Deposit insurance is a guarantee that depositors will be reimbursed if their bank fails. This assurance can prevent bank runs by maintaining depositor confidence in the banking system. The Federal Deposit Insurance Corporation (FDIC), established in 1933, provides insurance for all banks and is mandatory for all federally-chartered banks and savings institutions. While deposit insurance may prevent bank runs, it also has unintended consequences, such as encouraging banks to take on excessive risk and reducing depositor discipline. The effectiveness of deposit insurance depends on its design and administration, and it must be accompanied by other measures to strengthen the banking system, such as increased scrutiny of banks and more effective capital and liquidity regulation.

Explore related products

What You'll Learn

![]()

Deposit insurance restores depositor confidence

Deposit insurance is a crucial tool for restoring depositor confidence and preventing bank runs. The assurance that depositors will be reimbursed in the event of a bank failure instils confidence in the market. This confidence-building mechanism is particularly important given the significant social and fiscal costs associated with banking crises.

The Federal Deposit Insurance Corporation (FDIC), established in 1933 following a wave of bank failures and runs, provides insurance for all banks. FDIC-insured banks are required to join the Federal Reserve System, and the FDIC has regulatory and examination functions. The creation of the FDIC was a pivotal step in restoring depositor confidence by providing a safety net for depositors.

However, deposit insurance alone is not enough to prevent bank runs. It must be complemented by other measures to strengthen the banking system. These include increased scrutiny of mid-sized banks, more stringent capital regulations, and more effective liquidity regulation. Additionally, deposit insurance schemes should incorporate features that help internalize risk-taking by banks, such as limited coverage and risk-adjusted premiums.

The design of deposit insurance is critical. Poorly designed schemes can increase the likelihood of a banking crisis and distort incentives for both bank managers and depositors, leading to excessive risk-taking. Therefore, deposit insurance should be optimally designed to balance the trade-off between welfare benefits and the costs of coverage. While higher coverage limits can reduce the probability of bank failures, they may also encourage riskier behaviour by banks.

In conclusion, deposit insurance plays a vital role in restoring depositor confidence and preventing bank runs. However, it should be implemented as part of a comprehensive framework that includes regulatory measures and careful consideration of coverage limits to balance the benefits and costs effectively.

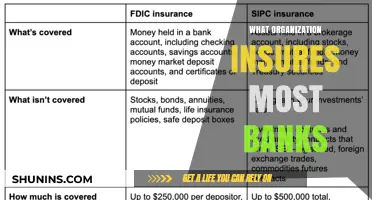

Understanding FDIC Insurance Limits: One Account or One Bank?

You may want to see also

Explore related products

![]()

It prevents contagion effects

Deposit insurance is a vital tool in preventing bank runs and the contagion effects that may follow. Bank runs can have a ripple effect, triggering a full-blown contagion. Concerns about the insolvency of one bank can spread, leading to multiple bank failures. This was evident in the 2023 regional banking crisis, where the collapse of Silicon Valley Bank , the 16th largest lender in the US, was followed by the failure of Signature Bank and First Republic Bank. These consecutive failures prompted policymakers and legal scholars to call for unlimited deposit insurance.

Deposit insurance guarantees that depositors will get their money back if their bank fails. This assurance brings confidence to the market and prevents depositors from rushing to withdraw their funds, which could lead to a bank run. By ensuring depositor confidence, deposit insurance acts as a safety net, reducing the likelihood of a contagion effect.

However, deposit insurance must be carefully designed and accompanied by other measures to strengthen the banking system. Poorly designed deposit insurance schemes can distort incentives for both bank managers and depositors, leading to excessive risk-taking and moral hazard. Therefore, deposit insurance should be complemented by stringent capital regulations and prompt supervisory actions to address risks effectively.

Additionally, the effectiveness of deposit insurance depends on the institutional environment. In countries with strong institutions and rule of law, both public and private monitoring can help maintain financial stability. However, in countries lacking robust institutional frameworks, explicit deposit insurance may do more harm than good. Thus, it is essential to strike a balance between the benefits and costs of deposit insurance to prevent contagion effects and ensure the stability of the banking system.

Exploring Private Insurance Bans Around the Globe

You may want to see also

Explore related products

![]()

It must be complemented by other actions

Deposit insurance is an effective tool to prevent bank runs, but it must be complemented by other actions to strengthen the banking system. While it ensures depositor confidence and prevents bank runs by guaranteeing that depositors will get their money back if their bank fails, it also encourages banks to take on excessive risk and distort incentives for both bank managers and depositors. This can lead to an increase in bank failures, causing serious disruptions to a country's economic activities and significant social and fiscal costs. Therefore, it is important for deposit insurance to be optimally designed and administered, with features that help internalize risk-taking by banks, such as limited coverage, risk-adjusted premiums, and more stringent capital regulations.

In addition, countries should cultivate an environment that empowers private market participants, such as large uninsured depositors, shareholders, and creditors, to monitor the banks they invest in. This is especially important in countries with strong institutions and rule of law, where both public and private monitoring can be effective. However, in countries with weak institutional environments, explicit deposit insurance may do more harm than good in terms of improving financial stability.

