Life insurance with a cash value component is a type of permanent policy that can build funds over time. This type of policy can be appealing as it allows you to access the money early by taking out a loan against the policy, surrendering the policy, or making a withdrawal. The cash value in permanent life insurance policies can generate impressive returns, but it also comes with risks. There are several types of life insurance that can build cash value, including whole, universal, variable, and indexed life insurance. The cash value growth depends on the type of policy and market conditions.

| Characteristics | Values |

|---|---|

| Types | Whole, Universal, Variable, and Indexed |

| Coverage | Life-long |

| Premium | Depends on age at the time of purchase; remains the same over time |

| Cash Value | Grows based on a fixed interest rate set each year in the policy by the company |

| Accessing Cash Value | Withdrawals, loans, or by cancelling the policy |

| Risk | Low for whole life insurance; higher for variable life insurance |

Explore related products

What You'll Learn

![]()

Whole life insurance

When you pay your premium, one portion of that payment goes toward the policy's death benefit, another portion is channeled toward the insurer's costs and profits, and the third increases the policy's cash value. This cash value amount can increase over the life of the policy and can be accessed by the policyholder while they are living. You can withdraw money from the cash value to cover expenses or take out a loan against the policy. However, withdrawing money or taking out a loan will decrease the cash value of your whole life insurance policy.

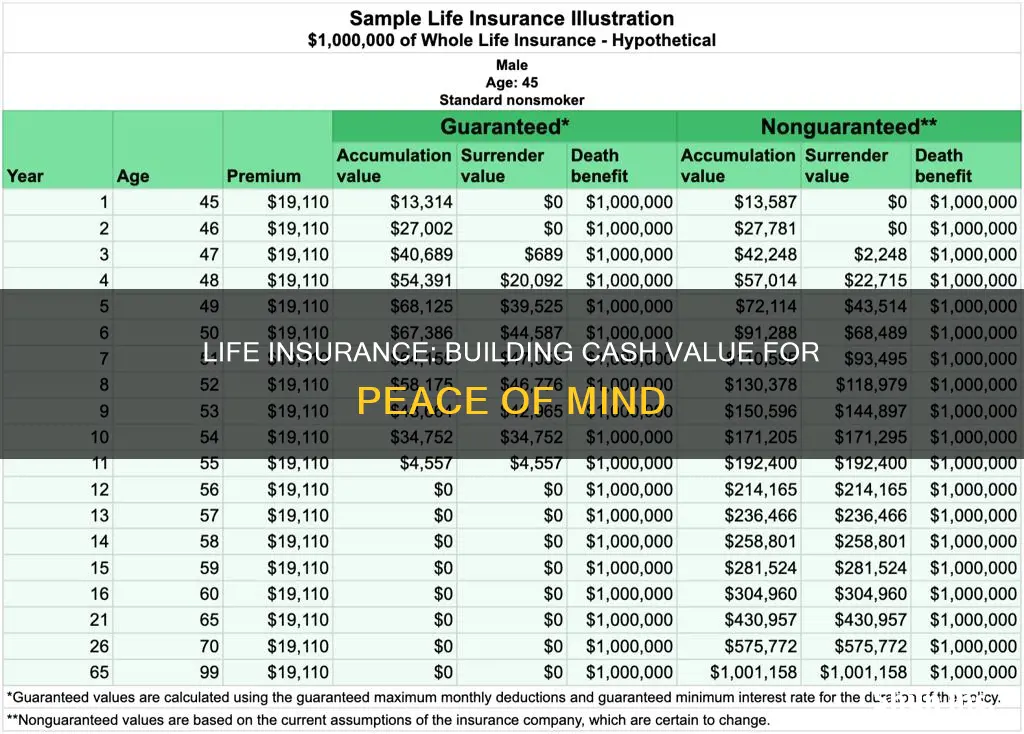

If you are considering a whole life insurance policy, it is important to understand its costs, benefits, and potential for long-term growth. You can request a policy illustration, which will include a whole life cash value chart, to help you make an informed decision.

Life Insurance Agent: Steps to Start and Succeed

You may want to see also

Explore related products

$14.99 $14.95

![]()

Universal life insurance

One of the key benefits of universal life insurance is its flexibility. It allows you to raise or lower your premiums within certain limits, and it can be cheaper than whole life coverage. However, if your investments underperform or you underpay for too long, it could affect your death benefit or cause your policy to lapse. The cash value earns an interest rate set by the insurer, and it can change frequently, although there is usually a minimum rate that the policy can earn.

