There are many reasons why your monthly insurance payments may be high. Firstly, insurance companies consider your risk level when determining your premium. Factors such as your age, driving record, location, vehicle, credit score, gender, and marital status can influence your premium. Additionally, market changes, including increases in natural disasters, accidents, inflation, and supply chain issues, have contributed to rising insurance rates. Furthermore, insurance companies may offer discounts or bundle policies to provide some financial relief. It's important to note that insurance rates vary across states due to different minimum coverage requirements. Understanding these factors can help you identify ways to lower your insurance costs.

| Characteristics | Values |

|---|---|

| Age | Younger, less experienced drivers tend to pay higher insurance rates because they are considered more likely to have an accident than older motorists. |

| Gender | Some insurers charge women higher premiums than men when all other factors are equal. |

| Credit score | A higher credit score may result in lower insurance premiums. |

| Driving record | A history of accidents, a DUI, or other instances of poor behavior on the road will increase insurance rates. |

| Job | Certain jobs that require long commutes or many hours on the road may result in higher insurance rates. |

| Location | Insurance rates can vary depending on the state, metro, and ZIP code due to factors such as minimum coverage requirements, claim frequency, and weather patterns. |

| Vehicle | More expensive or high-risk vehicles may lead to higher insurance rates. |

| Claims history | A higher number of claims in an area, due to extreme weather damage, accidents, or other factors, can increase insurance rates. |

| Market changes | The increase in natural disasters, accidents, inflation, and supply chain issues have contributed to higher insurance rates. |

| Coverage requirements | Different states have varying minimum coverage requirements, which can impact the cost of insurance. |

Explore related products

What You'll Learn

![]()

Age and experience

In addition to age, insurance companies also consider driving experience when determining premiums. New teenage drivers, due to their lack of experience, are statistically more likely to be involved in accidents, leading to higher insurance rates. On the other hand, elderly drivers, particularly those over 80, may also face higher insurance costs as they are considered to be at a higher risk of accidents. However, it is important to note that some states, such as Hawaii and Massachusetts, do not allow age to be used as a rating factor, resulting in similar rates for different age groups.

While age and experience play a crucial role in insurance pricing, it is just one of many factors that insurance companies consider. Other factors include gender, marital status, education level, credit score, driving record, vehicle type, and location. These factors collectively contribute to the overall risk assessment of an individual, which directly impacts the insurance premium.

To lower insurance costs, individuals can consider various options. Maintaining a clean driving record, free of traffic violations and accidents, is one of the most effective ways to reduce premiums. Additionally, improving one's credit score, bundling insurance policies (e.g., auto and home), increasing deductibles, and taking advantage of available discounts can all help reduce insurance costs. It is also beneficial to compare rates and seek quotes from multiple insurance providers to find the most suitable policy.

Michigan's New Auto Insurance Law: Effective Date and Changes

You may want to see also

Explore related products

![]()

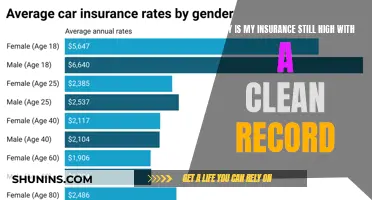

Gender

The impact of gender on insurance costs varies depending on the type of insurance in question.

Life Insurance

Observations since at least 1880 have shown that men tend to die earlier than women due to genetics and hormones. This means that life insurance companies will set higher rates for men because women live longer. Women will therefore pay lower premiums for longer. According to U.S. Census Bureau data, the projected life expectancy for a male born in 2010 is 75.6 years, while that of a woman is 81.4 years. This means that a woman will be paying premiums for about six years longer than a man. Consequently, women's life insurance premiums are lower.

Auto Insurance

Historically, men have paid more for car insurance than women because insurance companies view them as a higher risk to cover. Men are more likely to be involved in accidents, not wear their seatbelts, and drive dangerously. However, this is not the case for older drivers. Beyond the age of 60, rates for male drivers tend to be somewhat more expensive.

Some U.S. states, such as California, Hawaii, Massachusetts, Michigan, Montana, North Carolina, and Pennsylvania, have banned the use of gender as a factor in auto insurance rates. In these states, young male drivers will not be charged a higher premium than their female counterparts.

Health Insurance

Affordable Care Act (ACA)-compliant plans sold through state exchanges and the federal marketplace cannot use gender as a factor in setting premiums. However, short-term health insurance plans can and often do charge women significantly higher premiums than men. This is because medical costs during childbearing years are more than 45% higher than those for people who cannot give birth of the same age, and the difference can be as much as 270% when including birthing costs. Before the ACA, women buying insurance on the individual market were routinely charged up to 80% more for monthly premiums than men.

Learner Driver Insurance: Am I Covered?

