Life insurance policies have a maturity date, or end date, which is expected to be after the insured person dies. This date is usually set at an age few people live beyond, such as 95 to 121 years old. When a life insurance policy matures, it owes the cash value or death benefit to the insured. The maturity of a life insurance policy is neither positive nor negative, but it is important to understand how it pertains to your financial plans.

| Characteristics | Values |

|---|---|

| Definition of maturity in life insurance | The maturity benefit is a lump-sum payment made by the insurance provider when the policy has reached its expiration date |

| Who receives the maturity benefit? | The maturity benefit is paid out to the policyholder if they survive beyond the maturity period of the policy. If the policyholder passes away before the maturity date, the benefit is paid to the beneficiary. |

| Types of life insurance policies | There are two main types of life insurance: term insurance and permanent insurance. Term insurance provides pure death benefit protection and does not build cash value, while permanent insurance builds up a tax-deferred cash value over time. |

| Maturity dates | Maturity dates vary depending on the type of policy and the age of the insured person. Term insurance has a set coverage period, often between 10 and 30 years, after which the policy matures or expires. Permanent insurance policies have a designated maturity date, typically after the insured person's death, and may be set at an advanced age such as 95, 105, 118, 121, or beyond. |

| Calculation of maturity benefit | The maturity benefit is equal to the amount of the fund value or the sum of premiums paid up to that time, along with any additional benefits chosen by the insurance company. In some cases, it may be equal to the cash value of the policy or the face amount. |

| Taxation | The maturity value paid out to the policy owner is subject to income tax. |

| Extension options | Some permanent life insurance policies offer maturity extension riders (MERs) that allow the policyholder to extend the maturity date until their death or their decision to terminate the policy. |

Explore related products

What You'll Learn

![]()

Maturity benefits and how to get them

Maturity benefits are the amount you receive from your insurance provider when your policy reaches its term. This is typically paid out as a lump sum, but some plans enable periodical maturity distributions depending on instalments. The maturity amount comprises the premiums paid up to that point plus any additional benefits.

Term insurance provides pure death benefit protection and does not build cash value. It does not have a maturity date, and there are no maturity advantages. Whole life insurance policies, also known as permanent life insurance, provide coverage for the remainder of your life. Permanent life insurance policies have a designated maturity date, or the expected end date of a permanent life insurance policy. This estimation is determined after evaluating the commissioners' standard ordinary (CSO) mortality table, which is used by life insurers to predict the mortality of a given demographic. The maturity date of a permanent life insurance policy is usually set at an age few people live beyond, such as 99 or 121 years old.

To receive maturity benefits, you must have paid all your premiums and finished the term. If you have a permanent life insurance policy, you can purchase a maturity date extension rider (MER) to keep your policy in force beyond the maturity date. To do this, you will need to know your original maturity date and any associated deadlines for electing an MER.

COPD and Life Insurance: Does Old American Approve?

You may want to see also

Explore related products

![]()

Permanent life insurance and maturity dates

Permanent life insurance, also known as whole life insurance, provides coverage for the remainder of the insured person's life. Unlike term life insurance, which provides coverage for a set period, permanent life insurance policies have a designated maturity date, or the expected end date of the policy. This date is determined after evaluating the commissioners' standard ordinary (CSO) mortality table, which is used by life insurers to predict the mortality of a given demographic.

The maturity date of a permanent life insurance policy is based on the age of the insured person and varies depending on when the policy was issued. For example, a policy issued using the 2017 CSO tables could mature when the insured person reaches 121—an age few people live beyond. However, if the policy was issued using the 1980 CSO tables, the maturity date might be when the insured person turns 99. This could be an issue for a policyholder approaching their 100th birthday.

When a permanent life insurance policy matures, the "maturity value" of the policy is paid out to the policy owner, and coverage ends. The maturity value may be equal to the cash value of the policy or the face amount. It is important to note that a portion of the cash value paid out is taxable to the policy owner. This can be a problem, as the maturity value may be a very large amount, and beneficiaries may be left with less or no inheritance.

To address this issue, some permanent life insurance policies offer the option to purchase a maturity date extension rider (MER) before the end of the policy. This type of policy rider allows the policyholder to extend the maturity date until their death or until they choose to terminate the policy. To purchase an MER, the policyholder needs to know their original maturity date and any associated deadlines for electing the MER. It is recommended to speak with a life insurance agent to understand the specific details of a policy and the options available for extension riders.

Final Expense Insurance: A Life Insurance Variant?

You may want to see also

Explore related products

![]()

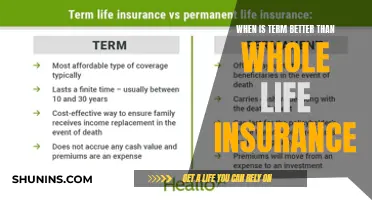

Term life insurance and maturity

Term life insurance is a type of insurance that provides coverage for a specific period of time, typically between 10 and 30 years. It is designed to offer financial protection to beneficiaries in the event of the policyholder's death during the specified term. This type of insurance is often chosen by individuals who want to ensure their loved ones are taken care of during a particular phase of their lives, such as when they have young children or dependents.

