Group life insurance is a single contract that provides coverage to a group of people, typically those employed by the same company. It is offered by an employer or another large-scale entity, such as an association or labor organization, to its workers or members. While it is generally inexpensive and easy to qualify for, there are some groups that may not be eligible for coverage. This includes individuals who are not actively employed by the company offering the policy, those who have not met the minimum probationary period, and those who do not meet the minimum number of participants required for group coverage in certain states.

Explore related products

What You'll Learn

![]()

Those who are unemployed or retired

Group life insurance is offered by an employer or another large-scale entity, such as an association or labor organization, to its workers or members. It is typically inexpensive and may even be free for certain employees. Coverage is guaranteed to all group members, and qualifying is easy as it does not require a medical exam or underwriting.

However, if you are unemployed, you will lose out on key benefits such as group life insurance. If your employer eliminates your position, a group life insurance policy will not cover you while you are out of work. To secure your life insurance coverage while unemployed, you will need to cancel your group life insurance benefits and purchase a private life insurance policy. Your employment status does not usually impact your ability to purchase a new private life insurance policy, and many carriers offer life insurance for unemployed individuals who are also disabled. However, it is important to note that your health issues may dictate the type and amount of coverage you can get.

If you are retired, you may be able to keep your existing basic life insurance coverage if you meet certain conditions. These include being enrolled in basic life insurance under the Federal Employees' Group Life Insurance (FEGLI) program when you retire, not having converted your life insurance coverage to an individual policy, and having had life insurance coverage for the five years immediately preceding retirement or for the full periods of federal service when coverage was available. If you are not eligible to continue coverage into retirement, you will be given the opportunity to convert to an individual policy.

It is important to note that if you leave your employer, your group life insurance coverage will usually stop. However, you may be able to convert your life insurance policy to an individual policy, although your premium after conversion may be higher.

Understanding Interest Calculation on Life Insurance Cash Value

You may want to see also

Explore related products

![]()

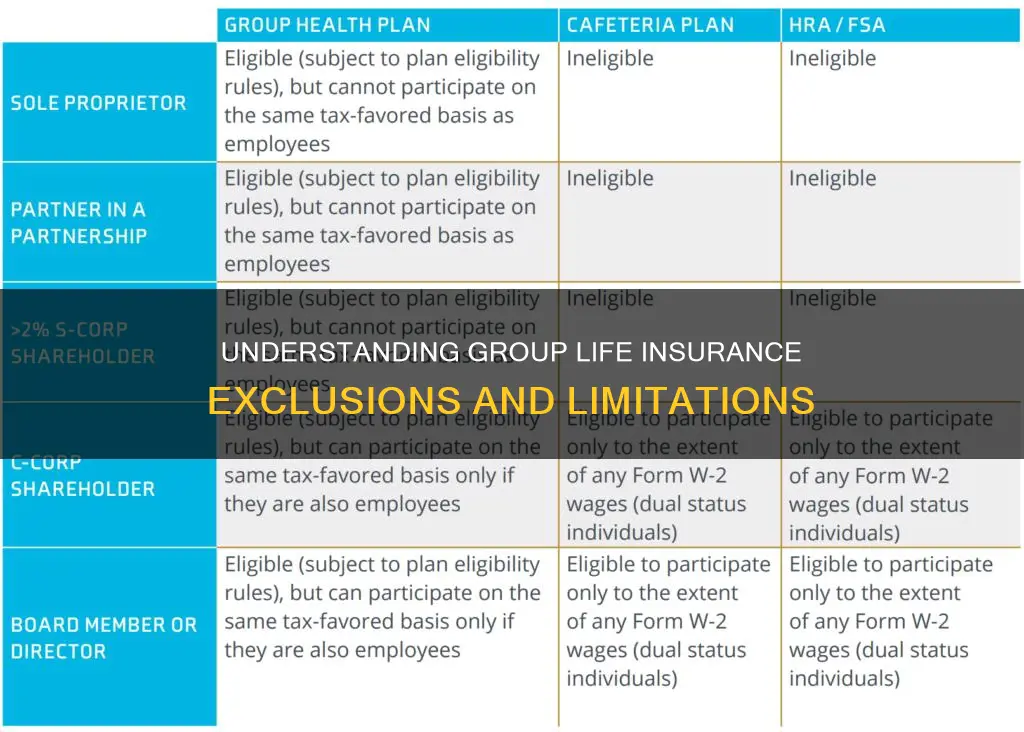

Those who are self-employed or work for a different company

Group life insurance is a single contract that provides coverage to a group of people, typically those who work for the same company. The employer owns the policy, which covers the employees. This means that those who are self-employed or work for a different company are not eligible for group life insurance.

Self-employed individuals do not have access to the same insurance benefits as those who work for a company that provides group life insurance. Instead, they must purchase their own insurance. This includes life insurance, as well as other types of insurance such as disability, health care, and dental insurance. Self-employed individuals can compare rates on the Health Insurance Marketplace and may qualify for tax credits and cost-sharing reductions. They should research and understand their insurance options to determine the best policies to fit their financial needs.

Life insurance options for the self-employed include term, whole, and universal life insurance, each with unique benefits. Critical illness insurance is another option that self-employed individuals may want to consider. This type of insurance helps provide coverage for serious, life-threatening illnesses. It can complement health insurance for self-employed individuals, as it pays out a cash benefit that can be used to maintain quality of life, pay off debts, or supplement lost income.