Another advantage of universal life insurance is the ability to borrow against or cash in your savings portion, which grows over your lifetime. You can take out a loan against the accumulated cash value without tax implications, and the interest rates on these loans are often lower than rates available for a personal loan. However, unpaid loans will reduce the death benefit by the outstanding amount.

When deciding whether universal life insurance is right for you, it's important to consider your long-term coverage needs and whether you want a policy with a cash value component. Universal life insurance can be a good option for those who want to build wealth and have the ability to withdraw or borrow from their policy. However, it's important to carefully manage your account to ensure that your policy remains in force.

Beneficiaries: Multiple People, One Life Insurance Policy

You may want to see also

Explore related products

![]()

Variable life insurance

However, there are also some downsides to variable life insurance. The fees and expenses associated with the policy may be significant, and it tends to cost more than other permanent life insurance policies. The cash value component of variable life insurance is invested in assets like mutual funds, so it may rise or fall in value. Therefore, these policies carry more risk compared to other life insurance policies. If your investments underperform, your cash value can decrease, leaving you with less wealth to tap into.

Life Insurance Post-Stroke: Is It Possible?

You may want to see also

Explore related products

![]()

Permanent life insurance

There are several types of permanent life insurance policies, including whole life, universal life, and variable life. Whole life insurance provides coverage for the entire life of the policyholder, with fixed premiums that do not change with age or health status. Universal life insurance offers more flexibility, as premium payments can be adjusted over time. Variable universal life insurance provides even more flexibility, as the cash value can be invested in sub-accounts tied to the market, allowing for the potential for greater growth but also the risk of decline.

Life Insurance Simplified: Understanding AAA Ratings

You may want to see also

Explore related products

![]()

Death benefits

The death benefit is the primary reason for purchasing life insurance and is the amount of money paid to the beneficiary (the person chosen to receive the money) when the policyholder dies. When you buy a life insurance policy, you can select a death benefit and name a beneficiary who will receive the payout. For example, if you buy a life insurance policy with a $100,000 death benefit and pass away, the insurance company will pay $100,000 to the person you named as your beneficiary. This money can be used to cover living expenses, education, retirement savings, or even a vacation. It is usually tax-free, but it is recommended to consult with a tax advisor.

There are no stipulations or conditions on benefit payouts. The beneficiary can receive the death benefit as a lump sum or in smaller amounts over time, depending on their preference and the insurance company's offerings. If the beneficiary is revocable, it is relatively easy to change their share without their consent. However, if the beneficiary is irrevocable, it can be challenging to remove them from the policy or change their share without their consent.

The death benefit can be reduced in certain situations. For example, if the policyholder willfully misrepresented their information during the application process to obtain lower premiums, the insurance company may reduce the benefit amount or cancel coverage. Additionally, if there are outstanding loans against the cash value of the policy, the death benefit may be reduced. If the policy has an adjustable death benefit, the payout may be lower than the original coverage amount.

It is important to note that the death benefit is separate from the cash value component of a life insurance policy. The death benefit is typically paid out of the premiums, while the cash value component is an investment that grows over time and can be accessed early by the policyholder through loans, withdrawals, or surrendering the policy.

Life Insurance and SSI Disability: How Does OPM Affect You?

You may want to see also

Frequently asked questions

Life insurance with cash value is a type of permanent policy that can build funds over time through the cash value component. The two main components that make up a life insurance policy are the death benefit and the cash value.

Cash value accumulates in your permanent life insurance policy because your premiums are split into three categories. One portion of your premium goes toward the death benefit, another goes toward the insurer's costs and profits, and the third contributes to the policy's cash value.

Whole life insurance, universal life insurance, and variable life insurance are types of life insurance that can build cash value. Term life insurance, on the other hand, is for a set period of time and does not build cash value.

With whole life insurance, the cash value grows at a fixed rate. With universal life insurance, the cash value is invested and the growth rate depends on how well those investments perform.

You can typically access the cash value in your life insurance policy before it ends by taking out a loan, making a withdrawal, or surrendering the policy. However, doing so may reduce your death benefit.