To address these challenges, regulators can use a framework that weighs the trade-off between the welfare benefits and the costs of deposit insurance coverage. This allows them to set optimal coverage limits that reduce the probability of bank failures without encouraging riskier behavior by banks. For example, the Federal Deposit Insurance Corporation (FDIC) in the United States provides insurance for all banks and has the authority to revoke a bank's deposit insurance, essentially forcing its closure.

Furthermore, deposit insurance should be complemented by increased scrutiny of mid-sized banks, more imaginative stress tests, and more effective capital and liquidity regulation. For instance, the Federal Reserve Act of 1913 was created to prevent bank runs by injecting liquidity into the financial markets and maintaining depositor confidence. Regulators must also consider the impact of technological advances and increased digitalization, as depositors become more sensitive to price and risk, making it challenging to ensure the stability of the banking system.

Healthcare Coverage: Public vs Private Options Explored

You may want to see also

Explore related products

![]()

It can encourage excessive risk-taking

Deposit insurance is a safety net that protects depositors' interests and helps prevent bank runs. However, it has been argued that deposit insurance can encourage excessive risk-taking by banks. This is because when deposits are insured, depositors may lack the incentive to monitor the bank's activities and risk exposure. This lack of market discipline can lead to excessive risk-taking by banks, which may culminate in banking crises.

The argument is supported by several studies, including those by Demirguc-Kunt and Huizinga (2004) and Ioannidou and Penas (2010). These studies find that deposit insurance can reduce the incentive for depositors to monitor banks, leading to a higher level of risk-taking. Additionally, it is believed that insurance companies may inadvertently encourage risk-taking by offering payouts to protect against losses.

Risk-based deposit insurance has been proposed as a solution to mitigate this issue. With risk-based insurance, banks are required to pay higher insurance premiums if they take on more risk. The idea is that this type of insurance will discourage reckless behaviour as banks will have to face the true cost of risk. However, the effectiveness of risk-based deposit insurance relies on the insurer's ability to fully understand the risk characteristics of the bank's investment portfolio, which can be challenging.

Furthermore, critics argue that the government may lack the resources or information to correctly assess bank risk and charge appropriate insurance premiums. Any risk-based premium charged may be deemed unfair, leading to distortions and inefficiencies in the banking sector. Therefore, while deposit insurance can help prevent bank runs, it must be accompanied by other measures to strengthen the banking system, such as increased scrutiny of banks and more effective capital and liquidity regulation.

In conclusion, while deposit insurance can be effective in preventing bank runs, it may also encourage excessive risk-taking by reducing the incentive for depositors to monitor banks. This can lead to increased risk-taking and potentially higher costs when banks fail. Therefore, it is important to design deposit insurance optimally and consider its potential impact on risk-taking behaviour.

Private Disability Insurance: Taxable Income?

You may want to see also

Explore related products

![]()

It reduces depositor discipline

Deposit insurance is a guarantee that depositors will be reimbursed if their bank fails. This assurance can increase depositor confidence and prevent bank runs. However, it has been argued that deposit insurance reduces "depositor discipline".

Depositor discipline refers to the ability of depositors to monitor and police bank activity. Without deposit insurance, depositors would be incentivized to closely scrutinize their bank's financial health and withdraw their deposits if they suspected insolvency. This form of market discipline helps to prevent banks from engaging in excessive risk-taking and maintains the stability of the banking system.

However, deposit insurance can reduce the effectiveness of depositor discipline. When depositors are assured that their funds are protected, they may become less vigilant in monitoring their bank's activities. They may no longer feel the need to withdraw their deposits in response to signs of financial distress, as they are guaranteed to be reimbursed. This reduction in depositor discipline can lead to a moral hazard problem, where banks are incentivized to take on excessive risks without facing the full consequences of their actions.

To mitigate the reduction in depositor discipline, it is important for deposit insurance schemes to be well-designed. Limited coverage, risk-adjusted premiums, and stringent capital regulations can help to internalize the risks of excessive risk-taking by banks. Additionally, empowering supervisors to take prompt corrective action can help to maintain discipline in the banking system.

While deposit insurance can reduce depositor discipline, it is important to note that depositor discipline is not the only factor governing the banking system. If depositor discipline were the sole governing force, there would likely be an increase in bank runs, losses for small savers, and economic instability, particularly in credit markets. Therefore, the challenge of maintaining a successful deposit insurance system lies in balancing depositor discipline with the overall stability of the banking system.

Americans With Private Health Insurance: How Many?

You may want to see also

Frequently asked questions

Deposit insurance is a guarantee that depositors will get their money back should their bank fail.

Deposit insurance brings confidence to the market and prevents a spiral of panic that can be caused by bank runs.

Deposit insurance can reduce "depositor discipline", which is the depositor's means of policing bank activity. It can also encourage banks to take on excessive risk.

The effectiveness of deposit insurance depends on how well it is designed and administered. It should be complemented by more stringent capital regulations and a system of oversight.