Life insurance is a complex and varied topic, with many options available to consumers. It is important to understand the different types of policies and their respective features to make an informed decision. One of the key considerations when choosing a life insurance policy is whether to opt for term insurance or cash-value insurance. Term insurance provides the most protection for your money and is generally the most affordable option, while cash-value insurance, which includes whole life and universal life policies, offers permanent coverage and a savings component. This savings component, or cash value, allows policyholders to accumulate funds for future use, such as borrowing or withdrawing cash, or paying policy premiums. Understanding the valuation of life insurance policies is, therefore, a critical aspect of financial planning, and consumers should carefully consider their options to ensure they choose the most appropriate policy for their needs.

| Characteristics | Values |

|---|---|

| Purpose | Accumulate funds for future use |

| Cash Value | A portion of each premium is deposited into an interest-bearing savings account |

| Tax | Tax-free |

| Use | Borrowing, withdrawing, or paying policy premiums |

| Comparison with Term Life Insurance | More expensive, no expiry after a specific number of years |

| Premium | Higher than term life insurance |

| Risk | Decreases as cash value increases |

| Death Benefit | Full amount paid upon death, regardless of cash withdrawals |

| Settlement Options | Lump sum, interest income, income for a specific period, income for life, or income for a specific amount |

| Valuation Manual | Adopted by the commissioner, substantially similar to the one approved by the National Association of Insurance Commissioners |

Explore related products

$83.53 $93

What You'll Learn

![]()

Cash value life insurance

A portion of each premium payment made is deposited into an interest-bearing savings account, allowing the policyholder to accumulate funds for future use. This cash value grows tax-free over the lifetime of the deposit, and the policyholder can use the cash value for several purposes, including borrowing or withdrawing cash from it, or using it to pay policy premiums.

The cash value of a universal life insurance policy, for example, can be used to pay for premiums or other expenses as needed. This type of insurance also allows the policyholder to change the value of premium payments, providing more adjustability in different life stages.

The cash value insurance feature is designed to benefit the policyholder while they are still alive, by providing a loan option and a way to potentially decrease premium payments. However, it is important to note that using the cash value may result in changes to the death benefit amount or even the termination of the policy. For example, if the policyholder borrows the full cash value, it may result in the coverage being terminated, and the death benefit will not be paid upon their passing.

Overall, cash value life insurance provides policyholders with an additional financial asset and financial flexibility, allowing them to leverage funds for loans, major expenses, and more.

Life Insurance: When It's Not Worth the Cost and Commitment

You may want to see also

Explore related products

$73.91

![]()

Adjustable life policies

Adjustable life insurance, also known as universal life insurance, is a type of permanent life insurance that offers flexibility to the policyholder. It is a hybrid policy between term life and whole life insurance. Term life insurance pays a death benefit if death occurs within a certain number of years, whereas whole life insurance pays a death benefit regardless of when death occurs.

Adjustable life insurance offers the policyholder the ability to adjust the benefits on the insurance policy depending on their current financial situation. This flexibility means that the policyholder can increase or decrease the premium, change the premium-paying period, increase or decrease the face amount of coverage, or change the period of protection. The premium is the amount that the policyholders pay for the insurance product, and the death benefit is the amount the policyholder's beneficiaries will receive when the policyholder dies.

The distinguishing feature of adjustable life policies is the inclusion of an interest-bearing savings component, the "cash value" account, which the policyholder can tap into while alive. The cash value of the policy can be increased by raising premium payments or decreased by withdrawing funds as a loan with interest. The cash value grows tax-free over the lifetime of the deposit, and the policyholder can borrow against it, use it to pay premiums, or withdraw cash from it. However, if the policy's cash value drops too low to cover the cost of the insurance, the insurer may raise premiums or the policy may lapse.

The flexibility of adjustable life insurance means that it usually comes with a higher price. The policyholder must pay higher premiums due to the cash value attached to the policy. Additionally, the policy may be affected by the investment portfolio it is a part of; if the investment portfolio does not perform well, the interest rate on the cash value will be significantly lower.

Understanding the Duration of Servicemen's Group Life Insurance

You may want to see also

Explore related products

![]()

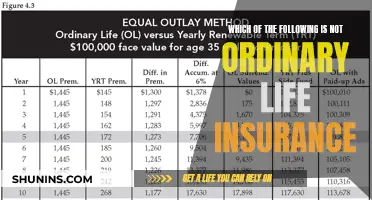

Term insurance

The valuation of term insurance policies can be complex and depends on various factors. One method used for valuation is the Interpolated Terminal Reserve (ITR) method, which calculates the value based on the policy's reserve value at a particular point in time. However, ITR may not always be an appropriate or accurate measure, and other methods, such as the income and market approaches, may be considered for a fair market valuation.

