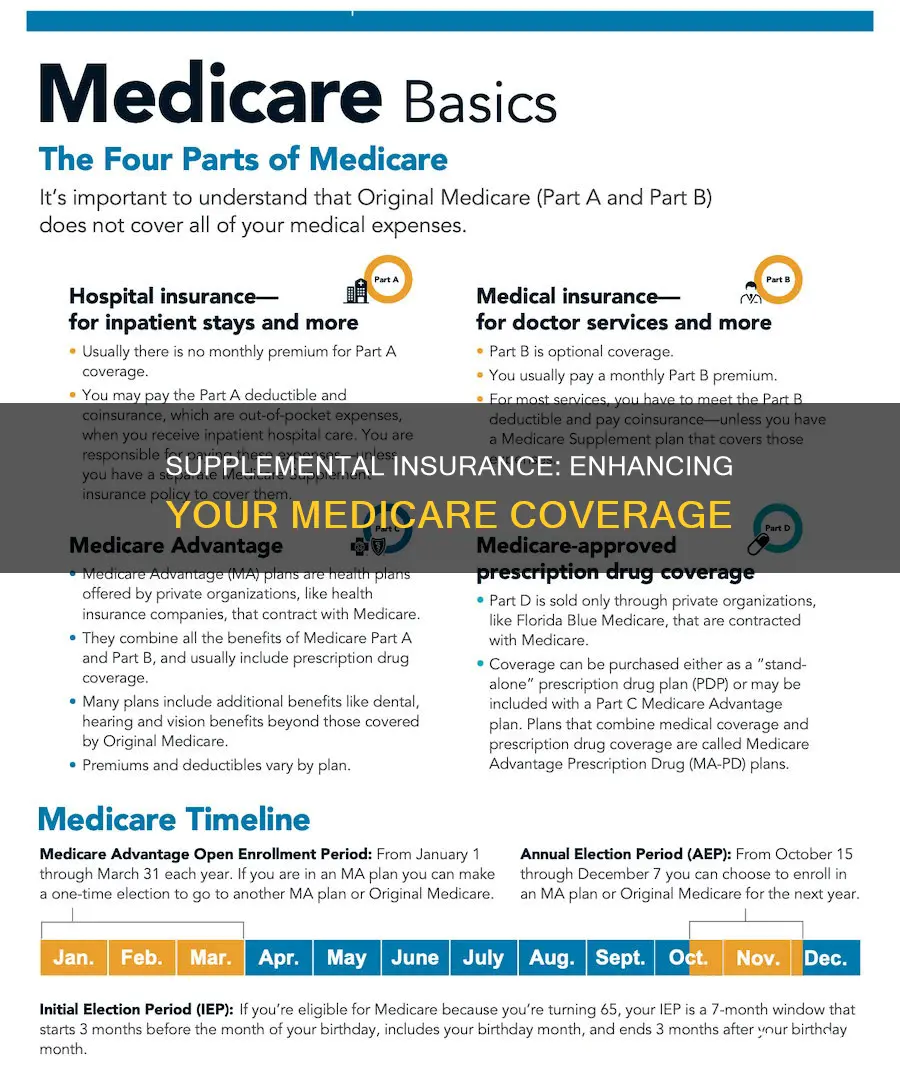

Medicare is a federal health insurance program that covers most healthcare costs for people aged 65 and over, as well as some people under 65 with disabilities. While Medicare covers a large share of healthcare costs, it does not cover everything, and there are gaps in the coverage that can result in high out-of-pocket expenses for beneficiaries. This is where Medicare Supplemental Insurance, also known as Medigap, comes in. Medigap is an optional add-on that can help fill these coverage gaps and protect against unexpected costs. It is important to note that Medigap policies do not cover long-term care, vision, dental, hearing aids, private-duty nursing, or prescription drugs. However, they can provide valuable financial protection for deductibles, coinsurance, and other medical expenses not fully covered by Medicare.

