Medicare is a health insurance program that provides coverage for around 60 million people in the United States, including older adults and younger adults with disabilities. While Medicare is the primary payer for most beneficiaries, many individuals also have supplemental insurance, also known as Medigap, to help cover additional costs. In 2016, eight in ten beneficiaries in traditional Medicare had some form of supplemental coverage, and this number has increased over time. Supplemental insurance can include employer-sponsored insurance, Medigap policies, or Medicaid, each offering varying levels of additional protection.

| Characteristics | Values |

|---|---|

| Percentage of Medicare beneficiaries with supplemental insurance in 2016 | 81% |

| Percentage of Medicare beneficiaries with no supplemental insurance in 2016 | 19% |

| Percentage of Medicare beneficiaries with employer-sponsored insurance in 2016 | 30% |

| Percentage of Medicare beneficiaries with Medigap in 2016 | 29% |

| Percentage of Medicare beneficiaries with Medicaid in 2016 | 22% |

| Percentage of Medicare beneficiaries with no supplemental coverage in 2018 | 10% |

| Percentage of Medicare beneficiaries with no supplemental coverage in 2022 | 5% |

| Percentage of Medicare beneficiaries with supplemental insurance in 2022 | 95% |

| Percentage of Medicare beneficiaries with Medigap in 2022 | 21% |

| Percentage of Medicare beneficiaries with Medigap in traditional Medicare in 2022 | 42% |

| Percentage of traditional Medicare beneficiaries under 65 with Medigap | 2% |

| Percentage of traditional Medicare beneficiaries over 65 with Medigap | 11% |

| Percentage of Medicare beneficiaries with employer-sponsored insurance in 2022 | 24% |

| Percentage of Medicare beneficiaries with private supplemental coverage in 2019 | 22% |

| Percentage of Medicare beneficiaries with retiree coverage in 2019 | 18% |

Explore related products

What You'll Learn

- Medicare supplement insurance (Medigap) covered 42% of people on traditional Medicare in 2022

- % of Medicare beneficiaries had no supplemental coverage in 2016

- Medicaid was a supplemental source for 19% of all Medicare beneficiaries in 2022

- Medicare Advantage plans are an alternative to traditional Medicare

- Medicare beneficiaries with supplemental coverage from group health insurance plans

![]()

Medicare supplement insurance (Medigap) covered 42% of people on traditional Medicare in 2022

