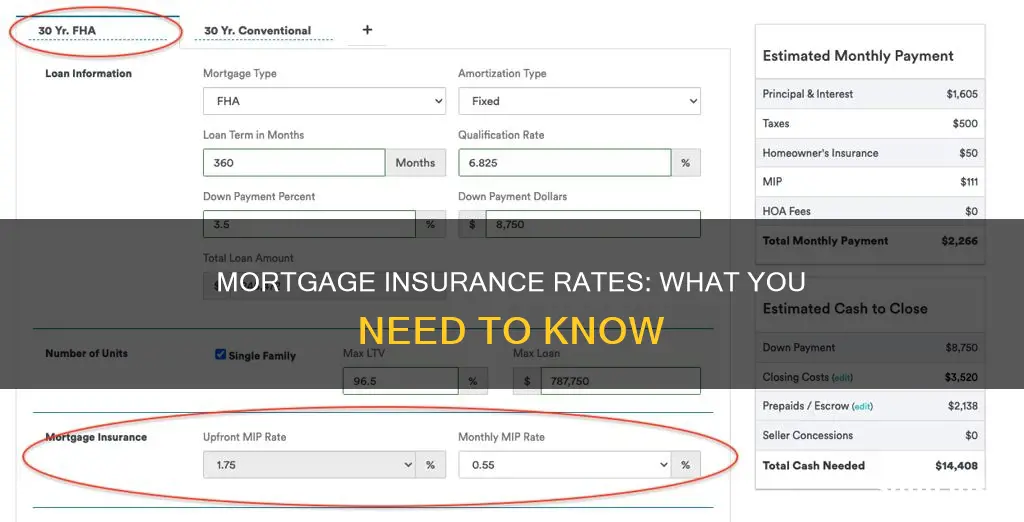

Private mortgage insurance (PMI) is a type of insurance that protects the lender in the event of the borrower defaulting on their mortgage. It is required for borrowers who take out a conventional mortgage with a down payment of less than 20%. The PMI rate varies depending on factors such as the borrower's credit score, debt-to-income ratio, and loan-to-value ratio. Typically, the PMI rate ranges from 0.2% to 2% of the loan amount per year, but it can be higher for borrowers with low credit scores and high debt-to-income ratios. Borrowers can use PMI calculators to estimate their monthly PMI costs and make informed decisions about their mortgage loans.

| Characteristics | Values |

|---|---|

| Type of Insurance | Private Mortgage Insurance (PMI) |

| Who pays the premium | The borrower |

| When is PMI required | When the down payment is less than 20% |

| PMI rate | Around 0.2% to 2% of the loan amount per year |

| Factors affecting PMI rate | Credit score, debt-to-income ratio, loan-to-value ratio, local housing market |

| PMI payment method | Monthly premium, upfront at closing, or a combination of both |

| Getting rid of PMI | Put 20% down, choose a single premium PMI, go for lender-paid PMI, request it when the mortgage balance is 80% of the home's value |

Explore related products

What You'll Learn

![]()

Lender-paid mortgage insurance

With LPMI, the lender pays the mortgage insurance costs, and in return, the lender charges a higher interest rate on the home loan. This higher interest rate is how lenders recoup the cost of LPMI. LPMI is often more affordable on a monthly basis than private mortgage insurance (PMI), but it may cost more over the life of the loan. It is important to note that LPMI cannot be cancelled and will remain in effect for the life of the loan, unless the loan is refinanced.

LPMI may be advantageous in certain situations. For example, if you plan to live in your home for a short period of time and won't reach the 20% equity mark needed to drop PMI, LPMI could be a better option. Additionally, if you have a high income, the higher mortgage interest rate may be appealing as mortgage interest is deductible on federal taxes.

When considering LPMI, it is essential to compare offers from multiple lenders to find the most favourable terms. Lenders may offer different interest rates and some may even advertise special loan programs that don't include a mortgage insurance requirement. It is also worth noting that LPMI is not the only option to avoid high upfront costs; borrowers can also consider a single premium PMI, which allows them to make a single payment to remove PMI from a conventional mortgage.

Hippo: Auto Insurance Options

You may want to see also

Explore related products

![]()

Private mortgage insurance (PMI)

The cost of PMI depends on several factors, including the size of the mortgage loan, the down payment amount, and your credit score. The higher the loan amount, the higher the PMI cost. A larger down payment will reduce the PMI cost. A higher credit score will also result in a lower PMI rate. PMI will usually be paid as a monthly premium alongside your mortgage payment, but it can also be paid upfront at closing or through a combination of both.

There are a few ways to avoid paying PMI. One way is to make a 20% down payment on the property. Alternatively, you can request to cancel PMI when your mortgage balance reaches 80% of your home's value. Lenders are required to cancel PMI when your balance reaches 78% of your home's value or when you reach the halfway point of your loan term. Another option is to choose a single premium PMI, which allows you to make a single payment to remove PMI from a conventional mortgage.

PMI should not be confused with homeowner's insurance, which protects you from losses if something unexpected happens to your home or belongings, such as a fire. PMI is also different from mortgage protection insurance (MPI), which is a type of life insurance that pays off your mortgage when you die or if you become unemployed or disabled.

Auto Insurance Medical Coverage: Is $5000 Sufficient?

You may want to see also

Explore related products

![]()

How much is mortgage insurance?

