Medicare health plans are available to those in Pasadena, MD, and are offered by private companies that contract with Medicare. There are several types of plans to choose from, including Original Medicare, which includes Part A (Hospital Insurance) and Part B (Medical Insurance). Medicare Advantage Plans (Part C) are another option, offered by Medicare-approved private companies, and often include drug coverage (Part D). For those on low incomes, there is the Medicare Buy-In Program, also known as QMB (Qualified Medicare Beneficiary) and SLMB (Specified Low-Income Medicare Beneficiary), which helps to cover the costs of Medicare coverage.

Medicare Insurance in Pasadena, MD

| Characteristics | Values |

|---|---|

| Medicare health plans | Part A (Hospital Insurance) and Part B (Medical Insurance) |

| Medicare Advantage Plans | Part C (offered by Medicare-approved private companies) |

| Other names for Part C | MA plan, Health Maintenance Organizations (HMOs), Preferred Provider Organizations (PPOs) |

| Other types of Medicare health plans | Special Needs Plans (SNPs), Medicare Medical Savings Accounts (MSAs), Private Fee-for-Service Plans (PFFS) |

| Medicare Advantage Plan disenrollment reasons | Moving outside the plan's service area, losing Medicare or Medicaid eligibility, joining a drug plan, or if the plan's contract with Medicare ends |

| Medicare Buy-In Program | QMB (Qualified Medicare Beneficiary), SLMB (Specified Low-Income Medicare Beneficiary) |

| QMB eligibility | Individuals with modest assets (up to $9,090 per individual or $13,630 per couple) with combined incomes that do not exceed 100% of the federal poverty level |

| SLMB eligibility | Incomes between 100% and 120% of poverty with assets up to $9,090 per individual or $13,630 per couple |

| Other programs | Maryland Children's Health Insurance Program (MCHP), Medicaid (Medical Assistance) |

Explore related products

What You'll Learn

![]()

Medicare Advantage Plans

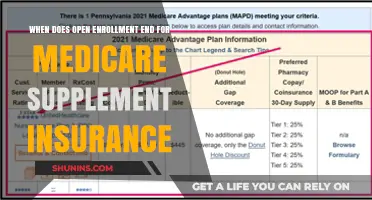

In Maryland, there are four types of Medicare Advantage Plans: Health Maintenance Organization (HMO), Preferred Provider Organization (PPO), Private Fee-for-Service (PFFS), and Special Needs Plan (SNP). Each type offers a different level of flexibility in choosing your care providers and varies in price. For example, with an HMO plan, you will generally have lower out-of-pocket costs but will need to choose a primary care physician from within the plan's network and will typically need a referral to see a specialist. With a PPO plan, you will have more flexibility to see out-of-network providers but will generally pay higher out-of-pocket costs.

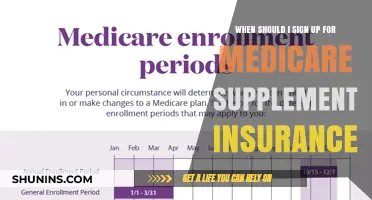

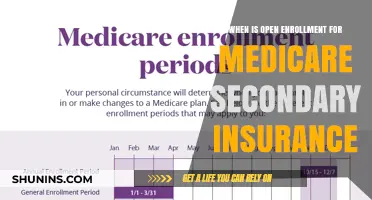

You can switch to a Medicare Advantage Plan during the Annual Election Period, which runs from October 15 to December 7. During this period, you can also switch between Medicare Advantage Plans or go back to Original Medicare. It's important to do your research and compare the different plans available in your area to find the one that best suits your needs. You can seek help from trained, unbiased counselors or utilize free resources such as the State Health Insurance Assistance Program (SHIP) in Maryland.

Some of the top-rated Medicare Advantage Plans in Maryland are offered by UHC, Aetna, and Kaiser Permanente. These plans often include additional benefits beyond Original Medicare, such as cost savings on dental and vision coverage. In 2025, the average monthly premium for a Medicare Advantage Plan in Maryland is expected to be $30.92, and all Medicare-eligible people in Maryland have access to a $0-premium plan.

Medical Malpractice: Insurance Liability and Legal Action

You may want to see also

Explore related products

![]()

Medicare Savings Programs

To qualify for a Medicare Savings Program, you typically must have an income and resources below a certain limit, although these limits vary by state and tend to increase each year. Some states do not consider certain types or amounts of income or resources when determining eligibility. Additionally, income limits are slightly higher in Alaska and Hawaii.

There are several types of Medicare Savings Programs, including:

- Qualified Medicare Beneficiary (QMB) program: Covers Parts A and B premiums, deductibles, coinsurance, and copayments.

- Specified Low-Income Medicare Beneficiary (SLMB) program: Covers Part B premiums.

- Qualifying Individual (QI) program: Available for those who do not qualify for any other Medicaid coverage or benefits; covers Part B premiums.

- Qualified Disabled & Working Individual (QDWI) program: Covers Part A premiums.

If you are already enrolled in Medicare and want help with the costs, you can apply for a Medicare Savings Program through your state. Even if you do not meet the income requirements, it is recommended that you still apply, as you may qualify for other programs.

Medical Insurance: Who's Covered and Who's Not?

You may want to see also

Explore related products

![]()

Qualified Medicare Beneficiary

The Qualified Medicare Beneficiary (QMB) program is one of four Medicare Savings Programs (MSPs) sponsored by Medicaid. The program covers Medicare Part A and Part B premiums, deductibles, copayments, and coinsurance for people with limited income and assets.