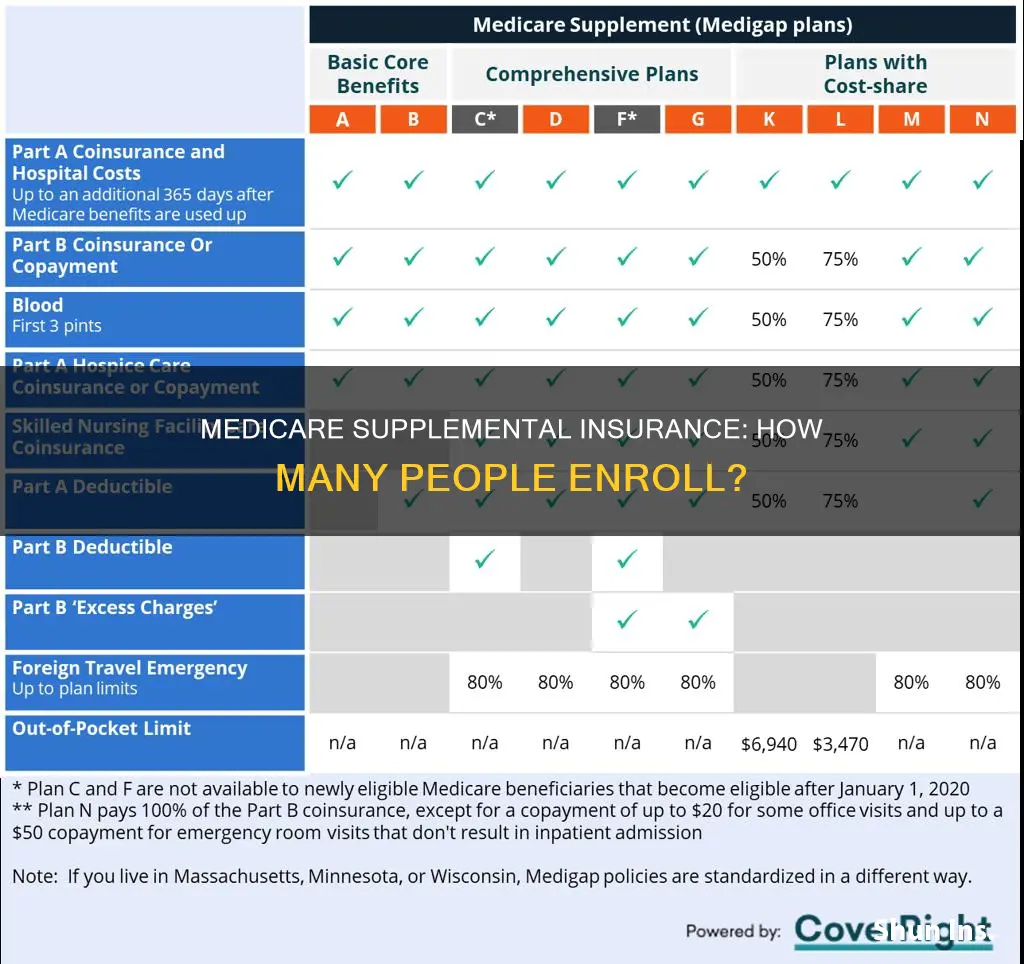

Medicare supplement insurance, also known as Medigap, is an extra insurance policy that can be purchased from a private company to help cover the costs of Original Medicare (Parts A and B). In 2022, Medigap covered 42% of people on traditional Medicare, which equates to around 12.5 million beneficiaries. This figure represents an increase in Medigap coverage among traditional Medicare users, as in 2016, only 29% of people on traditional Medicare had Medigap policies.

Medigap policies can help to limit the financial exposure of Medicare beneficiaries by covering some or all of Medicare Parts A and B cost-sharing requirements, including deductibles, copayments, and coinsurance. Additionally, some Medigap policies offer coverage for medical expenses incurred while travelling outside the US. However, it is important to note that Medigap generally does not cover long-term care, such as nursing home stays, vision, dental, hearing aids, private-duty nursing, or prescription drugs.

The percentage of people on traditional Medicare with Medigap coverage varies across different demographic groups. For instance, in 2016, beneficiaries with Medigap tended to have higher incomes and education levels and were more likely to be white compared to all traditional Medicare beneficiaries. Additionally, only a small share of Medigap policyholders (3%) were under the age of 65 and qualified for Medicare due to a disability. Federal law does not require insurers to sell Medigap policies to individuals under 65, even if they qualify for Medicare due to a long-term disability. As a result, individuals under 65 with disabilities may face challenges in obtaining Medigap coverage.

The availability and protection of Medigap policies also depend on state regulations and the open enrollment period. During the open enrollment period, Medigap coverage must be offered on a guaranteed-issue basis, and premiums cannot vary based on health status. However, outside of this period, most states allow medical underwriting, and insurers may deny coverage or charge higher premiums to individuals with pre-existing conditions.

Medical Insurance Coverage for Scleral Lenses: What You Need to Know

You may want to see also

Explore related products

![]()

19% of Medicare beneficiaries had no supplemental coverage in 2016

Medicare is the primary payer for beneficiaries in most cases, with any supplemental coverage acting as a secondary or "wraparound" coverage. Supplemental insurance coverage typically covers some or all of Medicare Part A and Part B cost-sharing requirements and, in some instances, covers benefits that Medicare does not. In 2016, 81% of beneficiaries in traditional Medicare had some form of supplemental insurance, including employer-sponsored insurance (30%), Medigap (29%), and Medicaid (22%).

However, 19% of Medicare beneficiaries, or 6.1 million people, had no supplemental coverage in 2016. These individuals were more likely to be older, male, and have modest incomes between $20,000 and $40,000. Without supplemental coverage, these beneficiaries were fully exposed to Medicare's cost-sharing requirements and lacked the protection of an annual limit on out-of-pocket spending. This placed them at greater financial risk, potentially incurring high medical expenses or foregoing medical care due to costs.

The number of traditional Medicare beneficiaries without supplemental coverage has declined in recent years. Between 2018 and 2022, the percentage of total Medicare enrollees without supplemental coverage dropped from 10% to 5%. This decline is likely due to the increasing popularity of Medicare Advantage plans, which provide an out-of-pocket spending cap and covered 54% of all eligible beneficiaries in 2024.

Medigap, also known as Medicare Supplement Insurance, is sold by private insurance companies and can help cover deductibles, copayments, and coinsurance. While Medigap policies can provide valuable financial protection, they may not be accessible to everyone. Federal law does not require insurers to sell Medigap policies to beneficiaries under 65, and premiums may be higher for this age group. Additionally, Medigap policies typically do not cover long-term care, vision, dental, hearing aids, private-duty nursing, or prescription drugs.

Navigating Options When Insurance Refuses Medication Coverage

You may want to see also

Explore related products

![]()

Medicaid was a supplemental source for 19% of all Medicare beneficiaries in 2022

Medicare is a health insurance programme that provides coverage for around 60 million people in the United States, including 51 million older adults and 9 million younger adults with disabilities. Medicare beneficiaries can choose to receive their benefits (Part A and Part B) through the traditional Medicare programme or by enrolling in a Medicare Advantage plan.

Medicare Supplement Insurance, also known as Medigap, is an extra insurance policy that beneficiaries can purchase from private companies to help pay their share of costs in Original Medicare. Medigap policies fully or partially cover Medicare Part A and Part B cost-sharing requirements, including deductibles, copayments, and coinsurance. In 2022, Medigap covered 21% of Medicare beneficiaries overall, or 42% of those in traditional Medicare.

It is important to note that Medicare beneficiaries with no supplemental coverage are fully exposed to Medicare's cost-sharing requirements and may face higher out-of-pocket expenses. In 2022, the number of traditional Medicare beneficiaries without supplemental coverage declined to 3.2 million, or 5% of the total Medicare population.

