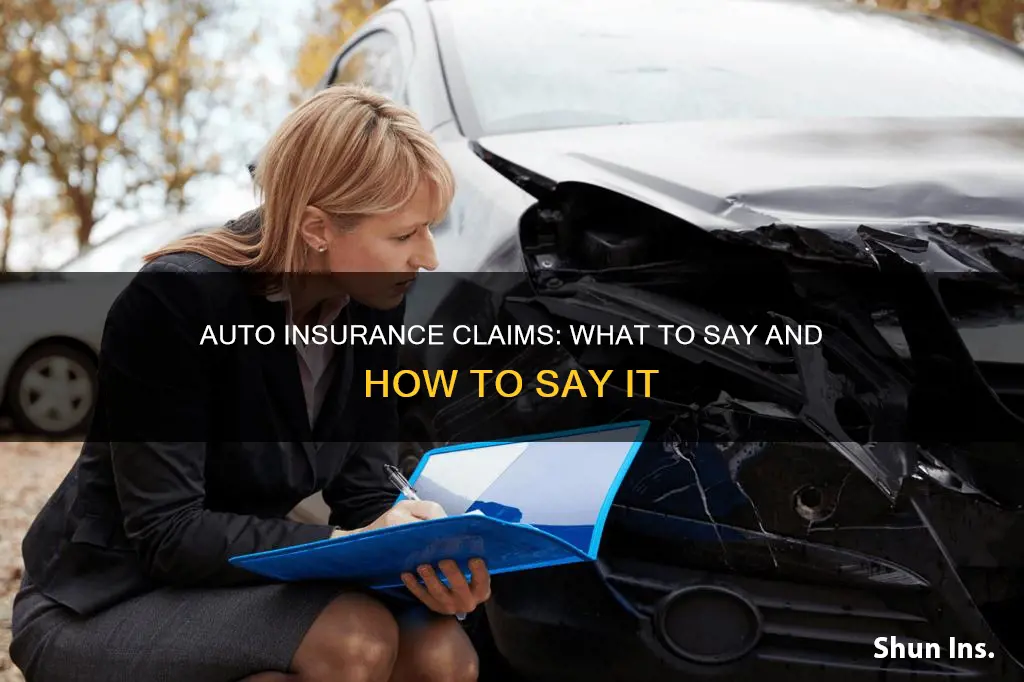

Filing an auto insurance claim can be a daunting task, especially if you've never done it before. The process can vary depending on your insurance provider, but it usually starts with a phone call, filling out an online form, or using your insurance company's mobile app. It's important to initiate the claim as soon as possible after a car accident and gather essential information, such as the details of the incident, the names and contact information of all involved parties, photos or videos of the damage, and a copy of the police report. Understanding your insurance policy is crucial, as different coverages may apply, such as liability, collision, or comprehensive insurance. You should also be aware of your deductible, as it will affect your out-of-pocket expenses. When speaking with insurance adjusters, it's best to provide brief and simple responses and avoid offering opinions or unnecessary details, as anything you say can potentially be used against you.

| Characteristics | Values |

|---|---|

| When to file a claim | When the accident involves significant damage or injuries, or involves theft or vandalism |

| What information is needed to file a claim | Details of the incident, information of all parties involved, photos or videos of the damage, copies of the police report, and insurance policy information |

| How to file a claim | Start the process via phone, mobile app, or online form, review your policy's coverage and deductibles, speak to an insurance adjuster, and arrange to have your vehicle repaired at an approved or preferred auto shop |

| Required documentation | Photos, videos, police report, receipts related to the incident (e.g. medical bills, auto repair, towing) |

| Following up on your claim | Ask for an estimated timeline and follow up if any delays occur |

Explore related products

What You'll Learn

![]()

Admitting fault

Understanding Admitting Fault

Consequences of Admitting Fault

When you admit fault, you accept full responsibility for any resulting damages, including property damage, medical bills, and other costs. Additionally, you may be held liable for any personal injuries suffered by the other driver, which could lead to a personal injury lawsuit. That's why it's crucial to understand the implications before admitting fault.

When to Admit Fault

If you are absolutely sure that you are at fault, it is best to admit it as soon as possible to avoid potential legal complications. However, it is recommended to consult a lawyer or legal representative before making any admissions.

What to Say When Admitting Fault

When speaking to the police or your insurance company, it is crucial to be honest and provide accurate information. Refrain from speculating or accepting fault if you are unsure. Provide details about the accident, such as the date, time, location, damage to your vehicle, skid marks on the road, and any injuries sustained. Remember to let the authorities determine fault based on the evidence, rather than admitting fault prematurely.

