Auto insurance is expensive for a variety of reasons. Firstly, insurance companies deem young and inexperienced drivers to be more likely to get into accidents, and therefore charge higher rates for drivers in their 20s. Secondly, insurance rates vary depending on location, with drivers in densely populated areas facing higher premiums due to increased risks of accidents, violations, and theft. Thirdly, insurance costs are influenced by the type of car, with luxury, sports, and high-tech vehicles being more expensive to insure due to costly repairs and replacement parts. Fourthly, insurance companies take into account personal characteristics such as marital status, education level, and credit score, which can impact rates. Finally, insurance rates have been rising due to inflation and increased claims, with repair costs for modern, tech-laden vehicles soaring.

Explore related products

What You'll Learn

![]()

High-risk drivers

Insurance companies often charge high-risk drivers higher rates or even refuse to offer them a policy. This is because high-risk drivers are statistically more likely to exhibit unsafe driving behaviours and file more claims. High-risk drivers are also more likely to have their coverage denied or face higher premiums if they have a history of serious driving violations, such as hit-and-run, road rage, reckless driving, or excessive speeding.

Young drivers, in particular, tend to display riskier driving behaviours and are more likely to be involved in accidents due to their lack of experience. As a result, insurance companies charge them higher rates. Similarly, drivers with poor credit scores are also deemed high-risk, as insurers have observed a correlation between poor credit and risky driving behaviour.

To reduce their insurance costs, high-risk drivers can take steps such as improving their credit score, taking defensive driving courses, and maintaining a safe driving record over time.

MetLife: Gap Insurance Coverage

You may want to see also

Explore related products

![]()

Young drivers

Auto insurance for young drivers is expensive because insurance companies consider them high-risk clients. Young drivers are more likely to be involved in accidents due to their inexperience and tendency to engage in risky behaviours like speeding or driving under the influence. This makes them more expensive to insure, as the increased risk of accidents leads to higher chances of insurance companies having to pay out claims.

Risk and Inexperience

Insurers base their rates on risk assessment, and young drivers are statistically more likely to be involved in accidents or commit traffic violations. Their lack of experience means they are still adjusting to the nuances of driving and gaining confidence in navigating unexpected situations on the road. This inexperience can lead to mistakes such as failing to check blind spots or driving too fast, which are common causes of accidents and insurance claims.

Distracted Driving

Higher Claims Cost

It's not just the frequency of accidents that matters, but also the cost of claims. Data shows that the average cost of a claim for a young driver is significantly higher than that of an older motorist. This is because younger drivers tend to have more serious accidents, resulting in higher repair bills and more expensive personal injury claims.

Gender

Additionally, gender plays a role in insurance rates, with young male drivers often paying more than their female counterparts. This is due to statistical evidence showing that young males are more likely to engage in aggressive driving behaviours and are involved in more fatal accidents.

Credit Score

In some cases, a young driver's credit score can also impact their insurance rates. Those with low credit scores or no credit history may be considered higher-risk clients and charged higher premiums.

Location

The cost of living in certain areas can also influence insurance rates. Higher costs of living generally result in higher insurance premiums, as young drivers may be seen as riskier clients in these locations.

Strategies to Reduce Insurance Costs

While insurance rates for young drivers are inherently higher, there are strategies to mitigate these costs:

- Staying on a parent's insurance policy is often more cost-effective than purchasing a separate policy.

- Taking a defensive driving or driver safety course can lead to discounts and lower rates, as it demonstrates a commitment to safe driving.

- Maintaining good grades can result in good student discounts, as there is a correlation between academic performance and responsible driving behaviour.

- Choosing a safer and more practical vehicle can help lower insurance costs, as sports cars or high-performance vehicles tend to be more expensive to insure.

- Installing additional safety features, such as alarms or etching the VIN into the windshield, can lead to discounts and lower rates.

- Improving credit scores can positively impact insurance rates, as it reflects financial responsibility.

- Shopping around and comparing rates from different insurance providers can help identify the most competitive rates and discounts offered for young drivers.

Vehicle Insurance: Is It Mandatory in Massachusetts?