Unlike permanent life insurance, term life insurance does not build cash value over time and typically does not have a maturity date. When a term life insurance policy reaches the end of its term, it simply expires, and coverage ceases. However, there are a few scenarios in which a term life insurance policy can be considered to have "matured."

One scenario is when the policyholder passes away during the term of the policy. In this case, the insurance policy has served its purpose, and the beneficiaries will receive the full death benefit. This can be considered a form of maturity, as the policy has fulfilled its intended function.

Another scenario is when the term of the policy expires. At this point, the policyholder has the option to renew the policy, convert it to a permanent policy, or let it terminate. If the policy is not renewed or converted, it will simply end, and there will be no further coverage or benefits. While this may not be a traditional form of "maturity," it signifies the end of the policy's active period.

It is important to note that some term life insurance policies offer a return of premium feature, where the insurance company returns all or a portion of the premiums paid if no death benefit has been claimed. This feature can provide a financial benefit to the policyholder upon the policy's expiration, similar to a maturity payout. However, it is not considered true maturity, as the policy itself does not build cash value.

In summary, while term life insurance policies do not have traditional maturity dates like permanent policies, they can be considered to have "matured" in certain situations, such as the policyholder's death or the expiration of the policy term. Additionally, features like a return of premium can provide a financial benefit similar to maturity payouts in some term life insurance policies.

Whole Life Insurance: Free but Worth the Cost?

You may want to see also

Explore related products

![]()

Universal life insurance and maturity

Universal life insurance is a form of permanent life insurance that can provide coverage for the entirety of the policyholder's life. It is similar to whole life insurance but offers more flexibility in terms of premium payments and death benefits. Universal life insurance policies can also accrue cash value, which can be used to pay premiums or increase the death benefit. This cash value grows tax-deferred over the lifetime of the policy.

While universal life insurance policies can last a lifetime, they do have a maturity date, typically set at an advanced age such as 95, 100, 105, 118, 120, or 121. This maturity date acts as a kind of "expiration date" for the policy. If the policyholder outlives the maturity date, they may receive a lump-sum payment equal to the cash value of the policy. However, if the policyholder passes away before the maturity date, their beneficiaries will receive the death benefit, which may include any remaining cash value.

The flexibility of universal life insurance policies allows policyholders to adjust their premium payments, which can be beneficial for those with fluctuating incomes. Additionally, policyholders can choose to pay more upfront to build a larger cash value, which they can borrow against or use to increase the death benefit. This flexibility, however, requires a more hands-on approach to managing the policy, as the cash value and premium payments need to be monitored to ensure the policy remains in effect.

There are different types of universal life insurance policies, including variable universal life insurance and indexed universal life insurance. Variable universal life insurance allows policyholders to tie their cash value gains directly to the market, offering the potential for higher returns but also higher risk. Indexed universal life insurance ties the cash value to the performance of stock indexes, and the cash value may be placed in a fixed account unless other investments are specified. It is important to carefully consider the different types of policies and their provisions, as well as consult with a financial advisor or insurance agent, to find the plan that best suits one's needs and risk tolerance.

Primerica Life Insurance: Steps to Becoming an Agent

You may want to see also

Explore related products

![]()

Maturity extension riders (MERs)

The maturity date of a permanent life insurance policy is the expected end date of the policy and is typically set at an age few people live beyond, such as 95 or 121 years. When a permanent life insurance policy matures, the coverage terminates, and the maturity value, or the cash value that has accumulated over the life of the policy, is paid out to the policyowner. If the policyowner is still alive when the maturity date arrives, they will receive this payout, which is subject to income tax.

MERs can be purchased to delay the policy's maturity date, providing coverage for the policyholder even after they reach the original maturity date. There are a few different ways that MERs can work. Some riders simply extend the maturity date by a set number of years, while others allow the policyholder to choose when they want the policy to mature. The cost of an MER will vary depending on the type of rider and the insurance company, and it is important to factor this additional cost into the overall policy cost when comparing different options. MERs are typically terminable, meaning that the policyholder can cancel the rider at any time.

It is important to note that MERs may need to be elected years in advance of the original maturity date, and the specific terms and conditions of MERs can vary depending on the insurance company. To make an informed decision about purchasing an MER, it is recommended to speak with a life insurance agent or financial advisor to understand the options available and how they can be tailored to your needs.

Life Insurance: Exploring Unique Characteristics and Features

You may want to see also

Frequently asked questions

Life insurance maturity refers to the termination of a life insurance policy, at which point the coverage ends and the maturity value is paid out to the policy owner.

The maturity value is the amount paid out to the policy owner when a life insurance policy matures. It could be equal to the face amount, the cash value of the policy, or the sum of the premiums paid up to that time.

Term life insurance policies only provide coverage for a set period, after which they mature and terminate. If the policyholder is still alive, they may receive a payout, but all benefits will end. Whole life insurance policies, on the other hand, do not have a set maturity date and are designed to last until the death of the insured.