Life insurance is a complex and personal decision that depends on your financial situation, budget, and future plans. The two main types of life insurance are term and cash value policies. Term life insurance is a low-cost option that covers a specific period and pays out if the insured dies during that time. It is a good choice for those with a limited budget or a specific timeline, such as young families with higher debts. Cash value policies, on the other hand, can be kept for as long as needed and have investment features that allow policyholders to access money while alive. Whole life insurance, a type of cash value policy, covers you for your entire life and is a good option for those who want a simple, predictable, and low-maintenance policy. However, it is more expensive than term life insurance. Other factors to consider when choosing a life insurance policy include your health, family health history, and lifestyle, as these can impact the cost and availability of coverage.

| Characteristics | Values |

|---|---|

| Type | Term, Whole, Universal, Variable, Final Expense |

| Coverage Period | Term insurance covers a specific period, while whole and universal insurance cover the entire life |

| Cost | Term insurance is the cheapest, while whole insurance is more expensive |

| Premium | Premium for term insurance increases with age, while whole insurance premium remains the same |

| Cash Value | Whole, Universal, and Variable insurance have cash value, while most term insurance policies do not |

| Flexibility | Universal insurance offers flexibility in premium payments |

| Simplicity | Whole insurance is the simplest compared to other permanent life insurance options |

| Tax Treatment | Whole insurance is attractive due to its favorable tax treatment |

| Applicability | Term insurance is suitable for those with a limited budget or specific timeline, while whole insurance is suitable for those who want to leave an inheritance |

Explore related products

$15.95

What You'll Learn

![]()

Term life insurance

There are several types of term life insurance policies to choose from:

- Fixed-term: This is the most popular and basic version, lasting 10, 20, or 30 years with static premiums.

- Increasing term: This option allows you to increase the value of your death benefit over time, but it tends to be more expensive.

- Decreasing term: This type of insurance reduces premium payments over time and is suitable for those who anticipate fewer financial obligations as they age.

- Annual renewable: This provides coverage on a yearly basis and must be renewed annually. While it can be more expensive due to increasing premiums, it may be a good option for those needing short-term coverage.

How to Secure Life Insurance for Your Mother

You may want to see also

Explore related products

$8.99

![]()

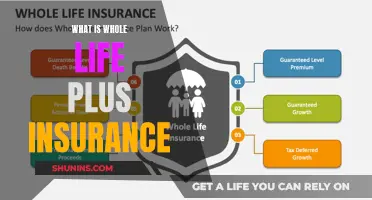

Whole life insurance

One of the advantages of whole life insurance is that it offers fixed premiums that remain consistent throughout the policy. This means that your expenses are predictable and do not increase over time. The death benefit amount is also guaranteed and does not change, providing certainty for your beneficiaries. However, it is important to note that whole life insurance tends to be more expensive than term life insurance, and the premiums are typically higher.

When considering whole life insurance, it is important to keep in mind that the cost may depend on factors such as your age, health conditions, coverage amounts, and cash value growth rates. The younger you are when you purchase the policy, the lower your monthly payments are likely to be. It is also worth noting that whole life insurance policies may have different features and specifics depending on the company and the specific policy.

Overall, whole life insurance offers permanent coverage, fixed premiums, and the ability to build cash value over time. It provides financial protection for your loved ones and can also help you fund significant expenses throughout your lifetime. However, it is important to carefully consider your needs, budget, and long-term financial goals when deciding if whole life insurance is the right choice for you.

Understanding Life Insurance: Face Value Fundamentals

You may want to see also

Explore related products

![]()

Universal life insurance

Variable universal life insurance offers additional investment options, allowing you to invest your cash value in "subaccounts" of your choosing. This provides more growth potential but also carries more risk, as you could lose part or all of your principal.

Roth IRA Life Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

Variable life insurance

When it comes to life insurance, there are many options to choose from, and it can be a tedious and overwhelming process. It is important to remember that the best type of insurance program should suit your needs today and be flexible for the future. Term insurance is the most straightforward type of life insurance policy to understand. It is also the cheapest and most suitable for those on a limited budget. However, permanent life insurance can be an attractive asset due to its favourable tax treatment.

However, there are also downsides to variable life insurance. It is a more complex policy type than other forms of life insurance, as you must monitor and manage your investments and determine how you want to pay premiums. This can require additional time and may lead to stress if you become overwhelmed by investment selection and management. Variable life insurance also tends to cost more than other permanent life insurance policies due to the potential for market downturns and the fees associated with offering the investment component.

Before purchasing variable life insurance, it is important to review all the costs, including fees, and determine whether you can afford this type of policy. You should also consider how much coverage you need and how long you will need the insurance. Variable life insurance may be a good option for those who enjoy managing their investments and are confident in doing so.

Get Life Insurance for Your Parents: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Final expense insurance

When considering final expense insurance, it is important to look at your monthly expenses and determine how much money you want to guarantee your beneficiaries. You can choose a coverage amount, and an agent will help you with the necessary paperwork. Final expense insurance is a good option if you want to provide financial support for your loved ones without the high cost of a traditional whole life insurance policy.

The Intricacies of Life Insurance Product Creation

You may want to see also

Frequently asked questions

There are two main types of life insurance: term and cash value policies. Term life insurance is purchased for a set period and provides a payout if the insured dies during that term. Cash value policies accrue value over time and can be withdrawn by the policy owner while they are still alive.

Term life insurance is the most straightforward type of life insurance. It is also the most affordable option, with lower rates than whole life insurance. You can choose the term length that suits you best, and it is a good option for those with specific timelines they want to plan around. However, it does not accrue value over time, and you will have to pay higher rates if you want to extend your coverage.

Whole life insurance is a good option for those seeking a low-maintenance policy that will cover them for their entire life. It also allows you to leave behind a sizable amount of tax-free money for your loved ones. However, it is initially much more expensive than term life insurance. Universal life insurance is another type of cash value policy that offers more flexibility when it comes to premium payments. However, the interest on the cash value of a universal policy is dependent on market interest rates, which means you could earn less when the market is down.

You should consider your budget, your coverage duration, and your final expenses. You should also consider the needs of your loved ones, including their future finances and any debts that will need to be paid off. Finally, you should consider whether you want to include additional family members on your policy.