Among those with supplemental insurance, Medicaid was a supplemental source for 19% of all Medicare beneficiaries in 2016. Medicaid is a federal-state programme that provides health and long-term care coverage to low-income individuals. It is designed to help those with low incomes and modest assets, ensuring they have access to necessary medical care.

In summary, while the majority of Medicare beneficiaries have some form of supplemental insurance, a small proportion rely on Medicaid as their supplemental source. This highlights the importance of supplemental coverage in ensuring that individuals have comprehensive health insurance protection.

Medicaid Insurance Changes in Illinois: When Can You Switch?

You may want to see also

Explore related products

![]()

Medicare Advantage plans are an alternative to traditional Medicare

Medicare Advantage plans, also known as Part C, are an alternative to Original Medicare. In 2024, nearly 33 million people, or 54% of eligible Medicare beneficiaries, were enrolled in a Medicare Advantage plan. This is a notable increase from 2018, when one-third of Medicare beneficiaries were enrolled in Medicare Advantage plans.

Medicare Advantage plans are offered by private companies that must follow rules set by Medicare. They often include Part A, Part B, and Part D (drug coverage) all in one plan. Medicare Advantage plans may have zero-dollar premiums, extra benefits, and reduced cost-sharing for many services, with an out-of-pocket spending limit.

However, Medicare Advantage plans have provider networks that limit you to their doctors, and they may not cover out-of-network providers. If you want to use a doctor that isn't in the network, your costs will increase. By contrast, with Original Medicare, you can choose any primary care doctor or specialist who accepts Medicare, and you don't need referrals to see a provider.

Medicare Advantage plans also have prior authorization requirements, whereas Original Medicare does not. Additionally, it is important to note that insurance companies can decide to join or leave Medicare each year. If a plan decides to stop participating, you will need to join another Medicare health plan or return to Original Medicare.

When deciding between Original Medicare and a Medicare Advantage plan, consider your specific needs, preferences, and the trade-offs between the two options.

Accident Indemnity Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

Medicare beneficiaries with supplemental coverage from group health insurance plans

Medicare beneficiaries can choose to receive their benefits through the traditional Medicare programme or by enrolling in a Medicare Advantage plan. In 2018, two-thirds of beneficiaries opted for traditional Medicare, while one-third chose a Medicare Advantage plan. Many beneficiaries with traditional Medicare also rely on other sources of supplemental coverage, such as Medigap, Medicaid, or employer-sponsored insurance.

Medicare Supplement Insurance, or Medigap, is an extra insurance policy that beneficiaries can purchase from private companies to help pay their share of costs in Original Medicare. Medigap policies fully or partially cover Medicare Part A and Part B cost-sharing requirements, including deductibles, copayments, and coinsurance. In 2022, Medigap covered 21% of Medicare beneficiaries overall, or 42% of those in traditional Medicare.

In 2016, eight in ten beneficiaries in traditional Medicare had some type of supplemental insurance, including employer-sponsored insurance (30%), Medigap (29%), and Medicaid (22%). However, by 2019, approximately 10% of Medicare beneficiaries had no supplemental coverage, while 90% had varying sources and degrees of private or public supplemental coverage. Specifically, 22% had purchased private Medigap policies, and 18% had retiree coverage through a former employer.

Federal law provides a six-month guarantee issue protection for adults aged 65 and older when they first enrol in Medicare Part B if they wish to purchase a supplemental Medigap policy. During this open enrolment period, Medigap insurers cannot deny coverage based on age, gender, or health status, and premiums cannot vary by health status. However, most states do not require insurers to issue Medigap policies to beneficiaries under age 65, and protections typically do not extend beyond the one-time open enrolment period.

When Medicare is the primary payer, as it usually is, any supplemental coverage from a group health insurance plan acts as the secondary payer, providing "wraparound" coverage for any remaining balance. Medicare is the primary payer for beneficiaries with supplemental coverage through a group health insurance plan under specific conditions outlined in the Medicare Secondary Payer provisions. These conditions include being 65 or older and enrolled in a group health plan with fewer than 20 employees, or having a disability and being under 65 with a group health plan with fewer than 100 employees.

Understanding Therapy Coverage with Medical Insurance

You may want to see also

Frequently asked questions

19% of people on traditional Medicare, or 6.1 million beneficiaries overall, had no supplemental coverage in 2016.

In 2022, 21% of all Medicare beneficiaries had Medigap coverage, including 42% of those in traditional Medicare. In 2016, 29% of traditional Medicare beneficiaries had Medigap coverage.

In 2022, 24% of all Medicare beneficiaries had some form of employer-sponsored health insurance coverage in addition to Medicare Part A and Part B. In 2016, 30% of traditional Medicare beneficiaries had employer-sponsored supplemental insurance.

In 2016, 22% of traditional Medicare beneficiaries with low incomes and modest assets had Medicaid as a source of supplemental coverage. In 2019, 9% of all Medicare beneficiaries had Medicaid as a supplemental coverage.