Life insurance policies can be sold by their owners to a third party, often a life settlement provider, in exchange for a cash payout. This is known as a life settlement. The new owner of the policy will pay any future premiums and receive the death benefit when the person whose life is insured dies. Most types of policies qualify for a life settlement, even term life insurance policies. People who sell their life insurance policies are typically over the age of 60 and may do so to cover medical bills and additional living expenses, or simply because they no longer need the policy. Life insurance can also be sold by insurance agents, who are usually compensated through commissions and bonuses. To sell life insurance, agents must comply with state licensing requirements, which may include passing an exam and undergoing a criminal background check.

Characteristics of Life Insurance Policies

| Characteristics | Values |

|---|---|

| Life insurance policy owners can sell their policies | For cash, it is known as a life settlement |

| Who can sell their life insurance policies? | Typically people over the age of 60 |

| How much can you get for selling your life insurance policy? | The average payout is 4-6 times the policy's cash surrender value |

| What are the factors that can impact the cash received from the sale? | The number of successful sales, the specifics of the case |

| What are the pros of selling a life insurance policy? | Cover medical bills and additional living expenses, get more money than if you surrender it back to the insurance company |

| What are the cons of selling a life insurance policy? | It is a highly competitive work environment that can lead to stress and burnout |

| What are some common reasons to consider selling a life insurance policy? | High monthly insurance premiums, changes in the insurance market or poor policy performance, unexpected financial issues, economic changes or hardships |

| What are the steps to sell life insurance? | Comply with the licensing requirements of the state, complete pre-licensing education requirements, pass an insurance licensing exam, apply for a license, receive a National Producer Number (NPN), find a job with a life insurance company or start your own |

| What are some sales tips for selling life insurance? | Networking and using referrals, creating a website and profiles on social media platforms, presenting yourself well and demonstrating empathy |

Explore related products

What You'll Learn

![]()

Life insurance sales roles

To become a life insurance sales agent, there are a few steps you need to take. Firstly, you'll need to complete the necessary education and licensing requirements, which vary depending on your state. This usually involves completing a specific number of hours of coursework and passing a licensing examination. Once you've obtained your license, you can choose to work for an insurance company or start your own business. If you work for an employer, they may provide you with leads, but if you're independent, you'll need to generate your own leads through networking, referrals, and marketing.

When selling life insurance, it's important to understand the different types of policies available and be able to explain the benefits to potential clients in a language they understand. It's about more than just listing features; it's about presenting solutions to their concerns. For example, you might ask questions about their savings and how their family would cope financially if they were to pass away or become hospitalized for an extended period. This approach, known as solution selling, is often more effective than simply listing features like a 24/7 helpline.

Developing expertise in a specific area of life insurance can help you stand out and build your brand. You can choose to offer a range of plans or specialize in a particular type of policy, such as term life insurance or universal life insurance. Additionally, some life insurance agents expand their offerings to include health insurance policies. By focusing on a specific area, you can establish yourself as an expert and make it easier to sell life insurance from home, providing you have the right equipment and a quiet workspace.

Who Gets Your Life Insurance Money: Contingent Beneficiaries Explained

You may want to see also

Explore related products

![]()

