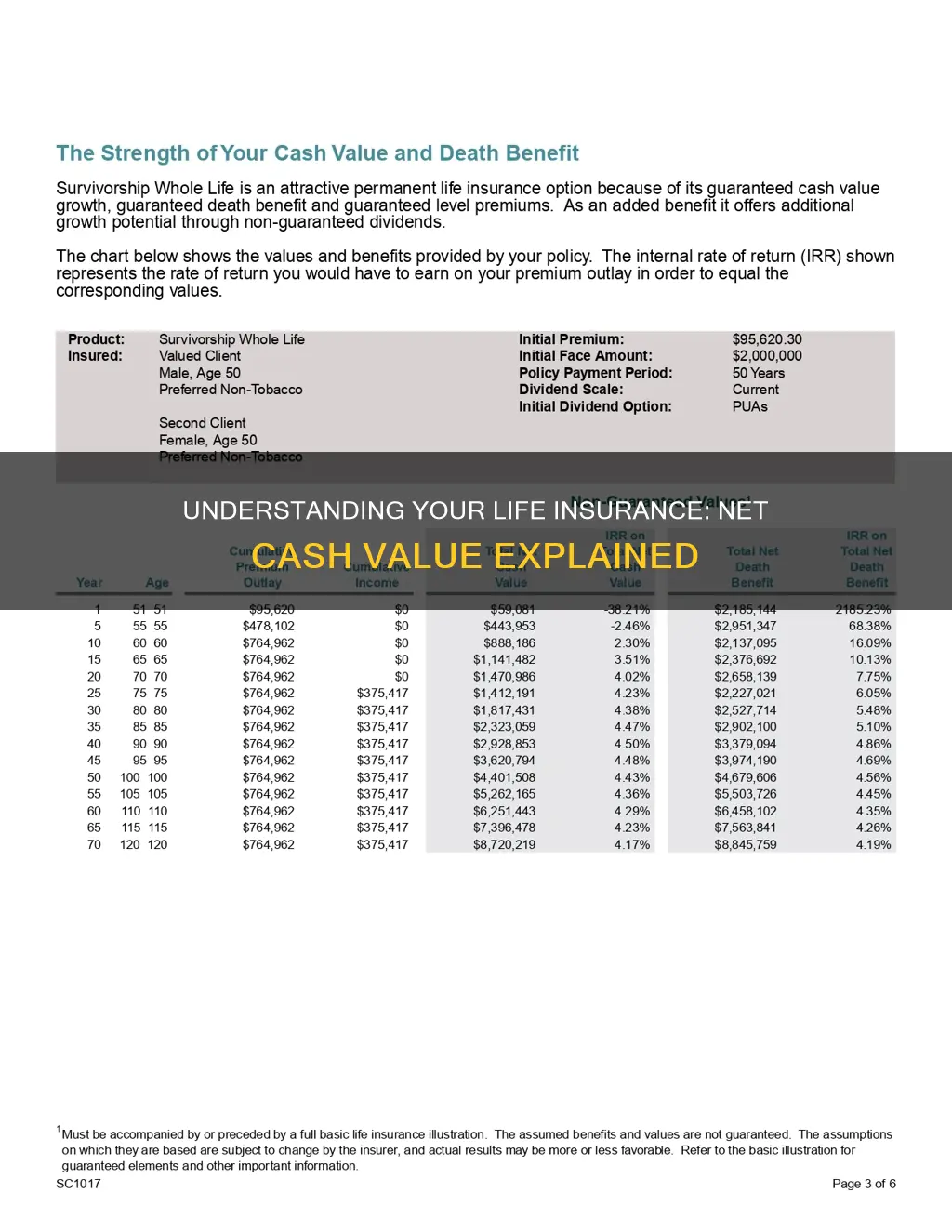

The net cash value of a life insurance policy is the amount of money you will receive if you cancel your permanent life policy. It is the actual surrender value of the policy, minus all fees, surrender charges and any outstanding loans against the policy. You will usually find it listed separately in your life insurance statements. The net cash value will generally be lower than your total accumulated cash value for the first several years of coverage, as it's reduced by fees and surrender charges. However, if you've had your policy in place for 10 to 15 years, the net cash value is likely to be close or equal to the total accumulated cash value.

| Characteristics | Values |

|---|---|

| Definition | The net cash value is the "actual" surrender value of the policy. |

| Calculation | Net cash value = Cash value – Fees – Surrender charges – Outstanding loans against the policy |

| Relation to total accumulated cash value | The net cash value is generally lower than the total accumulated cash value for the first several years of coverage. However, after 10 to 15 years, the net cash value is likely to be close or equal to the total accumulated cash value. |

| Relation to surrender value | The surrender value is usually lower than the cash value for a number of years, as part of the premiums goes toward agent commissions, office personnel salaries, lab fees, etc. |

| Relation to interest rate | A permanent life insurance policy will include a stated guaranteed minimum interest rate to be paid on your cash value account. No matter how low interest rates may fall, you’ll never earn less than the stated guaranteed interest rate. |

Explore related products

What You'll Learn

![]()

How to find the net cash value of your life insurance

The net cash value of your life insurance is the amount of money you will receive if you cancel your permanent life policy. It is the "actual" surrender value of the policy, minus all fees, surrender charges and any outstanding loans against the policy. You will usually find it listed separately in your life insurance statements.

The net cash value will generally be lower than your total accumulated cash value for the first several years of coverage, as it's reduced by fees and surrender charges. However, if you've had your policy in place for 10 to 15 years, the net cash value is likely to be close or equal to the total accumulated cash value.

The surrender value is usually lower than the cash value for a number of years, as part of your premiums goes toward agent commissions, office personnel salaries, lab fees, etc.