It is important to note that term insurance policies do not have a cash value component, which means they are generally more affordable than permanent life insurance policies. However, this also means that term insurance policies do not provide the same opportunities for accumulating funds or borrowing against the policy as permanent life insurance policies with a cash value component.

Who Collects Airforce Life Insurance: Daughter or Son?

You may want to see also

Explore related products

![]()

Death benefits

Life insurance acts as a financial safety net for your family. If the policyholder dies while the policy is active, the insurance company pays a sum of money, known as the death benefit, to the beneficiaries named in the policy. This money can help replace lost income and cover essential expenses, such as housing, food, and utility bills, ensuring that the policyholder's loved ones can maintain their lifestyle. It can also be used to pay for funeral expenses, cover outstanding debts, or be donated to charitable organisations.

The death benefit can be a significant source of financial support for the beneficiaries, especially if the deceased was the primary breadwinner. It can help them manage their immediate financial needs and provide long-term financial stability. In some cases, the death benefit can also be used to implement wealth transfer strategies, making it a versatile tool for those with complex financial planning or health-related situations.

The amount of the death benefit can vary depending on the type of life insurance policy chosen. Some policies offer a level death benefit, which remains the same throughout the policy's duration, while others provide an adjustable death benefit that can be increased or decreased based on certain conditions. For example, in a Universal Life Policy, the death benefit adjusts periodically and is written for a specific period. On the other hand, a Straight Life policy provides a level, guaranteed death benefit that remains unchanged.

When considering life insurance, it is essential to evaluate the different policy features and choose one that meets your specific needs. Some policies offer additional features, such as accelerated death benefits, a waiver of premium, or flexible premium payments. The chronic illness rider, for instance, allows access to a portion of the death benefit if the policyholder is diagnosed with a chronic illness requiring long-term care. These additional features often come at an extra cost, so it is important to weigh the benefits against the added expense.

Ultimately, the death benefit is a crucial aspect of life insurance, providing financial security and peace of mind for both the policyholder and their beneficiaries. By selecting an appropriate policy, individuals can ensure that their loved ones are taken care of in the event of their death, helping to cover expenses and maintain their standard of living.

Life Insurance Tax in New York: What You Need to Know

You may want to see also

Explore related products

$71.18 $90

$88.99 $131

![]()

Insurance valuation manuals

An insurance valuation manual would provide guidance on the various types of insurance policies, their features, and the options available to policyholders. For example, a manual might explain the difference between term life insurance and permanent life insurance, and how each type is valued.

Term life insurance policies, such as annually renewable term, level term, and decreasing term, provide coverage for a specific period and do not accumulate cash value. The premiums for these policies may increase or remain constant, but they eventually expire. On the other hand, permanent life insurance policies, including whole life and universal life, offer lifelong coverage and have a cash value component. This means that a portion of the premiums is allocated to a savings account that earns interest over time. This cash value can be borrowed against, withdrawn, or used to pay premiums, providing flexibility to the policyholder.

An insurance valuation manual would also outline the factors that influence the valuation of insurance policies. For instance, the manual would explain how the death benefit, or the amount paid out upon the insured's death, is determined and how it can be increased or decreased. It would clarify that providing evidence of insurability, such as proof of good health, may be required to increase the death benefit. Additionally, the manual would describe the impact of premium payments on the policy's valuation. For example, adjustable life policies allow policyholders to increase or decrease their premiums, affecting the overall value of the policy over time.

Furthermore, the manual would delve into the intricacies of cash value accumulation and its implications for valuation. It would explain that the cash value component of permanent life insurance policies grows tax-free and can be accessed during the insured's lifetime. However, withdrawals from the cash value account may result in a reduction of the death benefit. The manual would also highlight how the insurance company's risk decreases as the cash value increases, as the accumulated cash value offsets the insurer's liability.

Additionally, an insurance valuation manual might provide illustrative examples and calculations to demonstrate the valuation process. These examples could include scenarios with different policy types, premium payment frequencies, and cash value growth rates to showcase the dynamic nature of insurance valuation. By offering practical applications, the manual would enhance the understanding of insurance valuation for users.

Life Insurance and Suicide: Understanding the Payout

You may want to see also

Frequently asked questions

Cash value life insurance is a form of permanent life insurance that features a cash value savings component. The policyholder can use the cash value for various purposes, including borrowing or withdrawing cash from it, or using it to pay policy premiums.

A portion of each premium payment is allocated to the cost of insurance, and the remainder is deposited into a cash value account. The cash value of life insurance earns interest, and taxes are deferred on the accumulated earnings. As the cash value increases, the insurance company's risk decreases as the accumulated cash value offsets part of the insurer's liability.

There are many types of life insurance policies, including term insurance, cash value policy, whole life, convertible term, universal life, and guaranteed renewable. Consumer educators recommend that most buyers choose term insurance to afford adequate coverage.