How to sell your life insurance policy

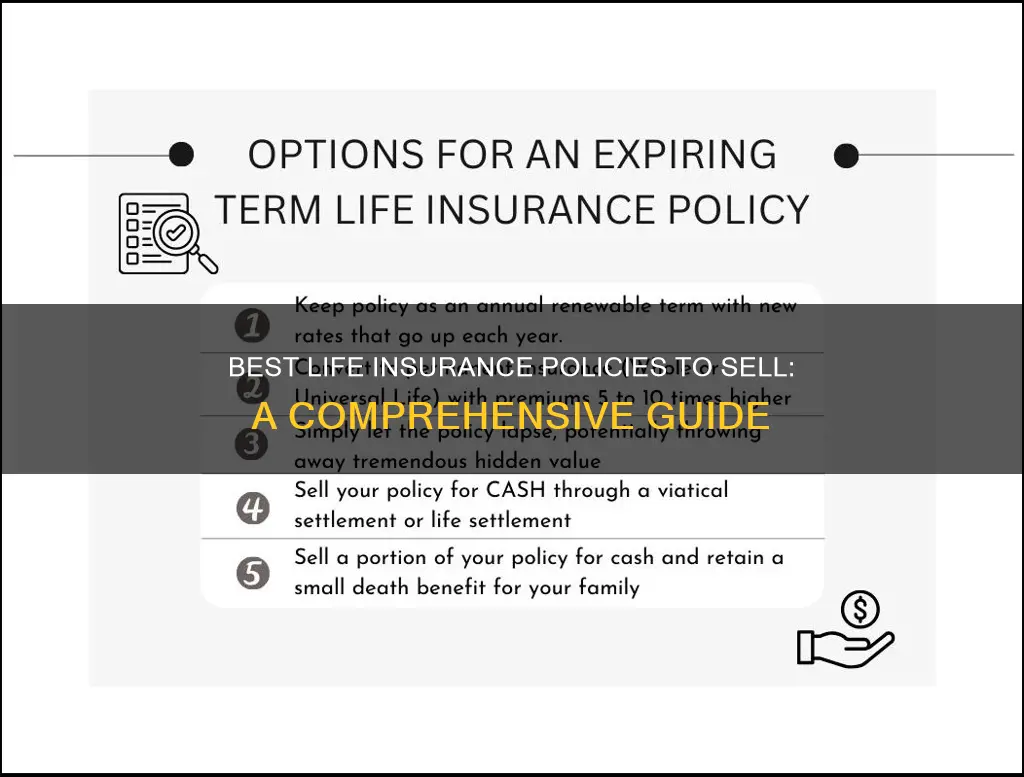

If you're looking to sell your life insurance policy, there are a few things you should know. Firstly, selling your life insurance policy is known as a life settlement, and it involves selling your policy to a third-party buyer for a cash payout. This payout is typically more than the policy's cash surrender value but less than its total face value.

Most types of policies qualify for a life settlement, and you can generally sell your policy if you're over 60, although this isn't a requirement. A decline in health since the policy was issued can also improve your chances of qualifying. It's important to note that you have the right to change your mind about the life settlement transaction even after receiving the proceeds, and you can rescind the contract up to 15 days after receiving the proceeds.

To sell your life insurance policy, you'll first need to meet certain minimum requirements, which you can determine by submitting your policy for a free evaluation. If you meet the basic qualifying factors, you'll then complete a detailed health questionnaire. Once a life settlement provider has all the necessary information and decides to make an offer, they will present the specifics of the offer and explain the next steps. At this point, you can accept the full cash offer or opt for an alternative, such as a Retained Death Benefit, which allows you to receive a smaller cash payment while keeping a portion of your policy's benefits with no future premium obligations.

If you're planning to sell your policy, it's recommended to consult a professional financial advisor, attorney, or accountant to determine if it's the best option for you. There may be other alternatives, such as taking out a policy loan or reducing the death benefit to lower your premium payments.

Now, if you're interested in selling life insurance as a career, there are a few steps you need to take. Firstly, you must comply with your state's licensing requirements, which include completing pre-licensing education and passing an insurance licensing exam. You'll then need to apply for a license, receive a National Producer Number (NPN), and decide whether to work for a life insurance company or start your own business. It's also important to understand the local and national laws around selling life insurance. Once you're licensed and have chosen your work setup, you can start selling. This involves generating leads, presenting yourself well, and demonstrating to clients how your insurance products can benefit them.

Life Insurance Claims: Time Limits After Death

You may want to see also

Explore related products

![]()

Life settlement providers

Some prominent life settlement providers include Abacus Life Settlements, Vespera Life, LLC, Life Settlement Solutions LLC, LifeRoc Capital, LLC, and Magna Life Settlements, Inc. These companies are licensed to operate in specific states and adhere to regulations governing the life settlement industry.

The process of selling a life insurance policy to a life settlement provider typically involves the following steps:

- The seller contacts multiple life settlement providers or uses a licensed broker to obtain offers.

- The provider evaluates the policy and the seller's health information to determine a fair price.

- The provider makes an offer, which the seller can accept or negotiate.

- The closing process involves transferring ownership of the policy and its accompanying documentation.

- The settlement payment is placed in escrow until the insurance company verifies the change of ownership.

- Once verified, the settlement payment is released to the seller.

It is important for individuals considering selling their life insurance policy to understand the potential impact on their finances and their survivors' future financial needs. Additionally, privacy concerns arise as the buyer may gain access to the seller's personal and health information.

How Spouses Can Change Life Insurance Address Details

You may want to see also

Explore related products

![]()

Pros and cons of selling your life insurance policy

Selling your life insurance policy can be a great way to get money for your unwanted policy, but there are some things you should keep in mind. Here are some pros and cons to help you decide if selling your life insurance policy is the right choice for you.

