Choosing the right medical insurance plan can be a complicated and confusing process. There are many different types of plans, such as HMO, EPO, PPO, and POS, and each offers different levels of coverage and provider flexibility. When selecting a plan, it is important to consider your specific healthcare needs, as well as the associated costs, such as monthly premiums, deductibles, and copays. Understanding the details of each plan and how they align with your requirements is crucial to making an informed decision. Additionally, it is worth noting that medical professionals and insurance companies frequently update their contracts, which can further impact your choice of plan and provider.

| Characteristics | Values |

|---|---|

| Type of plan | EPO, HMO, PPO, POS, Catastrophic, Bronze, Silver, Gold, Platinum |

| Cost | Premium, deductible, copay, coinsurance |

| Coverage | Doctor visits, hospital stays, medications, preventative care, dental, vision, mental health services |

| Provider choice | In-network, out-of-network |

| Income | Premium tax credit, cost-sharing reductions |

| Other | Health Savings Accounts (HSAs), Flexible Spending Accounts (FSAs) |

Explore related products

What You'll Learn

![]()

Health Maintenance Organization (HMO) plans

When choosing a health insurance plan, it is important to consider your personal situation, including your health, finances, and quality of life. Health Maintenance Organization (HMO) plans are a popular type of insurance provider that offers basic and supplemental health services to its subscribers through a network of contracted physicians and medical providers. HMOs are known for their lower out-of-pocket costs compared to other plans, but they also come with more restrictive conditions.

- HMO plans typically have lower premiums and out-of-pocket costs than other plan types, such as Preferred Provider Organization (PPO) plans.

- With an HMO plan, you must receive a referral from your designated primary care physician (PCP) within the HMO network to see a specialist.

- You are generally only covered if you receive care from doctors, hospitals, and other healthcare providers within the HMO network. However, some HMOs may offer Point-of-Service (HMOPOS) plans that allow for out-of-network services at a higher cost.

- HMOs provide coordinated and integrated care, focusing on prevention and wellness. The structured care standards ensure consistent quality across the HMO network.

- HMO plans may be subject to changes in contracts with medical providers. It is important to stay updated on any network changes to ensure your chosen doctors remain in-network.

When considering an HMO plan, it is essential to weigh the benefits and restrictions to determine if it aligns with your healthcare needs and preferences. Factors such as income, health status, and family dynamics should be taken into account when making your decision.

Florida Medicaid: Gym Membership Coverage Explained

You may want to see also

Explore related products

![]()

Employer-provided insurance

With employer-provided insurance, your employer will typically share the cost of your premium with you. The employer often pays most of the premium, and the employee pays the rest. Employers may offer a choice of group health plans to eligible workers. These include comprehensive benefit plans, which cover a large share of the hospital, physician, and prescription costs that a family might incur during a year; service-specific benefits, such as dental or vision care plans; and supplemental benefit plans, which may provide a limited additional benefit to enrollees if certain circumstances occur (e.g. $100 per day if hospitalized).

There are several benefits to employer-provided insurance. Firstly, it lowers your taxable income as employers deduct premium payments from your paycheck before taxes. Secondly, premium contributions from your employer are not subject to federal taxes, and your contributions can be made pre-tax. Thirdly, your employer does all the work of choosing the plan options, saving you time and effort.

However, there are also some potential drawbacks to consider. For example, if you have an offer of employer-provided insurance that is considered affordable (8.39% of household income in 2024) and provides minimum value, you will not qualify for financial help in the form of premium tax credits, but your family members may still qualify. Additionally, with employer-provided insurance, you are limited to the plans and options chosen by your employer, which may not fully meet your specific needs.

It is worth noting that large employers are subject to financial penalties under the ACA if they do not offer health insurance coverage that meets certain requirements to their full-time employees. This includes offering major-medical coverage and not a limited-benefit plan, and ensuring that coverage extends to dependent children.

Adding Dependents to Your Medical Insurance: A Step-by-Step Guide

You may want to see also

Explore related products

$10.39

![]()

Individual or family insurance plans

When choosing a health insurance plan, it is important to ensure that the plan meets your healthcare needs and budget. If you are married and/or have children, you should consider your family's healthcare needs and select a plan that works best for your circumstances. For instance, if you and your spouse have significantly different healthcare needs, you may benefit from separate plans with differing levels of coverage and pricing.

Individual health insurance plans are often categorized by the level of coverage they offer. On the Health Insurance Marketplace, plans are presented in "metal" categories: platinum, gold, silver, and bronze, with “catastrophic” plans also being available to some. The categories only differ in how you and your plan split the costs, not in the quality of care.

There are different types of Marketplace health insurance plans, and some plans restrict your provider choices or encourage you to get care from the plan's network of doctors, hospitals, pharmacies, and other medical service providers. Others pay a greater share of the costs for providers outside the plan's network. Depending on how many plans are offered in your area, you may find plans of all or any of the metal levels. Some common plan types include:

- Exclusive Provider Organization (EPO): A managed care plan where services are covered only if you use doctors, specialists, or hospitals in the plan’s network (except in an emergency).

- Health Maintenance Organization (HMO): A type of plan that usually limits coverage to care from doctors who work for or contract with the HMO.