It is important for self-employed individuals to have insurance to protect themselves, their families, and their businesses in the case of an accident, a medical issue, or other unexpected events. This is especially true since self-employed individuals may face financial risks that traditional employees do not, such as paying for their own insurance and self-employment taxes. By purchasing insurance, self-employed individuals can ensure that their families will be financially protected in the event of their death.

Life Insurance in India: Understanding the Basics

You may want to see also

Explore related products

![]()

Those who have not met the minimum probationary period

Group life insurance is offered by an employer or another large-scale entity, such as an association or labor organization, to its workers or members. It is usually inexpensive and may even be free for certain employees.

Some organizations require group members to participate for a minimum amount of time before they are granted coverage. This is known as the probationary period, which is typically 90 days, but can vary depending on the organization and the specific group insurance plan. During this time, new employees may not be eligible for group life insurance benefits. The probationary period allows the insurer to assess the risk associated with providing coverage to a new employee. It also helps the organization manage costs and ensure that employees are committed to their jobs.

The probationary period requirement for group life insurance is important because it incentivizes employees to stay with the company for a certain duration. This reduces turnover rates and encourages a sense of loyalty and stability within the workforce. Additionally, it gives the insurance company time to evaluate the overall health and risk factors of the group, rather than focusing on individual members, which is a key difference between group and individual life insurance policies.

While the probationary period may delay access to group life insurance benefits, it is generally a straightforward process to qualify for coverage once this period has been completed. Group life insurance is a valuable perk that provides financial security to beneficiaries in the event of an employee's death. It is also beneficial for those who may have trouble qualifying for individual policies due to health issues, as group policies often have more lenient underwriting standards.

Military Kids and Life Insurance: What's the Deal?

You may want to see also

![]()

Those who have not opted for coverage for their spouse and/or children

Group life insurance is a single contract that provides coverage to a group of people, typically those who work for the same company. The employer owns the policy, which covers the employees. The most common group life insurance policy is provided by employers, although some churches, professional associations, alumni groups, unions, and other affiliate organizations also offer group life insurance to members.

Group life insurance is a common part of employee benefit packages. Many employers provide, at no cost, a base amount of coverage as well as an opportunity for the employee to purchase additional coverage through payroll deductions. The insurance plan may also offer employees the option to buy coverage for their spouses and children. This is known as voluntary dependent life insurance.

Some employers give employees the option to buy a limited amount of group coverage for spouses and children. Age eligibility for children varies. For example, Family Servicemembers' Group Life Insurance (FSGLI) offers coverage for the spouse and dependent children of service members covered under full-time SGLI. Dependent children get free coverage until the child is 18 years old, and in some cases, coverage may be extended if the child meets certain requirements.

Group life insurance is a great way to get coverage if you have trouble qualifying for an individual policy due to health issues. This is because the underwriting standards are often more lenient for group policies. However, it's important to note that group life insurance generally comes with only basic coverage, which may not fulfill the needs of policyholders. As such, it should be treated as a perk and supplemented with a separate individual policy.

Hawaii Life Insurance: Renewal Timeframe and Considerations

You may want to see also

![]()

Those who have not purchased additional coverage beyond the basic insurance

Group life insurance is a single contract that provides coverage to a group of people, typically those who work for the same company. It is offered by an employer or another large-scale entity, such as an association or labor organization, to its workers or members. The employer owns the policy, which covers the employees, and the benefits are determined by the employer. The most common group life insurance policy is provided by employers, but some churches, professional associations, alumni groups, unions, and other affiliate organizations also offer group life insurance to members.

Group life insurance is generally inexpensive, especially for younger people, and the rates increase with age. It is often cheaper than an individual life insurance policy, and it does not require a medical examination or underwriting. This makes it a good option for those who may have trouble qualifying for individual policies due to health issues. Typically, all eligible employees are automatically enrolled in the base coverage once they meet the eligibility requirements, which may include working a certain number of hours per week or having been an employee for a specified length of time.

While group life insurance is easily accessible and affordable, it usually only provides basic coverage. The amount covered by the employer is typically $50,000 of tax-free group term life insurance, which may not be sufficient to meet the financial needs of the policyholder's loved ones. This basic coverage may only be enough to pay for funeral expenses and clear a few debts, but it may not be enough to cover larger expenses such as a mortgage, college tuition, or family living expenses. Therefore, those who only have the basic insurance provided by their employer may find that the coverage is not adequate for their needs.

To address this limitation, some employers offer supplemental group term coverage, allowing employees to purchase additional coverage beyond the base insurance. This extra voluntary coverage is still based on the less expensive group rate, and it may even be portable between jobs. However, it often requires applicants to answer a medical questionnaire or undergo a simplified underwriting process to determine eligibility. By purchasing this additional coverage, employees can ensure that their loved ones receive a more substantial benefit that can help cover larger expenses.

Life Insurance and Prenups: Structuring Your Future

You may want to see also

Frequently asked questions

Group life insurance is offered by an employer or another large-scale entity, such as an association or labor organization, to its workers or members. This means that those who are not workers or members of the organization providing the insurance are not eligible for group life insurance.

Yes, some organizations require group members to participate for a minimum amount of time before they are granted coverage. This is usually a probationary period of 90 days, but it can vary. Some policies may also require that employees work a certain number of hours per week to qualify.

If an individual leaves the organization, their coverage usually stops. However, some organizations allow ex-employees to maintain the same coverage, known as "porting" the life insurance.

Group life insurance generally comes with only basic coverage, which may not fulfill the needs of policyholders. It is also important to note that the employer controls the policy, which means premiums can increase based on decisions made by the employer.