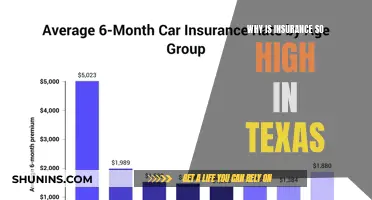

Memphis, Tennessee, has some of the highest insurance rates in the United States. The average cost of car insurance in Memphis is $1,700 per year, which is $371 more than Tennessee's average rate and $266 more than the national average. Memphis homeowners also pay an average of $3,931 annually for insurance, which is $1,349 more than the national average. This is due to a variety of factors, including age, driving record, credit score, and location.

| Characteristics | Values |

|---|---|

| Average annual car insurance rate in Memphis | $1,700 to $2,541 |

| Average monthly car insurance rate in Memphis | $180 |

| Average annual car insurance rate in Tennessee | $1,329 to $1,932 |

| Average monthly car insurance rate in Tennessee | $150 |

| Average annual homeowners insurance rate in Memphis | $2,974 to $3,931 |

| Average annual homeowners insurance rate in Tennessee | $2,582 to $2,685 |

| Average monthly homeowners insurance rate in Memphis | $328 |

| Average monthly homeowners insurance rate in Tennessee | $254 |

| Average annual cost of car insurance for Memphis seniors | $1,356 |

| Average monthly cost of car insurance for Memphis seniors | $113 |

| Average annual cost of car insurance for Memphis drivers with a speeding ticket | $3,576 |

| Average monthly cost of car insurance for Memphis drivers with a speeding ticket | $298 |

Explore related products

What You'll Learn

- Car insurance rates for teens and young adults are higher than for adults and seniors

- Speeding tickets and other driving violations can increase insurance rates

- Credit scores impact insurance rates

- Memphis is more at risk for natural disasters, resulting in higher rebuilding rates

- Insurance rates can vary depending on location, city demographics, and population density

![]()

Car insurance rates for teens and young adults are higher than for adults and seniors

Car insurance rates in Memphis, Tennessee, are higher than the state and national averages. The average cost of car insurance in Memphis is $180 per month, or $2,161 annually, which is $484 more than the state average in Tennessee and $266 more than the national average.

There are ways to make car insurance for teens and young adults more affordable. Maintaining a clean driving record and taking a professional driving course can help lower premiums. Carriers may also offer discounts for good students and safe driving. Additionally, opting for an older, used vehicle with high safety ratings can reduce insurance costs.

As drivers gain experience and age, their insurance rates will generally decrease. By the time a driver turns 25, their insurance premiums may be roughly half of what they were as a teenager. However, rates may start to increase again for senior drivers, as age-related factors such as slower reaction times and vision changes can increase the risk of accidents.

Auto Insurance: Uninsured Motorist Coverage Not Always Recommended

You may want to see also

Explore related products

![]()

Speeding tickets and other driving violations can increase insurance rates

Speeding tickets and other driving violations can have a significant impact on insurance rates. Insurance companies view drivers with recent tickets or accidents on their record as higher-risk, meaning they are more likely to file an insurance claim. As a result, insurers typically charge these drivers higher rates. The impact of a speeding ticket on insurance rates can vary depending on the driver's state and insurer, with some states imposing demerit points on the driver's license, which can further influence the insurance premium.

The increase in insurance rates due to speeding tickets is influenced by several factors, including the driver's insurance company, driving record, insurance history, and the speed at which they were travelling when cited. For example, speeding between 6-10 miles over the speed limit can result in an average increase of $40 per month in insurance costs, while speeding 21-25 mph over the limit can lead to an average increase of $54 per month. The frequency of speeding tickets also matters, with insurance rates likely to increase if a driver receives two or more tickets within a three-year period.

In addition to speeding tickets, other moving violations such as running a red light or stop sign, texting while driving, or driving under the influence (DUI) can also lead to higher insurance rates. The impact of these violations on insurance costs can vary by state, with a DUI conviction resulting in a 160% increase in rates in California but only a 73% increase in Maine.

The presence of a clean driving record can sometimes mitigate the impact of a speeding ticket on insurance rates. Some states offer drivers the opportunity to keep minor infractions off their record by completing a driving safety course or a driver safety class. Additionally, certain insurance companies may not increase rates for drivers with a single speeding ticket, and the impact of the ticket may only be temporary, lasting for three to five years.

It is important to note that insurance companies carefully review a driver's record when determining insurance rates, and the presence of speeding tickets or other driving violations can result in higher premiums. Drivers with a history of violations are encouraged to shop around and compare rates from multiple insurers to find the most affordable policy for their situation.

Mold Damage: Filing an Auto Insurance Claim

You may want to see also

Explore related products

$29.99 $29.99

$28.97 $32.97

![]()

Credit scores impact insurance rates

Credit scores have a significant impact on car insurance rates. A higher credit score can lead to lower insurance rates, while a lower credit score can result in higher rates. This disparity can be substantial, with drivers with poor credit paying up to 95% more for full coverage insurance compared to those with good credit. In some cases, individuals with excellent credit scores may pay an average annual rate of $2,286 for full coverage, while those with poor credit scores could face averages of $4,708 or more.

Insurance companies use credit-based insurance scores to evaluate an individual's credit history and determine their insurance rates. These scores are based on various factors, including outstanding debt, credit history length, credit mix, payment history, and pursuit of new credit. While each insurance company has its own proprietary formula for calculating credit-based insurance scores, the impact of credit scores on insurance rates is undeniable.