Exchanging Information

It is important to exchange names, phone numbers, and insurance information with the other driver. If there are witnesses, get their contact information as well. This will be helpful if further communication or legal proceedings are necessary.

Documenting Side Effects

Make sure to document any medical procedures and expenses resulting from the accident. These records can be crucial if a lawsuit arises from the incident.

Avoiding Common Mistakes

One common mistake people make is immediately admitting fault at the scene of the accident. It is advisable to take a few moments to assess the situation and ensure your safety. Contact a police officer to file a report and exchange information with the other driver, but refrain from admitting fault at this early stage.

In summary, admitting fault in an auto insurance claim can have significant consequences, and it's important to be honest and provide accurate information without speculating or oversharing. Consult a legal professional if needed and follow the guidelines provided by your insurance company to ensure a smooth claims process.

Insurance Notes: Vehicle Contingency Disclosure

You may want to see also

Explore related products

![]()

Giving opinions

When it comes to giving opinions during the process of filing an auto insurance claim, it is generally recommended to avoid doing so. Here are some reasons why:

Firstly, opinions about how an accident occurred are subjective, and it is best to stick to objective facts when speaking to an insurance company. The insurance company can use anything you say against you and will investigate the accident to determine how it occurred. Therefore, it is advisable to only share information backed by solid evidence and with the approval of your lawyer. If you don't know the answer to a question, it is best to say, "I don't know" instead of offering an opinion or guessing.

Secondly, insurance adjusters will often let you talk at length during phone calls, carefully listening for any information that can be used to shift blame or dispute liability. They may use any extra details you provide to reduce your chances of receiving maximum compensation for your injuries and related losses. Thus, it is in your best interest to keep your responses brief, simple, and focused on answering the specific questions asked without providing unnecessary additional information.

Additionally, insurance companies are in the business of protecting their profits and will look for ways to save money and close claims quickly and cheaply. Admitting any blame, even partial responsibility, can provide grounds for the insurer to deny your claim, make lowball settlement offers, or dispute liability for your damages. While honesty is important, you are not obligated to offer more information than is necessary or to admit liability.

In summary, when giving opinions during the process of filing an auto insurance claim, it is best to refrain from speculating and stick to the facts. Let the evidence speak for itself, and consult with your lawyer before sharing any information with the insurance company.

Nationwide Insurance: Gap Coverage Options

You may want to see also

Explore related products

![]()

Providing unnecessary details

When filing an auto insurance claim, it's important to be concise and only provide the necessary information. Here are some tips to avoid providing unnecessary details:

Only answer the questions asked

When speaking to an insurance adjuster, keep your responses brief and simple. Only answer the specific questions they ask and avoid providing additional information. Anything you say can be used against your case, so it's in your best interest to avoid long conversations and stick to the relevant details.

Avoid discussing irrelevant personal details

The insurance representative does not need to know every aspect of your life after the accident. Refrain from discussing information about your family, job, past accidents, or any other details that are not directly relevant to your accident injury claim.

Don't answer unasked questions

If the insurance adjuster doesn't inquire about certain details, such as your speed during a vehicle crash, there is no need to offer this information voluntarily. Only share information that is backed by solid evidence, and always consult your lawyer before sharing any details.

Avoid speculating or offering opinions

Insurance companies want to collect as much information as possible to potentially shift the blame to you. Refrain from offering opinions or speculations about how the accident occurred, as these are subjective and can be used against you. Let the insurance company investigate and determine the cause of the accident.

Be careful with recorded statements

Insurance companies may request a recorded statement, but you are not obligated to provide one. Recorded statements can be used to find inconsistencies and contradictions, which may be taken out of context and used against you. Consult a lawyer before agreeing to any recorded statements.

Remember, the goal is to provide factual and concise information relevant to the claim. Anything beyond that could potentially reduce your chances of receiving maximum compensation for your injuries and losses.

Understanding Loan Lease Coverage in Auto Insurance Policies

You may want to see also

Explore related products

![]()

Discussing substance use

When filing an auto insurance claim, it's important to be aware of the potential impact of substance use on the process. Here are some key considerations and suggestions for discussing substance use:

Understanding the Role of Substance Use

It is crucial to document all substance use or history, regardless of whether the claimant has a formal diagnosis of substance use disorder. As an insurance provider, understanding the role of substances in the claimant's life is essential. Ask questions about the reasons behind their substance use and its effects on their life. This includes exploring how substance use interacts with any symptoms or impairments they may have and its relevance to disability.

