The Federal Deposit Insurance Corporation (FDIC) is an independent federal government agency that insures deposits in commercial banks and thrifts. The FDIC was created by Congress to maintain stability and public confidence in the nation's financial system. It provides deposit insurance to protect individuals' money in the event of a bank failure. Deposit insurance is the government's guarantee that an account holder's money at an insured bank is safe up to a certain amount, typically $250,000 per account. This insurance is provided automatically when an individual opens an account at an FDIC-insured bank.

| Characteristics | Values |

|---|---|

| Name of the program | Federal Deposit Insurance Corporation (FDIC) |

| Year of establishment | 1933 |

| Purpose | To protect bank depositors and boost confidence in the U.S. financial system |

| Coverage | $250,000 per depositor, per ownership category, and per FDIC-insured bank |

| Funding sources | Insurance premiums paid by banks and interest earned on U.S. government obligations |

| Management | Five-member board, including the Chairman of the FDIC, the Comptroller of the Currency, the Director of the Office of Thrift Supervision, and two public members appointed by the President and confirmed by the Senate |

| Deposit Insurance Funds | Bank Insurance Fund (BIF) and Savings Association Insurance Fund (SAIF) |

| Bank failures | The FDIC either sells the bank or pays off insured deposits and liquidates the bank's assets |

Explore related products

![Federal Deposit Insurance Act: [As Amended Through P.L. 117–263, Enacted December 23, 2022]](https://m.media-amazon.com/images/I/517mroyL3UL._AC_UY218_.jpg)

What You'll Learn

![]()

The Federal Deposit Insurance Corporation (FDIC)

The FDIC manages two deposit insurance funds: the Bank Insurance Fund (BIF) and the Savings Association Insurance Fund (SAIF). The BIF insures deposits in commercial banks and savings banks, while the SAIF covers deposits in savings and loan institutions. Insured banks pay for deposit insurance through premium assessments on their domestic deposits. The FDIC receives no taxpayer money or appropriations from Congress; instead, it is funded by insurance premiums paid by banks and interest earned on its investments in U.S. government obligations.

The FDIC has a five-member board, including the Chairman of the FDIC, the Comptroller of the Currency, the Director of the Office of Thrift Supervision, and two public members appointed by the President and confirmed by the Senate. The FDIC has the authority to regulate and supervise state non-member banks, and it can revoke a bank's deposit insurance, effectively forcing its closure. When a bank fails, the FDIC can sell the bank to a willing buyer or pay off insured deposits and liquidate the bank's assets. The FDIC also offers open bank assistance, arranging for the purchase or recapitalization of an institution before it fails, protecting even uninsured depositors.

The FDIC provides resources for bankers, including guidance on regulations, information on examinations, and training programs. It also educates and protects consumers, promoting economic inclusion and connecting people with financial resources in their communities. The FDIC publishes documents in the Federal Register and, as of 2025, launched a Mission-Driven Bank Fund to support insured Minority Depository Institutions (MDIs) and Community Development Financial Institutions (CDFIs).

Arvest Bank Accounts: Are They Insured?

You may want to see also

Explore related products

![]()

Deposit insurance funds

The Federal Deposit Insurance Corporation (FDIC) manages the Deposit Insurance Fund (DIF) to ensure that deposits at member banks are protected. The FDIC was founded in 1933, and since then, no depositor has lost any FDIC-insured funds. The FDIC helps maintain stability and public confidence in the US financial system by insuring deposits of up to $250,000 per depositor, per ownership category, at each FDIC-insured bank. The FDIC also helps fund resolution activities when banks fail.

The DIF is backed by the full faith and credit of the US government and has two sources of funding: assessments (insurance premiums) paid by FDIC-insured institutions, and interest earned on funds invested in US government obligations. The FDIC buys Treasury notes, and the interest on these notes helps the DIF grow. The FDIC does not receive any taxpayer money or appropriations from Congress. Instead, the agency is funded by insurance premiums paid by banks and interest earned on the DIF, which is invested in US government obligations. The banks' premiums depend on the size of the bank and bank regulators' assessment of the riskiness of the bank.

The FDIC manages two deposit insurance funds: the Bank Insurance Fund (BIF) and the Savings Association Insurance Fund (SAIF). The BIF insures deposits in commercial banks and savings banks up to a maximum of $100,000 per account. Insured banks pay for deposit insurance through premium assessments on their domestic deposits. Foreign deposits are not insured and are thus not subject to deposit insurance premiums.

