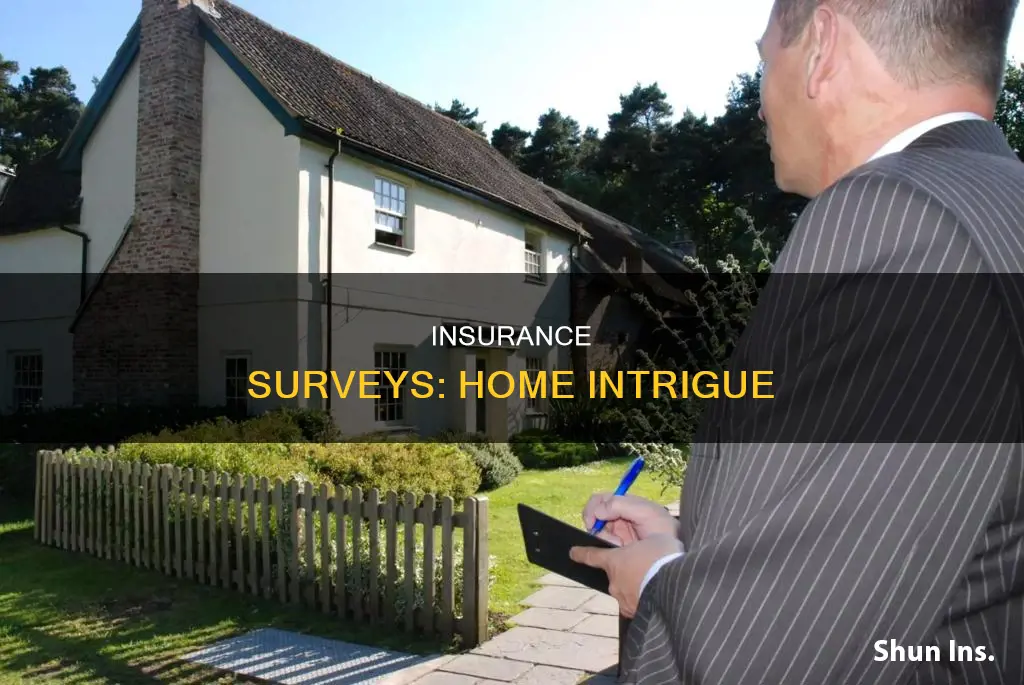

There are many reasons why an insurance company may want to survey your house. It could be because you're buying a new house, switching insurance companies, or haven't had an inspection in a long time. The insurance company wants to assess the risk of insuring your home and make sure there are no major liability hazards or maintenance concerns. The inspection will typically focus on the HVAC, plumbing, and electrical systems, as well as safety measures such as smoke detectors and fire extinguishers. While it may seem intrusive, the inspection is done to protect you and save you hassle and money in the long run.

| Characteristics | Values |

|---|---|

| Reason for insurance survey | To assess the risk of insuring your home |

| Type of survey | Exterior, interior, or both |

| Focus of survey | HVAC system, plumbing system, electrical system, safety measures |

| Time of survey | A few weeks after the insurance policy starts |

| Inspector's qualifications | Highly-skilled professionals trained to detect flaws and dangers |

| Factors for assessment | Size, location, and age of the house |

| Notice before survey | May or may not be given |

| Cost of survey | $300 to $500 |

Explore related products

$15.95 $15.95

$12.82 $16.95

What You'll Learn

![]()

To assess the risk of insuring your home

Insurance companies assess the risk of insuring your home to determine the likelihood of future claims. This is done through a home insurance inspection, which is often carried out by a third-party surveying firm. The inspection assesses the home's structure and appliances to help determine risk. For example, they may look for missing handrails, deteriorated roofs, or debris in the yard that could pose a fire risk. The inspection helps the insurance company decide whether to offer coverage, adjust premiums, or deny coverage if the home is too risky to insure.

Home insurance inspections are typically triggered by new home purchases, recent renovations, switching insurance providers, or the age of the home. Inspections are also more common in areas prone to natural disasters, such as hurricanes, tornadoes, or wildfires. The inspection may be exterior-only or include the interior of the home, depending on the insurance company's requirements.

During the inspection, the homeowner may be present and can address any issues or concerns. If problems are found, the insurance company may give a deadline for fixes to be made to continue coverage. Alternatively, the insurance company may cancel the policy if the home is deemed too risky. In such cases, the homeowner will need to find another insurance provider or explore state-sponsored programs for high-risk homes.

While home insurance inspections are not always legally required, they are an essential part of the insurance company's risk assessment process. By conducting these inspections, insurance companies can adjust their coverage and premiums accordingly, ensuring that the home is adequately protected in the event of a major loss.

Farmers Insurance: Uncovering the Headquarters and its Address

You may want to see also

Explore related products

![]()

To appraise the replacement cost of your home

The replacement cost of your home is the amount it would take to rebuild your home to its original standard. This is an important figure for insurance companies, as it is the amount they will pay out in the event of a total loss.

There are several ways to calculate the replacement cost of your home. You can use an online replacement cost calculator, which will take your location and square footage into account. However, this method may not be entirely accurate, as it does not consider the unique features of your home.

For a more precise estimate, you can hire a professional appraiser to assess your property. They will inspect your home, taking into account factors such as the type of roofing and flooring, interior and exterior features, and local building costs. This method will give you a more detailed understanding of the replacement cost of your home.