In 2023, more than 8 million individuals (more than 1 out of 8 Medicare beneficiaries) were in the QMB group. The QMB program is designed to help low-income Medicare beneficiaries with their out-of-pocket costs. It covers the entire Medicare Part B premium, which is $185 a month for most beneficiaries as of 2025. This adds up to an annual savings of $2,220.

To be enrolled in the QMB program, you must be enrolled in Medicare Part A at a minimum and meet strict income and asset limits. These limits are based on the Federal Poverty Guidelines (FPG) and may differ from state to state. Some states may set higher income limits or waive the asset guidelines altogether.

If you qualify for QMB but also meet the requirements for full Medicaid benefits, you are considered dual-eligible or QMB Plus. You will receive benefits from both the QMB program and your state Medicaid program. Having coverage through both programs may allow you to receive additional services not typically covered by Medicare, such as vision, hearing, and dental care.

You can apply for Medicare Savings Programs through your state. Even if you don't think you qualify, it is recommended that you still apply. In some cases, you may qualify for these programs even if your income or resources are higher than the federal limits listed.

Michigan Medicaid: A Horrible Insurance Trap?

You may want to see also

Explore related products

![]()

Specified Low-Income Medicare Beneficiary

The Specified Low-Income Medicare Beneficiary (SLMB) program is one of four Medicaid-administered Medicare Savings Programs (MSPs). The SLMB program helps low-income individuals with the cost of their Medicare premiums, deductibles, and co-insurance. To be eligible for the SLMB program, individuals must have income and assets below certain limits set by their state. Most states use general guidelines, but some may set higher income limits or waive asset limits.

The SLMB program covers the Medicare Part B premium, which is $185 per month for most people in 2025. This premium is for medical insurance and covers services such as doctor visits, outpatient care, and some preventive services. Additionally, individuals with SLMB status may also qualify for a program called SLMB Plus (or SLMB+). SLMB Plus provides benefits from both the SLMB program and the state Medicaid program, offering dual coverage that can include important health care services not covered by Medicare, such as vision, hearing, and dental care.

To determine eligibility for the SLMB program, individuals can contact their State Health Insurance Assistance Program (SHIP) or visit BenefitsCheckUp. These programs help individuals understand their options and provide assistance with the application process. It is important to note that each state has its own requirements and application process for Medicare Savings Programs, so it is recommended to consult the specific guidelines for one's state.

While the SLMB program helps with Medicare premiums, deductibles, and co-insurance, it is important to understand that individuals are still responsible for these costs to some extent. Additionally, the SLMB program does not provide coverage for all health care services, and there may be out-of-pocket expenses associated with certain treatments or services. Therefore, it is essential to carefully review the coverage provided by the SLMB program and consider other available options to ensure that one's health needs are adequately met.

The SLMB program is a valuable resource for low-income individuals, helping to make Medicare more accessible and affordable. By covering the Medicare Part B premium and offering the potential for dual coverage through SLMB Plus, the SLMB program can provide significant financial assistance for healthcare costs. However, it is important to stay informed about the specific benefits and limitations of the program in one's state to make informed decisions regarding healthcare coverage.

Rare Medical Conditions: Insurance Coverage and Access

You may want to see also

Explore related products

![]()

Special Enrollment Period

In Maryland, there are various Medicare health plans to choose from, including Original Medicare, Medicare Advantage Plans (Part C), Medicare Medical Savings Accounts (MSAs), and more.

A Special Enrollment Period is a period in which you can make changes to your Medicare Advantage and Medicare drug coverage when certain life events happen. These events include moving outside your plan's service area, losing Medicare or Medicaid eligibility, or joining a drug plan (under specific circumstances). You can also use the Special Enrollment Period to switch to a new Medicare Advantage Plan or Medicare drug plan. This period typically lasts for 2 months, during which you can make changes or switch plans without incurring a late enrollment penalty.

If you are in a Medicare Advantage Plan and move outside of your plan's service area, you will be automatically enrolled in Original Medicare when dropped from your previous plan. However, you can choose to switch to a new Medicare Advantage Plan or a Medicare drug plan during the Special Enrollment Period. If you notify your plan before moving, your chance to switch begins one month before the move and continues for two full months after.

In Maryland, there is an additional opportunity for a special enrollment period when filing taxes and checking a box on the state tax form. This special enrollment runs through the tax season.

How Long Do Accidents Affect Insurance Premiums?

You may want to see also

Frequently asked questions

The types of Medicare health plans available in Pasadena, MD, include Original Medicare, which covers Part A (Hospital Insurance) and Part B (Medical Insurance). There is also the Medicare Advantage Plan (Part C), offered by private companies that contract with Medicare. These plans often include drug coverage (Part D).

The Medicare Buy-In Program, also known as QMB (Qualified Medicare Beneficiary) and SLMB (Specified Low-Income Medicare Beneficiary), helps low-income individuals with the costs of Medicare coverage. QMB assists individuals with modest assets and combined incomes that do not exceed the federal poverty level. SLMB is for those with incomes between 100 and 120 percent of poverty and assists with Part B premiums.

You can apply for the Medicare Savings Program to receive financial assistance with your Medicare costs. Additionally, the state of Maryland offers the Specified Low-Income Medicare Beneficiary (SLMB) program to assist with Part B premiums for those who qualify.