You may want to see also

Explore related products

![]()

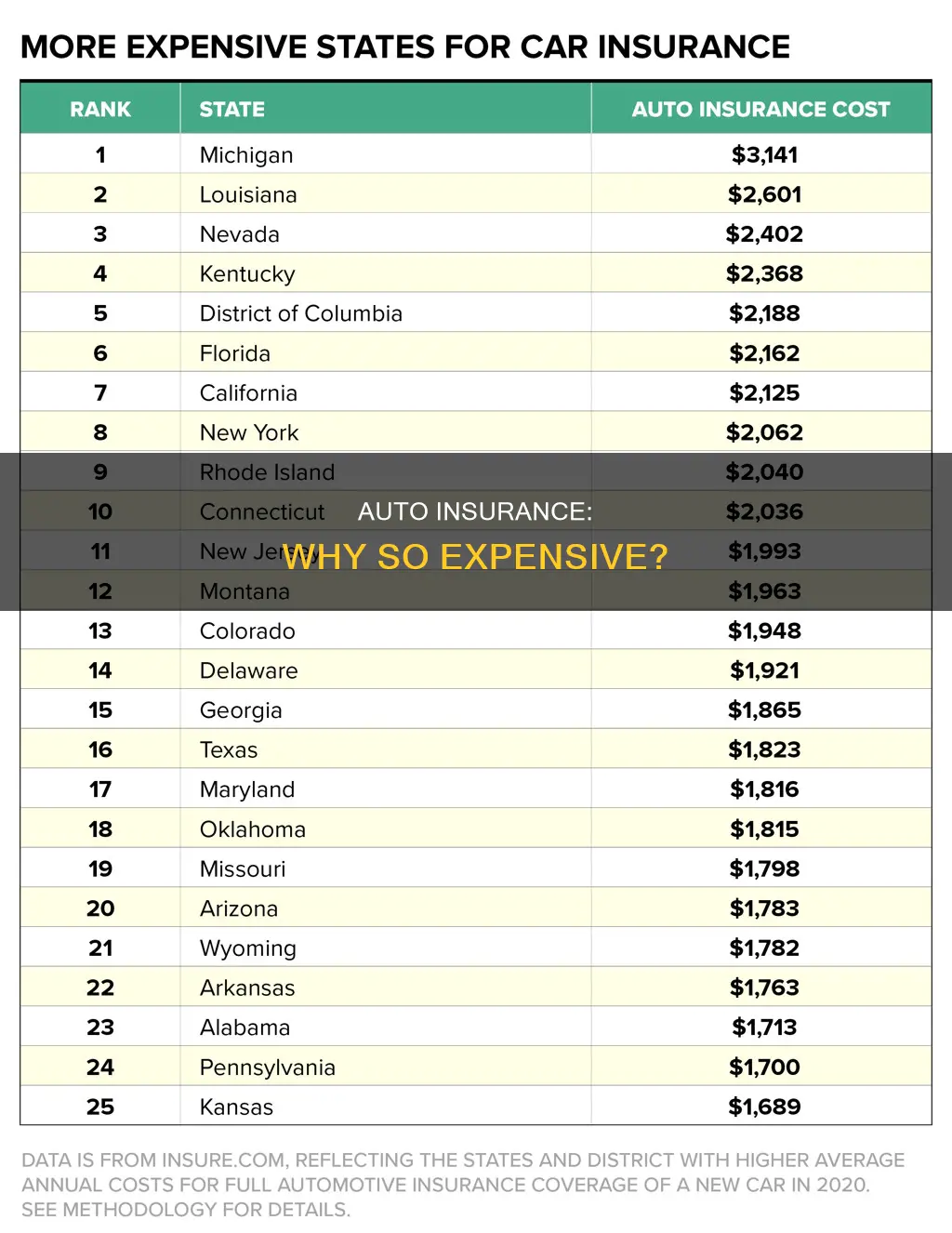

Location

Some states require drivers to carry higher levels of car insurance coverage, which raises costs. Living in a place where car insurance repairs are more expensive or where there is a high likelihood of theft and vandalism also increases the cost of coverage. Additionally, living in a location prone to severe weather—such as flooding or hail—can contribute to higher car insurance rates.

The average annual cost of car insurance nationwide is $2,118, but drivers in New York pay the most ($4,769 per year), while folks in Idaho pay the least ($1,021).

Michigan is a notoriously expensive state to insure a vehicle. Michigan drivers pay 73% more than the national average for car insurance. Three primary factors contribute to Michigan's high auto insurance rates:

- Michigan requires no-fault insurance with unlimited Personal Injury Protection (PIP).

- The insurance coverage options offered in Michigan attract insurance fraud, litigation fees and expensive healthcare bills.

- Insurance companies have to charge higher premiums in Michigan to earn a profit.

Florida is the third most expensive state to insure a vehicle, with a statewide average of $2,425 per year. The major reason for this is the insurance companies' loss-to-profit ratio in Florida. Hurricanes and flooding result in car insurance companies paying out heavy claim losses on a regular basis.