If you have a permanent life insurance policy, it will include a stated guaranteed minimum interest rate to be paid on your cash value account. Regardless of how the economy does, you’re guaranteed to receive at least the minimum interest rate specified in your policy. If interest rates go up, the insurer may also raise your interest rate payment. No matter how low interest rates may fall, however, you’ll never earn less than the stated guaranteed interest rate.

Accidental Death Insurance: Supplemental Life's Financial Safety Net

You may want to see also

Explore related products

$8.99

$15.95

![]()

How net cash value differs from cash value

The net cash value of a life insurance policy is the amount of money you will receive if you cancel your permanent life policy. It is the "actual" surrender value of the policy, and it will be listed separately in your life insurance statements.

The net cash value is typically lower than the total accumulated cash value for the first several years of coverage, as it is reduced by fees and surrender charges. However, as the policy matures, the net cash value will increase and may eventually become close to or equal to the total accumulated cash value.

The cash value of a life insurance policy is the sum of money that grows in a cash-value-generating annuity or permanent life insurance policy. It is the money held in your permanent life insurance policy, and it builds when your insurance provider invests some of your premium in bonds or another vehicle.

The main difference between net cash value and cash value is that net cash value takes into account fees, surrender charges, and any outstanding loans against the policy, while cash value does not. Net cash value is the amount you are left with after subtracting these expenses from the accumulated cash value. In the early years of a policy, the surrender value may be significantly lower than the cash value due to the allocation of premiums toward covering initial policy expenses. However, as the policy matures and accumulates more cash value, the surrender value approaches closer to the actual cash value.

Globe Life Insurance Rating: Is It Worth the Cost?

You may want to see also

Explore related products

![]()

How net cash value changes over time

The net cash value of a life insurance policy is the amount of money you will receive if you cancel your permanent life policy. It is the "actual" surrender value of the policy and is usually listed separately in your life insurance statements.

The net cash value is typically lower than the total accumulated cash value for the first several years of coverage, as it is reduced by fees and surrender charges. However, after 10 to 15 years, the net cash value is likely to be close to or equal to the total accumulated cash value. This is because, over time, a larger proportion of your premiums will go towards your cash value rather than being spent on agent commissions, office personnel salaries, lab fees, etc.

If you have a permanent life insurance policy, it will include a stated guaranteed minimum interest rate to be paid on your cash value account. This means that, regardless of how the economy performs, you are guaranteed to receive at least the minimum interest rate specified in your policy. If interest rates rise, your insurer may also raise your interest rate payment. However, even if interest rates fall, you will never earn less than the stated guaranteed interest rate.

It is important to note that the net cash value of your life insurance policy may change over time due to factors such as the performance of the economy and the associated interest rates. Additionally, if you make partial surrenders or withdrawals from your cash value account, this will also impact the net cash value of your policy.

Canceling MassMutual Life Insurance: A Step-by-Step Guide

You may want to see also

Explore related products

$19.89 $7.95

![]()

How to withdraw from your net cash value

The net cash value of a life insurance policy is the amount of money you will receive if you cancel your permanent life policy. This amount will be listed separately in your life insurance statements.

There are several ways to withdraw from your net cash value. One way is to take out a loan against your policy. Loans are generally provided at lower interest rates than a bank loan, do not require credit checks, and do not affect your credit rating. Repaying the loan is optional, but if you don't, your death benefit will be reduced.

Another way to withdraw from your net cash value is to withdraw some of the funds from your cash value, either in a lump sum or in payments. This will also reduce your death benefit.

You can also use the cash value to pay for your premium payments, if you have accumulated enough funds in your cash value account.

Finally, you can surrender your policy by withdrawing all of the cash value and ending your policy. This will eliminate your coverage and may require you to pay a surrender fee.

Cancer and Life Insurance: Payouts and Policies Explained

You may want to see also

Explore related products

![]()

How net cash value is calculated

The net cash value of a life insurance policy is the amount of money you will receive if you cancel your permanent life policy. It is the "actual" surrender value of the policy, and you will typically find it listed separately in your life insurance statements. The net cash value is usually lower than the total accumulated cash value for the first several years of coverage, as it is reduced by fees and surrender charges. However, if you've had your policy in place for 10 to 15 years, the net cash value is likely to be close or equal to the total accumulated cash value.

The net cash value represents your cash value minus all fees, surrender charges and any outstanding loans against the policy. It is important to note that part of your premiums goes toward agent commissions, office personnel salaries, lab fees, etc.

A permanent life insurance policy will include a stated guaranteed minimum interest rate to be paid on your cash value account. Regardless of how the economy does, you’re guaranteed to receive at least the minimum interest rate specified in your policy. If interest rates go up, the insurer may also raise your interest rate payment. However, no matter how low interest rates may fall, you’ll never earn less than the stated guaranteed interest rate.

Life Insurance Cash Value: Can It Decrease Over Time?

You may want to see also

Frequently asked questions

The net cash value of a life insurance policy is the amount of money you will receive if you cancel your permanent life policy.

You will typically find the net cash value listed separately in your life insurance statements.

The net cash value is the 'actual' surrender value of the policy, minus all fees, surrender charges and any outstanding loans against the policy.

Yes, the net cash value will generally be lower than the total accumulated cash value for the first several years of coverage, as it is reduced by fees and surrender charges. However, if you've had your policy in place for 10 to 15 years, the net cash value is likely to be close or equal to the total accumulated cash value.

No, your policy's net cash value is guaranteed regardless of how the economy does. If interest rates go up, the insurer may also raise your interest rate payment, but you'll never earn less than the stated guaranteed interest rate.