There are several reasons why you may want to convert your term life insurance to permanent life insurance. Unlike term life insurance, which offers coverage for a fixed period, permanent life insurance provides lifelong protection and the potential for cash value accumulation. This means that your loved ones will receive a payout regardless of when you pass away, and you can also build a stable cash value over time. Additionally, converting your policy can be done without a health exam, and you may be able to convert all or just a part of your term life insurance. However, it's important to note that premiums for whole life insurance are typically higher, and you should review your current policy to understand any limitations or requirements for conversion.

| Characteristics | Values |

|---|---|

| Protection | Permanent life insurance offers lifelong protection and potential cash value accumulation. |

| Cost | There is usually no direct cost to convert term life insurance to a permanent policy, but premium payments will likely be higher. |

| Coverage | Permanent life insurance has no expiration date, unlike term life insurance. |

| Cash value | Permanent life insurance grows cash value that you can access during your life. |

| Health | Converting to permanent life insurance may be a good option if your health has worsened, as the company won't consider your health when you convert. |

| Age | Converting to permanent life insurance may be a good option if you are older, as the benefits of stable cash value and leaving a legacy may be more appealing. |

| Complexity | Term life insurance is less complex than permanent life insurance. |

| Budget | Term life insurance is more budget-friendly than permanent life insurance. |

Explore related products

What You'll Learn

- Permanent life insurance offers lifelong protection and cash value accumulation

- You can convert all or some of your term life insurance to permanent life insurance

- Converting is a good option if you have a serious health condition

- Permanent life insurance is a good option for those with long-term obligations

- Converting is easier than applying for a new policy

![]()

Permanent life insurance offers lifelong protection and cash value accumulation

Permanent life insurance offers lifelong protection, ensuring that your beneficiaries receive a payout no matter when you pass away, provided the premiums are paid. This type of insurance also includes a savings element, known as the cash value component, which accumulates over time and can be utilised by the policyholder.

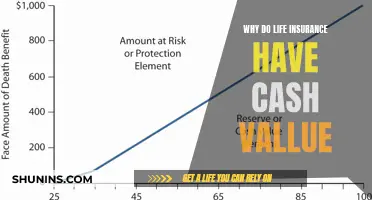

The cash value in a permanent life insurance policy is usually subject to the policy's performance and the insurer's investment strategy and is generally not guaranteed. Whole life insurance offers a guaranteed minimum cash value, but other types of permanent life insurance, such as universal and variable life insurance, may fluctuate with market conditions. Policyholders should review their policy details to understand the guarantees and potential risks of their cash value life insurance.

The cash value component of permanent life insurance can provide several benefits. Firstly, it can be borrowed against, providing a source of funds in emergencies or for other financial needs. Secondly, withdrawals are also possible, but it's important to note that they may affect the death benefit portion and could incur taxes. Additionally, the cash value can grow tax-deferred, and some policies offer tax-efficient loans and withdrawals, further enhancing the financial benefits.

Converting term life insurance to permanent life insurance can be advantageous in certain situations. Permanent life insurance offers lifelong protection, whereas term life insurance typically covers a limited period, such as 10, 20, or 30 years. By converting to a permanent policy, individuals can ensure that their loved ones are financially protected regardless of their lifespan. Additionally, permanent life insurance provides the opportunity for cash value accumulation, which can be a valuable source of funds during emergencies or retirement.

It's important to consider the financial implications when deciding whether to convert to permanent life insurance. While there is usually no direct cost to convert, the premium payments for permanent life insurance are typically higher than those for term life insurance. Individuals should assess their financial stability and ensure they can comfortably afford the higher premiums to avoid losing coverage.

Life Insurance and HIPAA: What's the Connection?

You may want to see also

Explore related products

![]()

You can convert all or some of your term life insurance to permanent life insurance

There is usually no direct cost to convert term life insurance to a permanent policy, but your premium payments will likely be higher. If you choose a total conversion, the amount of your new coverage will be the same as your term insurance. For example, if you have a $250,000 death benefit through your term life insurance, your new permanent life insurance contract will also be $250,000. If you opt for a partial conversion, you will have both a term and a permanent policy active at the same time, which is usually more cost-effective in the long term than having permanent life insurance alone.

Permanent life insurance has the added benefit of a cash value component that accumulates in the policy and grows with interest over time. This cash value is guaranteed to grow over time and is unaffected by market fluctuations. You can use the cash value to borrow money in the form of a life insurance loan or even to pay your premiums.

It's important to note that not all term life insurance is convertible, so be sure to check your policy or speak to your insurance company. Policies also typically allow conversions only until the policyholder reaches a certain age, usually 65 or 70.

Disputing Life Insurance Denials: What's the Time Limit?