Louisiana is the most expensive state for car insurance, with an average cost of $3,265 per year. Like Florida, Louisiana is considered a high-risk state from an insurance provider's perspective, with an increased likelihood of claim losses due to hurricanes, flooding and other natural disasters.

Tennessee Auto Insurance: Is It Mandatory?

You may want to see also

Explore related products

![]()

Vehicle type

The type of car you drive can also impact your car insurance rates, especially if you buy collision and comprehensive insurance.

Cars with advanced safety equipment like parking assist and lane departure warnings can increase repair costs because the equipment is more expensive to repair or replace.

Cars with racing-spec engines, an array of high-tech features, or a luxury price tag will be more expensive to insure. Vehicles with the following attributes cost more to insure:

- Advanced tech features

- Sport design or functionality

- High likelihood of theft

Luxury cars, sports cars, and full-size pickup trucks are the most expensive vehicles to insure.

For example, the Tesla Model S Performance, Volvo XC90 T8 Inscription, and Dodge Ram 1500 Rebel are among the most expensive cars to insure.

On the other hand, the Honda CR-V, Jeep Wrangler Sport, and Subaru Crosstrek are among the least expensive cars to insure.

The make and model of your vehicle play a major role in determining your insurance costs. Certain vehicles are deemed riskier to insure, which can raise the cost of your car insurance policy.

For instance, insurance providers might consider you more likely to get into an accident or receive a speeding ticket if you have a car with a powerful engine.

The trim level of your car can also impact your insurance rates. Newer cars with high-tech features will cost more to repair or replace, leading to higher insurance rates.

Additionally, luxury and high-performance cars, such as the Porsche Panamera, Maserati Quattroporte, Audi R8, and Mercedes-AMG GT, typically come with hefty insurance bills.

When choosing a vehicle, it's important to consider not only the purchase price but also the ongoing cost of insurance. By selecting a car with good safety features and a lower risk profile, you can keep your insurance costs relatively low.

Drunk Driving: Auto Insurance Coverage?

You may want to see also

Explore related products

![]()

Credit score

Auto insurance companies use credit-based insurance scores to help them decide whether to take on a policyholder and what premium they will charge. While it is only one of many factors, a good credit score can help you save money. Credit-based insurance scores are calculated differently from the credit scores calculated by FICO and VantageScore, which are used by creditors. While these credit scores predict the likelihood of a consumer falling behind on payments, credit-based insurance scores predict the likelihood of a consumer filing insurance claims that will cost the company more money than it collects in premiums.

In the US, most states permit insurers to factor in credit history when determining rates. However, California, Hawaii, Massachusetts, and Michigan prohibit or limit the use of credit information in setting auto insurance rates. In these states, your credit score will not affect your insurance rates, regardless of how good or bad it is.

If you have a low credit score, there are strategies to improve it. Paying your bills on time, decreasing your credit card debt, and keeping hard credit inquiries to a minimum can help boost your score. Improving your credit score can lead to better insurance rates and unlock other benefits, such as loan approvals and more favourable interest rates.

Southern vs Auto Owners: Insurance Differences

You may want to see also

Frequently asked questions

There are several factors that contribute to the high cost of auto insurance. Firstly, the increasing complexity of modern vehicles, loaded with technology and specialized materials, has led to a rise in repair costs. This, combined with inflation and supply chain issues, has resulted in higher insurance rates. Additionally, personal characteristics such as age, gender, marital status, occupation, and credit score can influence insurance rates, with younger and high-risk drivers often facing higher premiums. Location also plays a significant role, with densely populated areas and states with higher claims and uninsured drivers tending to have more expensive insurance.

The cost of repairing vehicles has been increasing due to the advanced technology and specialized parts used in modern cars. As a result, insurance companies have to pay more to cover the repairs or replacement of these vehicles, which leads to higher insurance rates for their customers.

Yes, insurance companies take into account various personal characteristics when determining insurance rates. For example, younger and less experienced drivers are often considered high-risk and charged higher rates. Additionally, factors such as gender, marital status, occupation, and credit score can also influence insurance rates, with rates varying across different states and even ZIP codes.

To reduce auto insurance costs, it is recommended to shop around and compare quotes from multiple insurance companies. Other strategies include choosing a car with good safety features, enrolling in usage-based insurance programs, increasing your deductible, and taking advantage of discounts offered by insurance providers, such as those for bundling policies or having a good student discount.