The Health Insurance Marketplace, also known as the exchange, is an organized market where individuals and families can shop for and enroll in health insurance. It is a federal health insurance program for people aged 65 and older and certain younger people with disabilities, as well as those with End-Stage Renal Disease. The Marketplace offers a range of different health plans, provides information to consumers, and offers financial assistance to enrollees based on their income. While the Marketplace is a government-run program, there are also private health insurance exchanges, such as eHealth, that offer ACA plans with the same essential Obamacare benefits as state or federal marketplaces. These private exchanges can help individuals navigate and compare plans to find the lowest prices. However, it's important to note that Marketplace plans and non-Marketplace plans differ in that the latter does not provide premium subsidies, and enrollees must pay rate increases themselves.

| Characteristics | Values |

|---|---|

| Nature of the entity | Marketplaces are organized markets where individuals and families can shop for and enroll in health insurance. |

| Nature of the service | Insurance provides financial protection against unexpected events, while a marketplace offers a platform for buying and selling goods or services, including insurance. |

| Eligibility | To be eligible for Marketplace health coverage, you must live in the US, be a US citizen or national, and not be incarcerated. |

| Enrollment period | There are limitations on when you can sign up for insurance on the marketplace, with a specified open enrollment period. Outside of this, there may be special enrollment periods after certain life events. |

| Plan availability | Plans available on the marketplace may vary by region, with some companies offering different plans in the private marketplace vs. a state's exchange. |

| Network variations | Plans on government marketplaces may have smaller provider networks compared to private marketplace plans. |

| Pricing | The price of a plan on the marketplace is the same regardless of where it is purchased. However, different people may pay different prices based on state, income, and household size. |

| Payment | When you have Marketplace insurance, you pay your monthly premiums directly to the insurance company, not to the Marketplace. |

| Financial assistance | Marketplaces may offer financial assistance, such as premium tax credits and cost-sharing reductions, based on income. |

Explore related products

What You'll Learn

![]()

Private health insurance exchanges

Private exchanges offer flexibility and choice, allowing employers to find plans that meet their specific needs and conform to ACA regulations. They are not insurers themselves, so they do not bear the risk, but they determine which insurance companies participate. An ideal private exchange promotes transparency, accountability, increased enrolment, and helps spread risk across a larger group of people.

Private exchanges can be used in both the individual and group markets. While the public exchanges/marketplaces established by the ACA provide options for individuals and small groups in certain states, there is no public exchange for large groups. As a result, large employers can utilise private exchanges to find suitable health plans for their employees.

Enrolling in a health insurance plan through a private exchange follows a similar process to that of a public exchange. Individuals or employers would visit a health insurance comparison site, submit an application, and choose a plan that best suits their needs. The monthly premiums are then paid directly to the insurance company, and coverage begins after the first premium payment.

It is important to note that private exchanges are not a recent development and have existed alongside public exchanges for several years. They provide an alternative option for individuals and employers to shop for health insurance plans outside of the ACA marketplace. By utilising private exchanges, consumers can compare benefits and prices across different insurance companies and select the plan that best meets their healthcare needs and budget.

Insurance Brand Toggle: 21st Century Update

You may want to see also

Explore related products

![]()

Limitations on when you can sign up

To be eligible to enrol in Marketplace health coverage, you must be a US citizen or national (or be lawfully present) and live in the United States. This is a federal health insurance program for people 65 and older and certain younger people with disabilities. It also covers people with End-Stage Renal Disease (permanent kidney failure requiring dialysis or a transplant).

There is no income limit for Marketplace eligibility, but your income will determine the amount of your health insurance costs. You can enrol in a tax credit when signing up for a plan through the Health Insurance Marketplace, and this will be based on the income estimate and household information you provide on your Marketplace application.

There is a yearly Open Enrollment Period when you can sign up for health insurance. This typically starts on December 15 for coverage from January 1, and on January 15 for coverage from February 1. However, there are some circumstances in which you can sign up outside of the Open Enrollment Period. You may qualify for a Special Enrollment Period if you have experienced certain life events, such as losing health coverage, moving, getting married, having a baby, or adopting a child. You may also qualify for a Special Enrollment Period if your household income is below a certain amount.

If you are eligible for a Special Enrollment Period, you can purchase health care insurance through the Marketplace outside of the open enrollment period. You can also enrol in Medicaid or the Children's Health Insurance Program (CHIP) at any time of year, and coverage can start immediately.

Insured in China: Nearly Universal

You may want to see also

Explore related products

![]()

Tax credits and cost-sharing reductions

The Affordable Care Act (ACA) provides two types of financial assistance to Marketplace enrollees: premium tax credits and cost-sharing reductions. Premium tax credits reduce enrollees' monthly payments for insurance coverage. The premium tax credit is refundable, meaning it is available to qualifying enrollees regardless of whether they owe any federal income tax. The amount of the premium tax credit is based on a sliding income scale, with lower-income enrollees receiving larger credits. The premium tax credit can be applied to any Marketplace plan except Catastrophic coverage.

Cost-sharing reductions (CSRs) are the second type of financial assistance available to Marketplace enrollees. Unlike premium tax credits, cost-sharing reductions are not provided as a tax credit and do not need to be reconciled when filing taxes. CSRs reduce enrollees' deductibles, copayments, and coinsurance, thereby lowering out-of-pocket costs. CSRs are only available for silver plans. People eligible for cost-sharing reductions who enroll in a silver plan will automatically receive a version of the plan with reduced cost-sharing charges.

