu-ray]](https://m.media-amazon.com/images/I/71Lb114AFoL._AC_UY218_.jpg)

![]()

Universal life insurance

Term life insurance is usually the cheapest form of life insurance. It is only active for a set number of years, generally 10 to 30, and doesn't generate cash value.

Leaving Life Insurance to a Trust: Is It Possible?

You may want to see also

Explore related products

![Short Term 12 [DVD] [2013] [Region 1] [US Import] [NTSC]](https://m.media-amazon.com/images/I/51jC+xMaCBL._AC_UY218_.jpg)

![]()

Variable life insurance

Term life insurance is usually the cheapest form of life insurance. It is only active for a set number of years and doesn't generate cash value.

Understanding Life Insurance Foul Play and Its Implications

You may want to see also

![End of Term [DVD]](https://m.media-amazon.com/images/I/61zb8XLHPXL._AC_UY218_.jpg)

![End of Term [Blu-ray]](https://m.media-amazon.com/images/I/61C-da10mXL._AC_UY218_.jpg)

![]()

Group life insurance

Term life insurance is usually the cheapest form of life insurance. It is only active for a set number of years, generally 10 to 30 years, and doesn't generate cash value. For example, in October 2024, a term life insurance policy with a $500,000 death benefit and a 20-year term averaged about $30 a month for a healthy 30-year-old male and $23 a month for a healthy 30-year-old female.

When considering group life insurance, it's important to balance cost and coverage. While getting the lowest price may be a priority, buying low-cost or cheap life insurance is not always the best choice. Life insurance provides financial protection for your loved ones upon your death, so prioritising cost over quality with a cheap policy can be risky.

Life Insurance Payments: When Do They End?

You may want to see also

Frequently asked questions

Term life insurance is usually the cheapest option because it's only active for a set number of years and doesn't generate cash value.

Term life insurance covers you for a set period, generally 10 to 30 years. If you outlive the term, the policy expires. It's useful for those who have temporary needs, like parents with young children or people paying off a mortgage with a partner.

Yes, consider a life insurance policy that requires a medical exam, which helps the company assess risk. Your employer may also provide life insurance for free, but it will probably end if you leave your job and often has low coverage limits.

Yes, buying low-cost or cheap life insurance isn't always the best choice. A low-cost life insurance policy may have low coverage limits that are not enough to meet the needs of your loved ones upon your death. It's important to balance cost and coverage when choosing a life insurance policy.