Whole of life insurance is a policy that lasts for the policyholder's entire lifetime. It guarantees a payout to the policyholder's family or beneficiaries after the policyholder's death. This is different from term life insurance, which only covers the policyholder for a fixed period of time. Whole life insurance policies require higher premiums than term policies, but the payout is always guaranteed. This type of insurance is also known as life assurance.

| Characteristics | Values |

|---|---|

| Type of insurance | Whole of life insurance |

| Payout | Guaranteed |

| Payout amount | Lump sum |

| Payout timing | When the policyholder dies |

| Payout conditions | Policy must be active |

Explore related products

What You'll Learn

![]()

Whole life insurance guarantees a payout after the policyholder dies

Whole life insurance policies are often more expensive than term life insurance policies, as they provide greater benefits. The premiums for whole life insurance are typically fixed throughout the policy duration, while term rates increase at each renewal as the insured person grows older.

When taking out whole life insurance, the policyholder pays premiums on a monthly or annual basis. In return, the insurance provider agrees to pay out a cash sum if the policyholder dies while the policy is active, as long as the terms and conditions are met. The beneficiary will need to contact the insurance provider as soon as possible after the death of the insured person and provide all the necessary documentation to support their claim. This includes the policy number, information about who they are, details of their relationship with the insured person, and the contact details of the insured person's doctor.

Understanding Life Insurance: Covering Your Basics

You may want to see also

Explore related products

![]()

Whole life insurance vs term life insurance

Whole life insurance is a policy that lasts for the policyholder's entire lifetime. If the policyholder dies, their family or beneficiaries will receive a lump sum payout. Whole life insurance is similar to term life insurance in that both types of policies offer a payout upon the death of the insured. However, there are some key differences between the two.

Term life insurance only covers the policyholder for a fixed period, typically 10, 20 or 30 years. If the policyholder dies within this time frame, their beneficiaries will receive a payout. However, if the policyholder outlives the term of the policy, there will be no payout upon their death. In contrast, whole life insurance guarantees a payout regardless of when the policyholder dies. This is why whole life insurance is also referred to as life assurance.

Another difference between the two types of policies lies in the premiums. Whole life insurance policies require significantly higher premiums than term life insurance policies with the same coverage limit. This is because whole life insurance offers greater benefits, such as guaranteed coverage for life and a fixed premium rate. On the other hand, term life insurance premiums increase at each renewal as the insured grows older.

When choosing between whole life insurance and term life insurance, it's important to consider your needs and financial situation. Whole life insurance provides the peace of mind that your loved ones will receive a payout no matter when you die. However, the higher premiums may be a burden for some. Term life insurance, on the other hand, offers coverage for a fixed period at a lower cost, but there is no guarantee of a payout if the policy term is outlived. Ultimately, the decision depends on your individual circumstances and priorities.

Group Term Life Insurance: Illinois Tax Laws Explained

You may want to see also

Explore related products

![]()

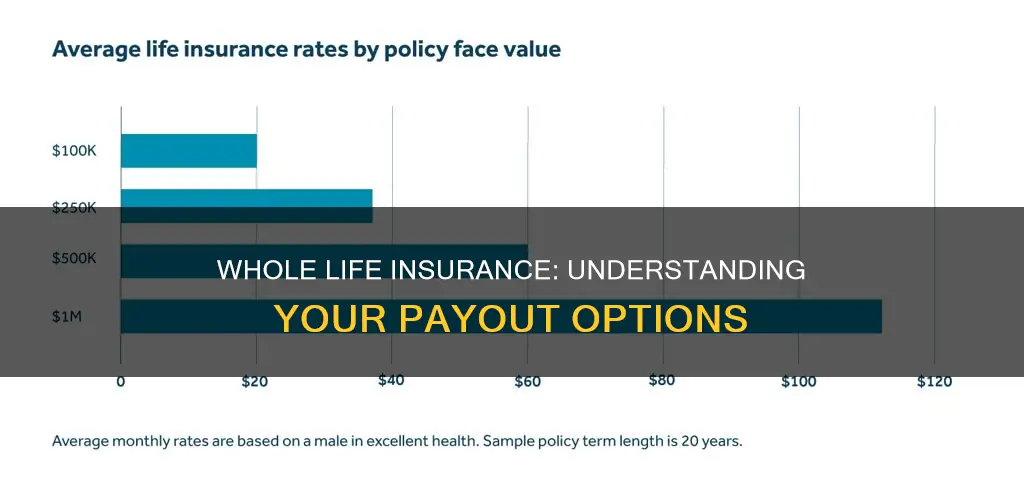

How much does whole life insurance cost?