- Preferred Provider Organization (PPO): A type of health plan that contracts with medical providers to create a network of participating providers. You pay less if you use providers that belong to the plan's network. You can use doctors, hospitals, and providers outside of the network for an additional cost.

- Point of Service (POS) plans: You pay less if you use doctors, hospitals, and other healthcare providers that belong to the plan's network. POS plans also require you to get a referral from your primary care doctor to see a specialist.

Health Savings Accounts (HSAs) and Flexible Spending Accounts (FSAs) allow you to set aside pre-tax dollars to pay for eligible healthcare expenses, such as copays, certain prescriptions, and some medical equipment. However, these plans are not available to everyone. HSAs require enrollment in a high-deductible health plan (HDHP) or catastrophic plan, and FSAs are only offered through employers and are not available in all companies.

Open Enrollment for Medical Insurance: When to Sign Up

You may want to see also

Explore related products

![]()

Government insurance programs

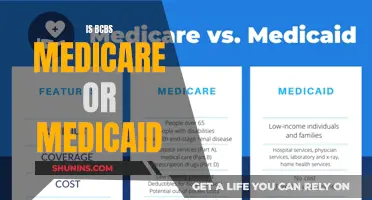

Medicare

Medicare is a federal government insurance program that provides health coverage for individuals aged 65 and older, as well as those who qualify due to a disability or specific illness. It includes the Traditional (Original) Fee-for-Service Program and Medicare health plans, such as Medicare Advantage. People with End-Stage Renal Disease (ESRD), requiring dialysis or a transplant, may also be covered by Medicare.

Medicaid and CHIP

Medicaid and the Children's Health Insurance Program (CHIP) are joint federal-state programs that provide health coverage for low-income individuals and families. Each state has its own eligibility rules and benefits package, and some states have unique names for their Medicaid programs. Medicaid and CHIP offer essential coverage to millions of Americans, ensuring access to healthcare for those who might otherwise be uninsured.

Federal Employees Health Benefits (FEHB) Plan

The FEHB Plan is a comprehensive health insurance program available to federal employees, retirees, and their survivors. It offers a wide selection of health plans, including Consumer-Driven and High Deductible plans, Preferred Provider Organizations (PPO), and Health Maintenance Organizations (HMO). The FEHB Program helps enrollees meet their healthcare needs by providing a range of options to suit different requirements and preferences.

TRICARE

TRICARE is a military healthcare system that provides coverage for uniformed service members, retirees, and their families. It is a vital component of the military healthcare network, ensuring that those who serve, as well as their loved ones, have access to necessary medical services. TRICARE includes VA Health Facilities as part of its network of providers.

When considering government insurance programs, it is important to review the specific details, eligibility requirements, and benefits offered by each program. These programs can provide valuable coverage for those who meet the criteria, ensuring access to healthcare services at affordable rates.

Teachers' Medical Insurance: What's Covered and What's Not

You may want to see also

Explore related products

![]()

Health Savings Accounts (HSAs) and Flexible Spending Accounts (FSAs)

HSAs are controlled by the individual and are more flexible. Contributions are made with pre-tax dollars and are associated with high-deductible health insurance plans. HSA participants can invest their balance and carry it over each year. However, if the money is not used for qualified health care expenses, the distribution is subject to taxation as ordinary income and a 20% penalty if the participant is under 65. HSAs must be paired with a high-deductible health plan, so they can become costly if you have significant medical expenses.

FSAs, on the other hand, are employer-owned and less flexible. Withdrawals are not allowed, and contributions cannot be rolled over to the next year. If you do not spend all the money in your FSA by the end of the year, you will lose your funds. FSAs have lower contribution limits and are only offered through employers, and not all companies offer them.

When choosing between an HSA and an FSA, it is important to carefully examine your options during open enrollment. Depending on your situation, a high-deductible health plan paired with an HSA might work well, or it might be too costly. It is also a good idea to confirm that these accounts cover the types of medical expenses you anticipate in the coming year.

Medical Insurance Reimbursement: Taxable or Tax-Exempt for Employees?

You may want to see also

Frequently asked questions

There are several types of health insurance plans, including HMO, EPO, PPO, and POS plans. These plans differ in the level of benefits they offer and the providers covered under the plan.

HMO stands for Health Maintenance Organization. It is a type of health insurance plan that offers complete coverage for medical services through a network of healthcare providers and facilities. You're generally only covered if you see doctors within the HMO network.

PPO stands for Preferred Provider Organization. With a PPO plan, you have the freedom to see any doctor or healthcare provider without a referral. However, you will pay less if you use providers that belong to the plan's network.

A deductible is the amount you pay before your insurance plan starts paying for your healthcare costs. For example, if you have a $1,000 deductible, you will need to pay the first $1,000 of covered healthcare expenses yourself. After you have paid the deductible, your plan will start covering your medical costs according to its terms.

There are several factors to consider when choosing a health insurance plan, including cost, coverage, provider network, and your specific healthcare needs. You should also review the benefits offered by the plan, such as coverage for doctor visits, hospital stays, medications, and preventive care. Additionally, consider your income, age, and the types of insurance coverage available to you.