Marketplaces will determine eligibility for advance tax credit payments and cost-sharing reductions for the coverage year in the fall before the new coverage year starts. Individuals and families with income up to 150% of the federal poverty level (FPL) will have a required contribution of zero, while those with income above 400% of the FPL will have a required contribution of 8.5% of household income.

The Health Insurance Marketplace Calculator can be used to estimate the amount of financial assistance an individual may receive. However, the calculator relies on the information entered by the user, while the Marketplace may calculate the Modified Adjusted Gross Income (MAGI) differently or verify income against previous years' data. Thus, the calculator results may not always match the actual tax credit amount received.

Teen Driver Insurance: What's the Cut-off Age?

You may want to see also

Explore related products

$37.99 $64.99

![]()

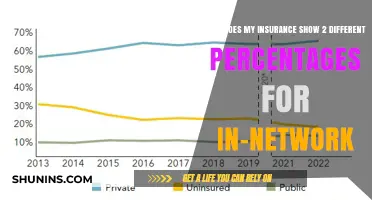

Different network structures

Health Insurance Marketplaces, also known as Exchanges, are organized markets where individuals and families can shop for and enrol in health insurance. Marketplaces offer a choice of different health plans, certify plans that participate, and provide information to help consumers understand their options and apply for coverage. There is a Health Insurance Marketplace in every state, with some operated by the State, like Covered California or The Maryland Health Benefit Exchange, and others run by the federal government, like HealthCare.gov.

Marketplace plans and non-marketplace plans are generally very similar, but they differ in their network structures. For example, Company A may offer a Cost-Effective Bronze HMO plan on a state exchange, but not on the private marketplace. Instead, Company A might offer a Budget-Friendly Bronze PPO plan in the private marketplace. Both plans include the 10 essential health benefits, but their network structures (HMO vs PPO) and other benefits differ.

HMO plans, or Health Maintenance Organization plans, typically limit coverage to a specific network of healthcare providers. This means that individuals can only receive coverage for services provided by in-network doctors or hospitals. PPO plans, or Preferred Provider Organization plans, on the other hand, offer more flexibility by allowing individuals to go out of network for their healthcare needs, although staying in-network may provide greater cost savings.

Additionally, the provider network associated with a company's exchange-based plan may include a smaller selection of healthcare providers and hospitals than the network associated with the same company's private marketplace plan. This is because health insurance carriers can lower their Obamacare exchange premium rates by only covering small or "narrow" networks of doctors.

It is important to carefully compare plan networks from the same company to ensure that the in-network options fit your personal preferences and are conveniently located.

ACA Marketplace: Insuring Millions

You may want to see also

Explore related products

![]()

Eligibility requirements

To be eligible to enrol in Marketplace health coverage, individuals must live in the United States, be a U.S. citizen or national (or be lawfully present), and not be incarcerated. There is also a yearly Open Enrollment Period for Marketplace health insurance, with the federal period running from November 1st to January 15th, and coverage starting on January 1st for those who sign up by December 15th. Outside of this period, individuals may qualify for a Special Enrollment Period if they experience certain life events, such as losing health coverage, moving, getting married, having a baby, or adopting a child. Individuals with a household income below a certain amount may also be eligible for a Special Enrollment Period.

Private health insurance exchanges, such as eHealth, also offer ACA plans that include the same essential Obamacare benefits as government-run marketplaces. These private marketplaces provide a convenient way for people from all states to buy marketplace and alternative health insurance plans. While the price of identical plans should be the same regardless of where they are purchased, private marketplaces may offer different plan options and network structures compared to government-run exchanges. For example, Company A may offer a Cost-Effective Bronze HMO plan on a state exchange, while only providing a Budget-Friendly Bronze PPO plan in the private marketplace.

Additionally, individuals who are 65 and older, have certain disabilities, or have End-Stage Renal Disease may be eligible for Medicare, which is a federal health insurance program. Similarly, Medicaid and the Children's Health Insurance Program (CHIP) provide free or low-cost health coverage to low-income individuals, families, children, pregnant women, the elderly, and people with disabilities. These programs are available in many states and individuals can enrol at any time of the year.

Understanding the Tax Benefits of Term Insurance: Exploring the 80C Connection

You may want to see also

Frequently asked questions

A health insurance marketplace is a place where individuals and families can shop for and compare health insurance plans. Marketplaces offer a choice of different health plans, certify plans that participate, and provide information to help consumers understand their options and apply for coverage.

Marketplace plans and non-marketplace plans are generally similar, but non-marketplace plans do not provide premium subsidies, and enrollees must pay rate increases themselves. Non-marketplace plans may also have smaller provider networks.

You will pay your monthly premiums directly to the insurance company, not to the marketplace. Your coverage will not start until you pay your first premium.

There are limitations on when you can sign up for a marketplace plan. The open enrollment period can vary between states, but the federal open enrollment period runs from November 1st to January 15th. There are also special enrollment periods outside of this time if you experience a qualifying life event, such as job loss, marriage, or moving.

You can review health care coverage options and purchase insurance through the Health Insurance Marketplace online, over the phone, or in person. Some states operate their own marketplaces, while others are run by the federal government through HealthCare.gov.