Whole of life insurance is a policy that lasts for the policyholder’s lifetime. It guarantees a payout after the policyholder dies, whenever that may be. This is why whole life insurance is also called life assurance.

Whole life insurance is similar to term life insurance, in that both types of policies offer a payout upon the death of the insured. However, term life insurance only pays out if the insured dies within a certain time frame, usually 10, 20, or 30 years. Whole life insurance, on the other hand, offers a guaranteed death benefit for the entire lifetime of the insured.

Because of this guarantee, whole life insurance policies require significantly higher premiums than term policies with the same coverage limit. Whole life premiums are typically fixed throughout the policy duration, while term rates increase at each renewal as the insured grows older.

When you take out life insurance, you pay premiums on a monthly or annual basis. In return, the insurance provider agrees to pay out a cash sum if you die while the policy is active, as long as you meet its terms and conditions. The beneficiary will need to contact the insurance provider as soon as possible after the death of the insured person and provide all the necessary documentation to support their claim.

Dying with Dignity: Impact on Life Insurance Policies

You may want to see also

Explore related products

![]()

What happens if the policyholder becomes terminally ill?

Whole of life insurance is a policy that lasts for the policyholder’s lifetime. If the policyholder dies, whole of life cover pays a lump sum to their family or beneficiaries. This is guaranteed, no matter when the policyholder dies. Whole life insurance is similar to term life insurance, but the latter only pays out if the policyholder dies within a certain time frame, usually 10, 20 or 30 years.

If the policyholder becomes terminally ill, whole of life insurance will pay out a sum of money. This can be used to pay off a mortgage, for example, or to help pay for a funeral. The beneficiary should contact their insurance provider as soon as possible after the death of the insured person and will need to have all the documentation to support their claim. This includes the policy number, information about who they are, details of their relationship with the insured person, and the contact details of the insured person’s doctor.

Life Insurance Beneficiaries: Inheriting Tax-Free

You may want to see also

Explore related products

![]()

What happens if the policyholder dies after their term life policy runs out?

Whole of life insurance is a policy that lasts for the policyholder's entire lifetime. If the policyholder dies, whole of life cover pays a lump sum to their family or beneficiaries. This is different from term life insurance, which only covers the policyholder for a fixed period of time. Whole of life insurance guarantees a payout after the policyholder's death, no matter when it occurs. This is why whole of life insurance is also called life assurance.

Term life insurance policies only pay out if the insured dies within a certain time frame, usually 10, 20, or 30 years. If the policyholder dies after their term life policy runs out, their beneficiaries will not receive a payout. This is because term life insurance only covers the policyholder for a fixed period of time, and does not guarantee a payout after the policyholder's death.

To ensure that their loved ones receive a payout, policyholders may consider converting their term life insurance policy to a whole of life insurance policy. This will guarantee a payout upon the policyholder's death, no matter when it occurs. However, it is important to note that whole of life insurance policies require significantly higher premiums than term life insurance policies with the same coverage limit. Whole life premiums are typically fixed throughout the policy duration, while term rates increase at each renewal as the insured grows older.

Additionally, policyholders should review their life insurance coverage regularly to ensure that it meets their needs and the needs of their loved ones. Life insurance is an important tool for financial planning and can provide peace of mind for policyholders and their families. By understanding the differences between whole of life and term life insurance, policyholders can make informed decisions about their coverage and ensure that their loved ones are protected in the event of their death.

Funding Life Insurance: ICICI Bank Account Options

You may want to see also

Frequently asked questions

Whole life insurance pays out a lump sum to the policyholder's family or beneficiaries when the policyholder dies.

Whole life insurance guarantees a payout after the policyholder dies, whereas term life insurance only pays out if the policyholder dies within a certain time frame, usually 10, 20 or 30 years.

Whole life insurance guarantees a payout whenever the policyholder dies, meaning your loved ones will receive a cash sum no matter when you die.