You may want to see also

Explore related products

![]()

Converting is a good option if you have a serious health condition

Converting term life insurance to permanent life insurance is a good option if you have a serious health condition. Permanent life insurance provides lifelong coverage, which means your loved ones will receive a payout when you pass away, regardless of how long you live. This is especially important if you want to ensure you leave a financial gift to your family.

When you convert term life insurance to permanent coverage, it is often done easily and generally without another medical exam. Your new permanent policy premium will be based on the rate class from when you originally purchased your term coverage and had a medical exam. This means that your health status will not influence the premium rates, which is a large advantage if you've developed conditions that would make a new permanent life policy too expensive or even unattainable.

Additionally, permanent life insurance policies typically have a cash value component, which can grow over time. This can be used as a form of savings or investment that the policyholder can borrow against if needed. This cash value accumulates in the policy and grows tax-deferred. However, it's important to note that it can take many years for the cash value to build substantially, and you may pay a surrender charge during the first few years of the policy.

When considering converting your term life insurance to permanent coverage, it's important to keep in mind that premium payments for permanent life insurance are typically higher. You will need to be within your policy's conversion window, and some insurers also have a maximum age requirement, such as 65 or 75 years old.

Life Insurance: Term vs Universal, Which is Cheaper?

You may want to see also

Explore related products

![]()

Permanent life insurance is a good option for those with long-term obligations

Term life insurance typically offers coverage for a limited duration, such as 10, 20, or 30 years. This can be sufficient for covering temporary responsibilities, such as paying off a mortgage or supporting dependent children until they become financially independent. However, if the insured person does not pass away within the policy's timeframe, the coverage expires, and the money invested in the policy may not be recouped.

On the other hand, permanent life insurance provides lifelong protection. It guarantees a death benefit regardless of when the insured person passes away. This makes it suitable for long-term obligations, such as ensuring financial support for a spouse or dependent children even after the policyholder's death. Permanent life insurance also offers the ability to build stable cash value over time, which can be accessed by the policyholder during their lifetime. This cash value component can be used for various purposes, such as borrowing money or paying premiums, and it grows tax-deferred, making it a valuable part of an overall financial strategy.

Converting from term to permanent life insurance can be advantageous for those with changing financial goals or health conditions. It allows individuals to extend their coverage beyond the original term period, ensuring that their loved ones will receive a payout regardless of when they pass away. Additionally, permanent life insurance policies often do not require a new health exam for conversion, making it a viable option for those who may have developed health issues since their original policy was issued.

However, it is important to consider the increased cost associated with permanent life insurance. Premiums for whole life insurance are generally higher than those for term life insurance. While the added benefits of permanent coverage are valuable, individuals must ensure they are financially stable enough to shoulder the higher expenses. Partial conversion, where only a portion of the term coverage is converted to permanent, can be a viable option to balance cost and the desire for extended coverage.

Life Insurance: How Long Should You Keep It?

You may want to see also

Explore related products

![]()

Converting is easier than applying for a new policy

Converting term life insurance to permanent life insurance is often easier than applying for a new policy. This is because, when taking out a new policy, most insurers will consider your current health, and you may have to take a medical exam. However, when converting a term life insurance policy, your health is typically not taken into account, and you usually won't need to take another medical exam. This means that if your health has deteriorated since you took out your original policy, you won't have to worry about paying higher rates due to increased health risks.

Another reason converting is easier than applying for a new policy is that you won't have to go through the underwriting process again. This can save you time and effort, as the underwriting process can be complex and involve a lot of paperwork. Additionally, your new permanent policy premium will be based on the rate class from when you originally purchased your term coverage and had a medical exam. The cost difference can be significant if you've had term coverage for a while and are now several years older.

It's important to note that not all term life insurance policies are convertible, so be sure to check with your insurance company. If your policy doesn't include a conversion privilege or rider, you may be able to add one, giving you the option to convert some or all of your term life policy to a permanent one. When deciding whether to convert, consider your financial situation, as premiums for whole life insurance are often more expensive than those for term life. Converting to whole life insurance may not be beneficial if you're not in a stable financial position, as you could risk losing your coverage if you're unable to pay the higher premiums.

Whole Life Insurance: Where to Get Covered for Good

You may want to see also

Frequently asked questions

Permanent life insurance offers lifelong protection and the potential for cash value accumulation. This means that your loved ones are likely to receive a payout when you pass away, regardless of when that is. Permanent life insurance also offers stable cash value and the ability to leave a legacy.

Permanent life insurance is more expensive than term life insurance. While the added benefits are typically worth the additional cost, it’s possible that you’re not in a position to shoulder the expense.

Contact your insurance company to begin the process. They will walk you through the details, including how much of your existing coverage you can convert and how much the conversion will cost. After finalising the details, you'll have a new policy.

The right time to convert is when you realise your circumstances are going to change or you need coverage for longer than you first thought. It is also worth considering conversion if your health has worsened, as this may make a new life insurance policy difficult or impossible to get.

There is usually no direct cost to convert, but your premium payments will likely be higher.