The FDIC has a five-member board, including the Chairman of the FDIC, the Comptroller of the Currency, the Director of the Office of Thrift Supervision, and two public members appointed by the President and confirmed by the Senate. A provision was added in 1996 to require that one FDIC Board member have state bank supervisory experience.

Public and Private Insurance: The US Dual System

You may want to see also

Explore related products

$37.99

![]()

Deposit insurance coverage

FDIC deposit insurance covers up to $250,000 per depositor, per FDIC-insured bank, for each account ownership category. Ownership categories include individual accounts, joint accounts, and accounts held by corporations, partnerships, limited liability companies (LLCs), for-profit unincorporated associations, and not-for-profit organizations. Each ownership category is treated independently, so a person with accounts in multiple ownership categories at the same bank may qualify for more than $250,000 in FDIC insurance coverage.

The FDIC maintains the Deposit Insurance Fund (DIF), which is backed by the full faith and credit of the United States government. The DIF is funded by insurance premiums paid by FDIC-insured institutions and interest earned on investments in U.S. government obligations. The FDIC uses the DIF to insure deposits and protect depositors of FDIC-insured banks in the event of bank failure. Since the FDIC was founded in 1933, no depositor has lost money in an FDIC-insured account due to a bank failure.

The FDIC provides resources to help depositors understand their deposit insurance coverage, including an online Electronic Deposit Insurance Estimator (EDIE) that can calculate how much of an individual's funds are covered by deposit insurance. The FDIC also provides a phone number (1-877-275-3342) that individuals can call to determine their deposit insurance coverage or ask specific questions about deposit insurance.

Exploring Private Insurance Bans Around the Globe

You may want to see also

Explore related products

![]()

Deposit insurance exemptions

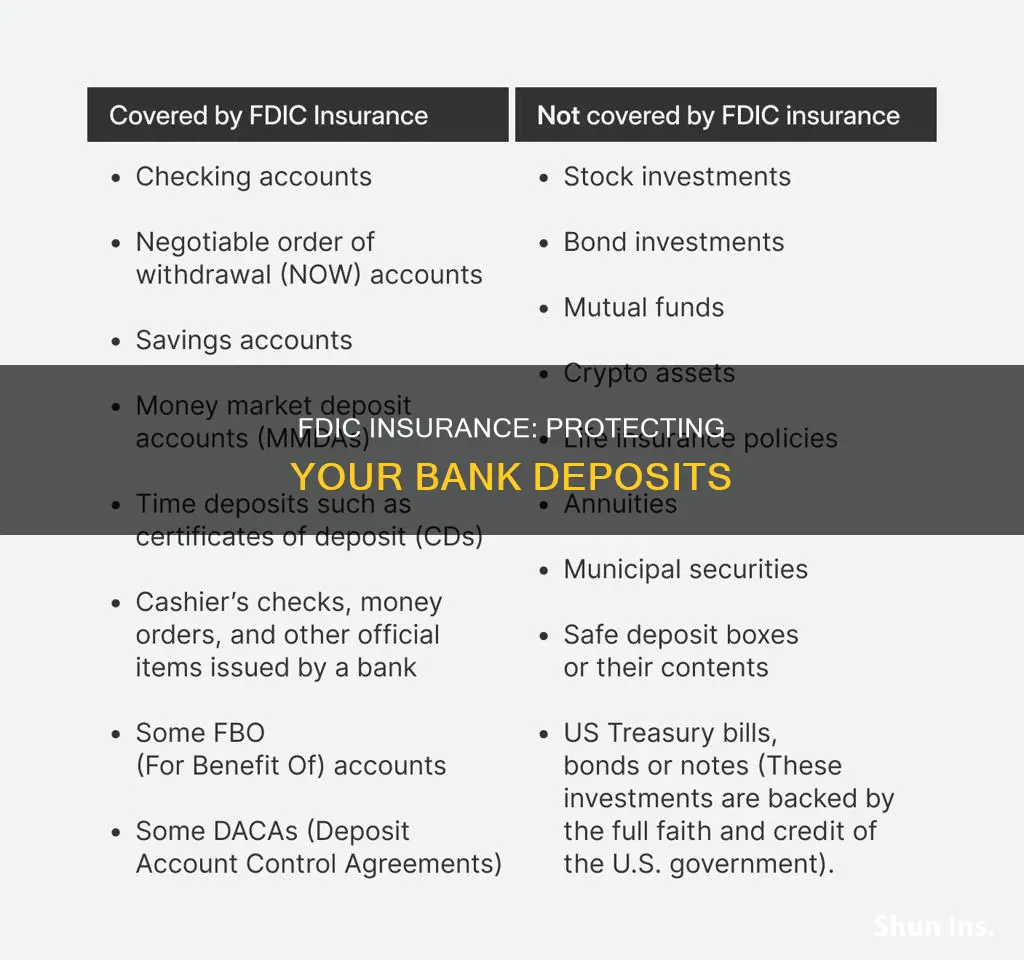

The Federal Deposit Insurance Corporation (FDIC) is an independent federal government agency that insures deposits in commercial banks and thrifts. FDIC deposit insurance covers deposits in all types of accounts at FDIC-insured banks, but it does not cover non-deposit investment products, even those offered by FDIC-insured banks. FDIC insurance covers deposits received at an insured bank, but does not cover investments, even if they were purchased at an insured bank.