In most states, credit scores are a significant factor in determining car insurance rates. However, it is important to note that California, Hawaii, Massachusetts, and Michigan have regulations prohibiting or limiting the use of credit scores in setting insurance premiums.

In Memphis, Tennessee, car insurance rates are already higher than the state and national averages. The average annual cost of car insurance in Memphis is $2,161, which is $484 more than the Tennessee state average and $266 more than the national average. With such high insurance rates, the impact of credit scores on insurance premiums in Memphis is likely to be significant.

To find the most affordable car insurance options in Memphis, it is essential to compare rates from multiple insurance companies. While credit scores play a crucial role in determining insurance rates, other factors such as driving record, age, and vehicle type also come into play. By considering all these factors and shopping around, Memphis drivers can find the best value for their car insurance needs.

Understanding Auto Insurance Statements: What You Need to Know

You may want to see also

Explore related products

![]()

Memphis is more at risk for natural disasters, resulting in higher rebuilding rates

Memphis, Tennessee, is known to have higher insurance rates than the state and national averages. One of the contributing factors to this is the city's vulnerability to natural disasters, which leads to higher rebuilding costs.

Memphis has a higher risk of tornado damage than the Tennessee average and a significantly higher risk than the national average. From 1950 to 2010, 79 historical tornado events with recorded magnitudes of 2 or above were documented in or near Memphis. In December 1987, West Memphis, Arkansas, experienced three natural disasters: an EF-3 tornado, a flood, and a snowstorm. This resulted in six fatalities, over $25 million in damages, and more than 100 injuries. The city of West Memphis has since installed six tornado sirens and flood control systems to better prepare for such events.

In December 2021, Memphis experienced another tornado outbreak. A line of storms with embedded supercells produced damaging winds of up to 60-70 mph as they moved through the Memphis metropolitan area. This resulted in the derailment of over 20 railroad cars in southern Marion and the knocking down of large trees, some of which fell on homes.

While the chance of earthquake damage in Memphis is similar to the Tennessee average and lower than the national average, the occurrence of earthquakes is still a consideration. There have been four historical earthquake events with recorded magnitudes of 3.5 or higher in or near Memphis.

The vulnerability of Memphis to tornadoes and other extreme weather events contributes to the higher insurance rates in the city. The frequent occurrence of these natural disasters results in significant damage, including injuries, fatalities, and property destruction. This leads to increased rebuilding and recovery costs, which are reflected in the higher insurance premiums for the area.

Vehicles with Lower Insurance Rates

You may want to see also

Explore related products

![]()

Insurance rates can vary depending on location, city demographics, and population density

Insurance rates can vary depending on a multitude of factors, including location, city demographics, and population density. These factors can influence the cost of insurance in a given area, and understanding these factors can help explain why insurance rates in certain locations, such as Memphis, Tennessee, may be higher than average.

Location plays a significant role in insurance rates. For instance, the cost of homeowners insurance in Memphis is influenced by the property's location within the city. Areas that are more prone to natural disasters, such as floods, hurricanes, or tornadoes, typically face higher insurance premiums due to the increased risk of damage and the potential for higher rebuilding costs. This variation in rates based on location is also evident in car insurance, where premiums can differ widely depending on the specific neighbourhood or ZIP code within a city.

City demographics, including factors such as the average age of residents, accident rates, theft, and vandalism, can also impact insurance rates. For example, in Memphis, the average car insurance rate for seniors is $113 per month, while rates for teenagers and young adults are typically higher due to their limited driving experience and higher risk of accidents. Additionally, the presence of uninsured motorists in an area can influence insurance rates, as insurance companies may factor in the potential costs associated with accidents involving uninsured drivers.

Population density is another factor that can affect insurance rates. In densely populated areas, the frequency of accidents, theft, or vandalism may be higher, leading to increased insurance rates. On the other hand, in less densely populated regions, insurance rates may be lower due to reduced accident risks and lower costs associated with repairs or replacement of damaged property.

The interplay of these factors can result in insurance rates that are higher or lower than the state or national average. In the case of Memphis, Tennessee, car insurance rates are notably higher than the average rates in Tennessee and the national average. The annual cost of car insurance in Memphis is approximately $2,161, while the state average is $1,732, and the national average is $1,895. Similarly, homeowners insurance rates in Memphis are higher than the state and national averages, with residents paying an average of $328 per month, compared to the Tennessee average of $254 and the national average of $215.

To conclude, insurance rates are dynamic and influenced by a combination of location-specific factors, including city demographics and population density. By understanding these factors, individuals can make more informed decisions when comparing insurance rates and selecting the most suitable policies for their needs.

Auto Insurance Quotes: Stop the Spam

You may want to see also

Frequently asked questions

The average car insurance rate in Memphis is $180 per month, which is $484 more than the state average in Tennessee and $266 more than the national average. Memphis's insurance rates are influenced by factors such as location, city demographics, population density, average resident age, accident rates, and theft and vandalism.

Car insurance rates for teenagers and young adults are typically higher than for adults because teens have less experience driving and a more limited history, which puts them at a higher risk for accidents. Memphis seniors pay an average of $113 per month for car insurance.

A speeding ticket or moving violation can increase car insurance rates in Memphis. The exact increase in insurance rates depends on factors such as the speed, the location of the violation, and the driver's history of speeding tickets. Memphis drivers with a speeding ticket pay an average of $298 per month for full coverage.

Some of the most affordable car insurance companies in Memphis include USAA, State Farm, Auto-Owners Insurance, GEICO, and Travelers.