It is essential to ensure that your home is adequately insured. Underinsurance is a common issue, with around 60% of homes in the United States not carrying enough coverage to properly replace or repair their homes. To avoid this, review your replacement cost regularly and consider adding extended replacement cost coverage to your policy. This will help account for inflation and rising labour and material costs.

Additionally, keep your insurance company informed about any home improvements or additions, as these can increase your home's replacement value. By proactively managing your insurance coverage, you can ensure that your home is sufficiently protected in the event of a disaster.

Insuring Your VT Renovation

You may want to see also

Explore related products

![]()

To address any pre-existing risks

Insurance companies conduct surveys to identify pre-existing risks and hazards that may impact a property and business. This allows them to understand their exposure to different types of risks and decide whether these fall within their risk appetite.

Pre-risk surveys are crucial for underwriters to determine the frequency and severity of a given risk, allowing them to set adequate terms and conditions for insurance coverage. The surveyors will inspect the property, document its condition, and assess critical systems and components to identify any risks associated with their operation and maintenance.

There are several types of insurance risk surveys:

- Liability (or casualty) surveys: These focus on health and safety issues that may arise from business operations, assessing potential risks to employees, customers, and visitors.

- Property surveys: These concentrate on fire and security issues, examining construction, fire protection systems, and security measures.

- Business Interruption surveys: These evaluate how a disaster might affect business operations and the steps needed for successful recovery.

Insurance companies may request a survey when you are buying a new house or switching to a different insurance company. They will look for any maintenance concerns or liability hazards, such as missing handrails, deteriorated roofs, or excess debris in the yard, which could lead to claims or lawsuits.

By addressing pre-existing risks through surveys, insurance companies can provide better protection to their clients and help them save money in the long run.

**Lucrative Rewards at the Farmers Insurance Open: Unveiling the Prize Money**

You may want to see also

Explore related products

![]()

To ensure the insurance coverage is sufficient

Insurance companies may want to survey your house to ensure that your coverage is sufficient. This can happen if you are buying a new house, switching your home insurance provider, or if your current insurance company wants to check in on your property after a certain number of years.

These surveys are typically done to ensure that the property is maintained and that there are no major liability hazards or maintenance concerns. For example, insurance companies might be looking for missing handrails on steps, missing steps off sliding doors, excess debris in the yard, deteriorated roofs, boarded windows, or rundown detached structures. They might also be checking to see if you have a swimming pool, trampoline, dogs, or a wood stove.

Insurance companies may also want to survey your house to update their files, ensure that you are not over or under-insured, or to check for any obvious safety issues. For example, they might want to determine the measurements of your house, the type of wiring and plumbing, or the presence of any safety hazards.

By conducting these surveys, insurance companies can ensure that your coverage is sufficient and that you are not at risk of being underinsured. This helps to protect you and save you money in the long run.

Farmer's Insurance House Value Calculation

You may want to see also

Explore related products

![]()

To check for potential red flags

Insurance companies may want to survey your house to check for potential red flags that could lead to claims or lawsuits. These red flags could increase your insurance premiums or even result in the cancellation of your policy. Here are some common issues that insurance companies may look for during a house survey:

- Structural damage: This includes issues such as missing handrails on steps, missing steps off sliding glass or exterior doors, deteriorated roofs, boarded windows, or missing siding. Structural damage can affect the safety and integrity of your home, leading to potential liability hazards.

- Fire hazards: Insurance companies may be concerned about fire hazards, especially if you live in an area prone to wildfires or close to flammable hills. They may look for excess debris in your yard, deteriorated roofs, or other potential fire risks.

- Liability hazards: Insurance companies want to ensure that your property is safe and does not pose any liability hazards. They may check for missing handrails, missing steps, or other potential dangers that could lead to accidents or injuries.

- Maintenance concerns: Insurance companies want to make sure that your property is well-maintained to reduce the risk of future claims. They may look for issues such as deteriorated roofs, boarded windows, rundown detached structures, or excess debris in the yard.

- Unapproved extensions or additions: If you have made any extensions or additions to your home without the proper approvals or permits, this could be a red flag for insurance companies. Unapproved work may not meet building regulations or safety standards, leading to potential hazards or liability issues.

- Swimming pools, trampolines, or other hazardous features: Insurance companies may want to know about any features on your property that could increase the risk of accidents or injuries, such as swimming pools, trampolines, or wood stoves. These features may result in higher insurance premiums or additional coverage requirements.

It's important to note that insurance companies have a valid reason for conducting house surveys and that their primary goal is to identify potential risks and ensure that your property is adequately covered. While it may be inconvenient, allowing access for a house survey can ultimately help protect you and your home in the long run.

Insurance Dropped: Your Action Plan

You may want to see also

Frequently asked questions

Insurance companies will sometimes survey houses to assess the risk of insuring the home and determine insurance premiums. This can be done by driving past the house or through a physical visit.

The inspectors are highly-skilled professionals who can detect flaws and dangers. They will be looking for potential red flags, such as signs of water damage, faulty security systems, and fire hazards.

Home insurance inspections are usually carried out 30-90 days after the commencement of a new insurance policy or the renewal of an existing one. They are not always essential, but most companies will require an inspection at the insurer's discretion.

It is not advisable to refuse the inspector entry as the insurance company may cancel your policy or not renew it.