You may want to see also

Explore related products

![]()

Education and profession

The cost of car insurance is influenced by a variety of factors, including age, gender, driving record, location, and credit score. However, education and profession can also play a significant role in determining insurance rates.

Education

Insurance companies have been known to use education level as a factor when calculating car insurance quotes. In general, drivers with higher education levels tend to pay less for car insurance. This is because insurers believe that highly educated people tend to file fewer claims. Additionally, having a college degree can lead to higher-paying jobs, resulting in increased financial stability and a lower risk of missing car insurance payments.

However, the practice of using education level to set insurance prices has been controversial. Critics argue that it disproportionately affects individuals from marginalized communities and lower-income backgrounds, who may have less access to higher education. As a result, some states are moving away from allowing education level to be considered in insurance pricing.

Profession

An individual's profession can also impact their car insurance rates. Certain occupations are associated with a higher likelihood of filing insurance claims, resulting in higher premiums for those in those professions. For example, service industry jobs or blue-collar jobs may be subject to higher rates than managerial or executive positions.

Similar to the debate surrounding education, the use of occupation in setting car insurance rates has been challenged by consumer advocates. They argue that it effectively considers factors such as race and income, which insurance companies are generally barred from using directly when setting rates.

It is worth noting that insurance companies vary in the weight they give to education and profession when determining premiums. Some companies offer discounts for higher education, while others may place less emphasis on education and profession, focusing more on other factors. Shopping around and comparing rates from multiple providers can help individuals find the most favourable rates.

GEICO Auto Insurance: Is a VIN Number Necessary?

You may want to see also

Explore related products

![]()

Marital status and location

Insurance companies generally charge lower rates for married drivers than for those who are single, separated, divorced, or widowed. This is because, statistically, married people tend to file fewer claims.

Your location can also impact your insurance rates. If you live in an area with a high rate of theft, accidents, or weather-related claims, insurance companies may consider you a higher risk to insure, leading to increased premiums. This can be true even if you have a perfect driving record. Additionally, insurance premium averages can vary by state, metro, and ZIP code due to factors like minimum coverage requirements, claim frequency, and weather patterns. For example, states with higher minimum coverage requirements will likely result in higher insurance rates for their residents.

The Chevy Cruze: Why Auto Insurance is Expensive

You may want to see also

Explore related products

![]()

Claims history

When it comes to insurance, the past is often used to determine the future. Insurance providers consider your claims history to be a significant factor in calculating your premium. The more claims you make, the higher your risk profile, which typically results in higher insurance premiums.

Each insurance claim you make will likely impact your insurance, but it's hard to determine the exact effect. Insurance companies will consider the nature and costliness of the claims filed, so not all claims will have the same impact. For example, a dog bite claim is likely to have a significant impact, with some carriers disqualifying you and others limiting liability. In contrast, a weather-related damage claim is likely to impact your premiums less than claims involving driver fault.

The size of the claim also matters. A $30,000 claim will likely affect your rate more than a $5,000 claim. Additionally, the type of claim matters, as different types of claims signal different kinds of risk. For instance, a fire claim may be viewed differently by your insurer than a home break-in.

How recently you've made a claim also affects your premium. The longer the time since your last claim, the lower the bearing it will have on your premium. Most claims will stay on your record for around three to seven years, after which your rate should begin to level out.

While it's essential to consider your claims history, other factors can also impact your insurance premium. These include your age, driving record, location, and the model of your car. Additionally, factors outside your control, such as increased claims in your area due to extreme weather damage or accidents, can also contribute to higher premiums.

Insuring Homes Held in Trust: Unraveling the Complexities for Auto Owners

You may want to see also

Frequently asked questions

There is no one-size-fits-all answer to this question. Many factors influence the price you pay for insurance, such as:

- Your age: Younger, less experienced drivers tend to pay higher insurance rates because they are considered more likely to have an accident than older motorists.

- Your driving record: If you have a history of accidents, a DUI, or other instances of poor behaviour on the road, your rates will go up.

- Your location: If your area has a high rate of theft, accident, or weather-related claims, it becomes riskier for an insurance company to cover drivers there.

Other reasons include:

- Your marital status: Most large auto insurance companies have lower rates for married drivers than for those who are single, separated, divorced or widowed.

- Your job: Certain jobs that require long commutes or many hours on the road can drive rates up.

- Your vehicle: If you purchase a more expensive car, your rate is likely to go up as your new ride may be more likely to be stolen and cost more to repair or replace than your previous vehicle.

Here are some ways to lower your insurance costs:

- Ask your insurer about discounts: Some common discounts include being a homeowner, going paperless, and bundling home and auto policies.

- Improve your credit score: Having a higher credit score may result in lower insurance premiums.

- Compare insurance providers: Request quotes from several insurers to see whether you can find a similar policy for less.