| Characteristics | Values |

|---|---|

| What is Medicare Supplemental Insurance? | Extra insurance bought from a private health insurance company to help pay out-of-pocket costs in Original Medicare. |

| Who is eligible? | Anyone who has Medicare Part A and Part B. |

| When is the best time to buy a Medigap policy? | When you turn 65 and are enrolled in Medicare Part B. |

| What are the benefits? | Fills "gaps" in Medicare Part A and Part B, covers deductibles, coinsurance, and other medical expenses not fully covered by Medicare, some policies offer coverage when travelling outside the U.S. |

| What is not covered? | Long-term care, vision, dental, hearing aids, private-duty nursing, or prescription drugs. |

| What are the costs? | You will have to pay a monthly premium to the Medigap insurance company in addition to the monthly Medicare Part B premium. |

Explore related products

What You'll Learn

![]()

Fills gaps in Medicare Part A and Part B

Medicare Supplement Insurance, also known as Medigap, is an optional add-on that fills the "gaps" in Medicare Part A and Part B. It is extra insurance that can be purchased from a private health insurance company to help pay for out-of-pocket costs in Original Medicare, which includes Part A (Hospital Insurance) and Part B (Medical Insurance).

Medicare Part A covers hospital services, while Part B covers other types of medical expenses. However, there are certain costs associated with these services that Medicare does not cover, leaving beneficiaries responsible for paying these out-of-pocket costs. For example, Medicare Part A has a deductible of $1,632 in 2024, which must be paid before Medicare starts paying for inpatient hospital care.

Medigap policies help to fill these gaps in coverage by paying for deductibles, coinsurance, and other out-of-pocket costs that Medicare does not cover. By purchasing a Medigap policy, individuals can protect themselves from unexpectedly high out-of-pocket costs. It is important to note that Medigap policies do not cover long-term care, vision, dental, hearing aids, private-duty nursing, or prescription drugs.

To purchase a Medigap policy, individuals must generally have both Medicare Part A and Part B. The best time to buy a Medigap policy is when an individual turns 65 and enrolls in Medicare Part B, as there is a six-month Medigap open enrollment period during which insurance companies cannot use medical underwriting to charge higher premiums or deny coverage based on health history. During this period, individuals can choose from standardized Medigap plans, which offer the same benefits regardless of the insurance company selling them, with price being the only differentiating factor.

Get Medical Insurance in Florida: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Covers deductibles, coinsurance and out-of-pocket costs

Medicare Supplement Insurance, also known as Medigap, is an optional add-on that can fill the "gaps" in Medicare Part A and Part B. Medigap is extra insurance that can be purchased from a private health insurance company to help pay for out-of-pocket costs in Original Medicare. It covers deductibles, coinsurance, and other out-of-pocket expenses that Medicare does not cover.

Medigap policies are designed to help with the costs that Original Medicare does not fully cover. For example, Medicare Part A has a deductible of $1,632 in 2024, which must be paid before Medicare starts paying for inpatient hospital care. Medigap policies can help cover this deductible, as well as coinsurance and other out-of-pocket costs.

By purchasing a Medigap policy, individuals can protect themselves from unexpectedly high out-of-pocket costs. These policies are particularly useful for those who may have frequent or unexpected medical expenses that are only partially covered by Original Medicare. While Medigap is not mandatory, it can provide financial peace of mind and help individuals manage their healthcare expenses more effectively.

It is important to note that Medigap policies do not cover all expenses. They typically do not cover long-term care, vision, dental, hearing aids, private-duty nursing, or prescription drugs. However, some Medigap policies may offer additional benefits, such as coverage for health care during foreign travel. Therefore, it is essential to carefully review the terms of the Medigap policy to understand what is and is not covered.

The best time to purchase a Medigap policy is when individuals first turn 65 and enroll in Medicare Part B. During this six-month Medigap open enrollment period, insurance companies cannot use medical underwriting to charge higher premiums or deny coverage based on health history. This guarantees acceptance into a Medigap policy, regardless of any pre-existing conditions.