The cost of mortgage insurance varies depending on the type of loan, whether it's government-backed, and who pays the premium. Private mortgage insurance (PMI) is for conventional loans, which are basic mortgages. If your down payment is less than 20%, your lender will require you to pay PMI. Typically, PMI fees range from 0.2% to 2% of the original loan amount per year. According to the Urban Institute's Housing Finance Policy Center, the average cost of PMI for a conventional home loan ranges from 0.46% to 1.50% of the original loan amount per year.

Your credit score, debt-to-income ratio, and loan-to-value ratio (LTV) can affect your PMI rate. Borrowers with low credit scores, high DTIs, and smaller down payments will typically pay higher mortgage insurance rates. Building your credit score, paying down debt, and putting down as much as you can afford may reduce your PMI costs.

You can calculate your monthly mortgage payment with PMI using a PMI calculator. The calculator will ask for the dollar amount of the home you plan to buy, the amount of cash you plan to pay upfront, and your interest rate. It will then provide an estimate of your monthly PMI cost.

There are several ways to get rid of mortgage insurance. With a conventional mortgage, you won't have to pay mortgage insurance if you put down at least 20%. You can also make a single payment to remove the PMI from a conventional mortgage, or request that the mortgage servicer remove the PMI once your mortgage balance is 80% of the value of your home.

Cell Phone Tickets: Insurance Premiums and Costly Consequences

You may want to see also

Explore related products

![]()

Factors affecting PMI rate

Private Mortgage Insurance (PMI) is a type of insurance that is required when taking out a conventional mortgage with a down payment of less than 20%. PMI rates typically range from 0.5% to 1.5% of the loan amount per year, but can be as high as 6%. The rate varies depending on several factors, including:

Down Payment

The size of the down payment is a significant factor in determining the PMI rate. A smaller down payment will result in a higher PMI rate, as it is considered a higher risk for the lender. Conversely, a larger down payment can help lower the PMI rate.

Credit Score

An individual's credit score also plays a crucial role in determining the PMI rate. Borrowers with lower credit scores will typically pay higher PMI rates compared to those with higher credit scores. Lenders consider borrowers with lower credit scores to be at a higher risk of defaulting on their loans.

Debt-to-Income Ratio

The borrower's debt-to-income ratio (DTI) is another factor that can affect the PMI rate. A high DTI indicates that a larger portion of the borrower's income is dedicated to debt repayment, which may lead to a higher PMI rate. Lenders view a high DTI as an increased risk factor.

Loan-to-Value Ratio

The loan-to-value ratio (LTV) is the amount of the loan compared to the value of the property. A higher LTV ratio indicates a higher-risk loan, as the borrower has less equity in the property. Lenders typically require PMI for loans with an LTV ratio above 80%. The PMI rate may increase with a higher LTV ratio to mitigate the risk.

Type of Loan

Different types of loans, such as conventional mortgages or adjustable-rate mortgages (ARMs), can have varying PMI rates. Additionally, loans backed by the Federal Housing Administration (FHA) have their own PMI structure, which includes an upfront cost and an annual or monthly premium.

It is important to note that PMI rates are not static and can change over time. Borrowers can take steps to reduce their PMI rates by improving their credit score, paying down debt, and making a larger down payment when possible.

Mercury Auto Insurance: Understanding Your Coverage Options

You may want to see also

Explore related products

![]()

Avoiding or cancelling PMI

Private mortgage insurance (PMI) is a type of home loan insurance that you're usually required to pay if you take out a conventional mortgage with a down payment of less than 20%. The insurance protects the lender, paying them a portion of the balance due if the borrower defaults on the loan. The PMI rate is typically between 0.2% to 2% of the loan amount per year, and it can be paid monthly alongside your mortgage payment or upfront at closing.

Avoid PMI:

- Make a 20% down payment: With a down payment of at least 20% on a conventional mortgage, you can avoid paying PMI altogether.

- Choose a single premium PMI: This option allows you to make a single payment to remove PMI from a conventional mortgage.

- Go for lender-paid PMI: The lender covers the PMI, but you'll usually pay a higher interest rate.

Cancel PMI:

- Wait for automatic cancellation: Federal law requires lenders to automatically cancel PMI when the loan-to-value (LTV) ratio reaches 78% of the home's purchase price or when the loan term reaches its halfway point, whichever comes first.

- Request early cancellation: You can request PMI cancellation when your mortgage balance reaches 80% of your home's original value, as long as you're current on your payments. This can be achieved by making additional payments or paying down your mortgage faster.

- Refinance: If you have at least 20% equity in your home, you can refinance into a new conventional loan without PMI. However, weigh the benefits against the costs of refinancing.

- Get a reappraisal: If you believe your home's value has increased, you can request a reappraisal and then ask for PMI cancellation.

It's important to note that the specific rules and guidelines for PMI cancellation may vary among lenders and loan types. Homeowners should refer to their loan documents or consult their lender or servicer for detailed information on their PMI cancellation options and requirements.

Insurance: High-Cost Protection or Peace of Mind?

You may want to see also

Frequently asked questions

A conventional mortgage is a basic everyday mortgage that is not government-backed.

The mortgage insurance rate for conventional mortgages varies depending on factors such as your credit score, debt-to-income ratio, and the local housing market. It is typically between 0.2% and 2% of the loan amount per year.

Mortgage insurance is typically required for a conventional mortgage when the down payment is less than 20%.

You can pay mortgage insurance through monthly premiums alongside your mortgage payments. You may also pay upfront at closing or a combination of both.

You can get rid of mortgage insurance by reaching 20% equity in your home, or an 80% loan-to-value (LTV) ratio on your mortgage. You can also request your lender to cancel the mortgage insurance when you pay off 20% of the original value of your home.