Pros:

- You get the value of your policy now. This can be especially useful if you need money for medical bills, additional living expenses, or other financial obligations.

- You can get more cash by selling your policy than by surrendering it or letting it lapse. A life settlement often provides a higher return on the death benefit of the policy, which means you could get a significant lump sum.

- You reduce or eliminate the burden of costly premiums. If you can no longer afford your premiums, selling your policy can provide financial relief.

- It can be a good option if you no longer need or want your policy. For example, if your family is already well-supported and doesn't need the payout from your policy.

Cons:

- Your beneficiaries will no longer receive a death benefit when you pass, and your coverage will end. This means they won't have the financial support you intended for them, so it's important to consider their needs before selling your policy.

- Life settlements are considered taxable income. You will have to pay taxes on any amount you earn that exceeds the premiums you have paid, which can reduce the overall benefit of selling your policy.

- There may be other options available to you if you can no longer afford your premiums. Your insurer may be able to help you adjust your policy to make it more affordable for your current lifestyle. It's worth exploring these alternatives before making a decision.

- Your health and age can impact the value of your policy. A decline in health or an increase in age since the policy was issued can improve your chances of qualifying for a life settlement, but it's not a guarantee. Each case is unique, and other factors may also come into play.

Understanding Life Insurance: Loss Ratios and Their Implications

You may want to see also

Explore related products

$34.99 $35

$9.97 $19.99

![]()

Tips for selling life insurance

Selling life insurance is about more than just selling a product. As a life insurance agent, you are promising to protect your clients' families and help them achieve their dreams and financial goals. Building trust and strong relationships with your clients is crucial to your success. Here are some tips to help you sell life insurance:

Get Licensed and Certified

Before you start selling life insurance, you need to complete the necessary education and pass a licensing exam. In the US, you will also need to meet certain educational and ethical insurance industry requirements to become a licensed insurance sales agent. You may also need to complete additional business courses or certifications to sell certain types of policies or work with specific companies.

Understand the Product

Understanding the product inside out is key to selling life insurance successfully. You need to be able to communicate the business benefits, terms, and conditions of the insurance policies clearly and accurately to your clients. Keep up to date with insurance industry changes, new product launches, and market trends to recommend the most suitable policies for your clients' needs and goals.

Build Relationships

Cultivate trust with your clients by being transparent and honest about the product, pricing, advantages, and potential dangers. Keep your commitments, provide outcomes, and follow up with clients to preserve trust. Actively listen to their concerns, anxieties, and financial objectives to give effective, tailored solutions. Building relationships will also help you get referrals and increase client retention and revenue.

Generate Leads

If you're working as a captive agent, your employer may provide you with leads. If you're working independently, you will need to generate leads through networking, referrals, and purchasing lists. You can also engage insurance marketing organizations or field marketing organizations to help with marketing and lead generation.

Focus on Solutions

When pitching to leads, speak in a language your prospects understand and demonstrate empathy with their situations. Focus on how your insurance products can solve their problems and safeguard them and their families in the case of injury, hospitalization, or death.

Cross-Sell and Upsell

Mention life insurance and its benefits to every customer and encourage staff members to do the same. Offer no-obligation life insurance reviews and provide quick quotes to educate customers on their options. Keep in regular contact with your customers to ensure their coverage is still right for their situation and remind them of your personalized service.

Convertable Life Insurance: Cash Value and Benefits Explained

You may want to see also

Frequently asked questions

Yes, you can sell your life insurance policy. This is known as a life settlement, and it involves selling your policy to a third-party buyer for a cash payout.

A pro of selling your life insurance policy is that you can receive a cash payout that is more than the policy's cash surrender value. You can use this money for any purpose, such as funding assisted living, medical costs, or travelling. A con is that you will no longer have the financial protection that the policy provided, and you may need to pay taxes on the proceeds.

To sell your life insurance policy, you will need to meet certain minimum requirements, such as being over the age of 60 or having a decline in health. You can then find a life settlement provider, who will make you an offer for your policy. If you accept the offer, you will transfer ownership of the policy and receive your payment.

To become a life insurance salesperson, you will need to complete your state's pre-licensing education requirements, pass an insurance licensing exam, apply for a license, and receive a National Producer Number (NPN). You can then find a job with a life insurance company or start your own business.