FDIC deposit insurance covers $250,000 per depositor, per FDIC-insured bank, for each account ownership category. All of your deposits in the same ownership category in the same FDIC-insured bank are added together for the purpose of determining FDIC deposit insurance coverage. However, you may qualify for more than $250,000 in FDIC deposit insurance coverage if you deposit money in accounts that are in different ownership categories. For example, if you have a single ownership account at an FDIC-insured bank, and you also have a joint ownership account with one or more people at the same bank, you will be insured for up to $250,000 for your single ownership account deposits and also insured separately for your ownership interest up to $250,000 for all of your joint ownership account deposits.

The FDIC manages two deposit insurance funds, the Bank Insurance Fund (BIF) and the Savings Association Insurance Fund (SAIF). The BIF insures deposits in commercial banks and savings banks up to a maximum of $100,000 per account. Insured banks pay for deposit insurance through premium assessments on their domestic deposits. Foreign deposits are not insured and are not subject to deposit insurance premiums.

The FDIC has an online Electronic Deposit Insurance Estimator (EDIE) that can be used to calculate how much of your funds are covered by deposit insurance.

How FDIC Insurance Protects Your Bank Account

You may want to see also

Explore related products

![]()

Deposit insurance history

The concept of deposit insurance originated in the United States in 1829, when New York created the first insurance program. Before the federal government adopted deposit insurance as policy in 1933, a total of 14 states had established deposit insurance systems. State insurance funds were successful until the National Bank Act of 1863. After the National Bank Act, many state banks converted to national charters to avoid the national tax on state bank notes, causing state deposit insurance funds to lose their effectiveness. Later, agricultural crises in the late 1920s contributed to the ultimate collapse of state insurance funds, as these funds could not diversify their risk.

The Federal Deposit Insurance Corporation (FDIC) is an independent federal government agency that insures deposits in commercial banks and thrifts. The FDIC was founded in 1933 after the stock market crash of 1929, which caused more than 9,000 banks to fail by March 1933. The FDIC was created to help boost confidence among consumers about the health and well-being of the nation's financial system. Since its founding, no depositor has lost any FDIC-insured funds. The FDIC helps maintain stability and public confidence in the U.S. financial system by insuring deposits of up to $250,000 per depositor, per ownership category at each FDIC-insured bank. This limit can be exceeded if funds are deposited in accounts with different ownership categories.

The FDIC manages two deposit insurance funds: the Bank Insurance Fund (BIF) and the Savings Association Insurance Fund (SAIF). The BIF insures deposits in commercial banks and savings banks up to a maximum of $100,000 per account. Insured banks pay for deposit insurance through premium assessments on their domestic deposits. The FDIC receives no taxpayer money or appropriations from Congress. Instead, it is funded by insurance premiums paid by banks and from interest earned on the FDIC's Deposit Insurance Fund (DIF), which is invested in U.S. government obligations. The interest earned on these notes helps the DIF grow. The DIF is backed by the full faith and credit of the United States government.

The FDIC has two options when a bank fails. The first is to sell the bank to a willing buyer, which may take on a portion or all of the failed bank's assets and liabilities. The second is to pay off the insured deposits and liquidate the failed bank's assets, with uninsured depositors recuperating money based on the value of the assets. The FDIC can also offer open bank assistance (OBA), in which it arranges for the purchase or recapitalization of an institution before it fails. Uninsured depositors are usually protected in these transactions.

Chase Bank: How FDIC Insurance Works

You may want to see also

Frequently asked questions

The Federal Deposit Insurance Corporation (FDIC) is an independent federal government agency that insures deposits in commercial banks and thrifts.

The FDIC provides \$250,000 in coverage per depositor, per account. However, you may qualify for more than \$250,000 in FDIC deposit insurance coverage if you deposit money in accounts that are in different ownership categories.

The FDIC provides deposit insurance to protect your money in the event of a bank failure. The FDIC helps maintain stability and public confidence in the U.S. financial system.