Phrasing Questions Sensitively

Avoid yes or no questions like "Do you use?" or "Have you ever used?". Instead, ask open-ended questions that encourage the claimant to share their experiences. For example, "What was going on in your life when you started using/drinking?" or "When you use, how does it affect your mental health symptoms? Does it make them better or worse?". Be mindful of phrasing questions in a non-judgmental way to build trust and encourage honest responses.

Using Person-First Language

When discussing substance use, adopt person-first language. This means referring to the claimant as a "person with a substance use disorder" rather than defining them by their disorder. This type of language emphasises that the person is not defined by their disorder and helps reduce stigma and negative bias.

Accuracy and Consistency in Terminology

Use consistent and clinically accurate terminology when discussing substance use. Refer to "substance use" to encompass all substances, including alcohol and drugs. Specify the severity of the substance use disorder (e.g., mild, moderate, severe) to provide a comprehensive understanding of the claimant's situation. Avoid stigmatising terms like "substance abuser" and instead opt for neutral phrases like "person in active use".

Addressing Denial and Fear

Recognise that denial is a common aspect of substance use disorders. The claimant may fear admitting their substance use due to concerns about losing benefits or facing legal repercussions. Create a safe and non-judgmental space for the claimant to share their experiences, assuring them that your role is to support their well-being and not to make a diagnosis.

Exploring Treatment and Sobriety

Ask questions about the claimant's experiences with treatment and sobriety. Inquire about their participation in treatment programs or self-help groups, such as Alcoholics Anonymous or Narcotics Anonymous. If they have been involved with the criminal justice system, they may have received treatment while in jail or on probation. Understanding their journey towards recovery can provide valuable context for their insurance claim.

Smart Savings: High Deductibles, Low Premiums

You may want to see also

Explore related products

![]()

Talking about injuries

When discussing injuries with an insurance company, it is important to be aware that anything you say can and will be used to assess your claim. Here are some key things to keep in mind:

- Do not say that you have no injuries or that you feel fine. Some injuries may take time to develop and be discovered. If you tell an insurance representative that you are uninjured, only to later discover that you have sustained bodily harm, you could jeopardize your recovery for those injuries.

- Do not provide any details about your care or how your injuries have impacted your life. The insurance company may already have insight into some of your injuries from a police report or information provided by another driver. The insurance representative will likely ask questions about the details of your injuries, such as treatment, providers, and missed work. Refrain from answering these questions and explain that you will provide the information once you have a better understanding of your injuries.

- Do not offer your opinion on how the accident occurred or what led to it. Opinions are subjective, and the insurance company can use anything you say against you. They will investigate and determine how the accident occurred. Only share information about the accident that is backed by solid evidence, and only if your lawyer approves. If you don't know the answer to a question, it is best to say, "I don't know."

- Do not share information about substance use. If you were injured in a traffic collision, do not volunteer information that confirms you consumed alcohol or any drugs, illegal or legal. The insurance company may blame you for the accident, and drunk driving is illegal. Even if you had a drink or two before the crash, the insurance company might deny your claim.

- Do not discuss your injuries with the insurance company. It may be tempting to downplay your injuries, but this gives the insurance carrier grounds to minimize the severity of your injuries and offer you less money. You need a doctor's examination, as some injuries do not immediately show symptoms. If you write off your pain too quickly, you risk not getting the compensation you need to pay for your medical expenses and other losses. You need to know the full scope of your injuries before sharing any information. When the time is right, your lawyer will share only the necessary records to prove your injuries.

- Do not provide a recorded statement about your injuries. You are not legally required to provide one, and insurance companies like recorded statements because they can comb through them for inconsistencies and contradictions. They can take your words out of context and use them against you.

- Do not provide access to your entire medical history. Insurance carriers may try to downplay a claimant's injuries by looking for pre-existing injuries or other events that explain symptoms and draw attention away from fresh injuries from an accident. They may need a copy of medical records directly related to the injuries sustained in the accident, but be cautious about signing any permission forms.

- Do not accept the first settlement offer. Many accident victims do not know their long-term prognosis, and some may not have discovered the full scope of their injuries. Insurance companies may offer an early settlement for far less than fair compensation, preying on claimants who struggle financially due to medical expenses and lost income. Once you accept a settlement offer, you must waive your right to future claims for the same event and injuries.

GAP Insurance: What It Covers

You may want to see also