Understanding Medical Insurance Premiums: What's the Average Cost?

You may want to see also

Explore related products

![]()

Offers financial protection for unexpected costs

Medicare is a federal health insurance program that covers most healthcare costs for people aged 65 and over. It also covers healthcare for some people under 65 with disabilities. However, Medicare has some "gaps" that could be costly. This is where Medicare Supplemental Insurance, or Medigap, comes in. It is an optional add-on that can fill these gaps in Medicare Part A and Part B.

Medigap is extra insurance that you can buy from a private health insurance company to help pay your share of out-of-pocket costs in Original Medicare. It covers deductibles, coinsurance, and other medical expenses not fully covered by Medicare. For example, some Medigap policies offer coverage when you travel outside the U.S. Additionally, Medigap policies cover other extra benefits that aren't covered by Medicare, such as durable medical equipment and supplies.

Medigap eligibility starts at 65, with guaranteed acceptance. When you turn 65 and enroll in Medicare Part B, you have a six-month Medigap open enrollment period. During this time, insurance companies cannot use medical underwriting to charge you more or deny coverage based on your health or medical history. After the open enrollment period, you can still try to sign up for a policy, but the insurance company may ask about your health and increase the premium or even deny you a policy if you have pre-existing conditions.

While it is not mandatory to purchase Medigap, it is a good idea to consider it, especially if you can afford it. It offers financial protection against unexpectedly high out-of-pocket costs. Without Medigap, you could be on the hook for thousands of dollars in unexpected medical expenses. Therefore, if you have Original Medicare and can afford Medigap, it is recommended to purchase a Medigap policy to protect yourself from potential financial strain due to medical costs.

Valley Medical Center: Insurance Coverage and Acceptance

You may want to see also

Explore related products

![]()

Provides extra benefits not covered by Medicare

Medicare is a federal health insurance program that covers most health care costs for people aged 65 and over. It also covers healthcare for some people under 65 who have disabilities. Medicare has two parts: Part A (Hospital Insurance) and Part B (Medical Insurance).

Medicare Supplement Insurance, also known as Medigap, is extra insurance that can be purchased from a private health insurance company to help pay for out-of-pocket costs that Original Medicare does not cover. This includes costs associated with care in a skilled nursing facility after a hospital stay, home health care, durable medical equipment, and preventive health services like exams and health screenings.

Medigap policies can also provide coverage for certain services that Original Medicare does not cover, such as emergency medical care when travelling outside the US (foreign travel emergency care). This is an especially useful benefit for those who travel frequently or plan to retire abroad. Additionally, some Medigap plans may offer extra benefits such as vision, hearing, and dental services, which are not typically covered by Original Medicare.

It is important to note that Medigap policies generally do not cover long-term care, such as extended stays in a nursing home, private-duty nursing, or prescription drugs. However, if you require prescription drug coverage, you can enrol in a separate Medicare drug plan (Part D).

Palo Alto Medical Foundation: Insurance Plans and Coverage

You may want to see also

Explore related products

![]()

Protects against high out-of-pocket costs

Medicare Supplement Insurance, also known as Medigap, is an optional add-on that can fill the "gaps" in Medicare Part A and Part B. It is extra insurance that can be purchased from a private health insurance company to help pay for out-of-pocket costs that Original Medicare does not cover. These out-of-pocket costs can add up to thousands of dollars per year, so Medigap helps protect against high expenses.

Medicare Part A covers hospital services, while Part B covers other types of medical expenses. However, there are gaps in this coverage, and Medicare does not pay for everything. For example, Medicare Part A has a deductible of $1,632 in 2024, which must be paid before Medicare starts paying for inpatient hospital care. Medigap policies can help cover these deductibles, as well as coinsurance and other out-of-pocket costs, according to the policy terms.

It is important to note that Medigap policies do not cover long-term care, such as care in a nursing home, vision, dental, hearing aids, or private-duty nursing. They also do not cover prescription drugs. If an individual requires insurance for prescriptions, they can purchase an additional Medicare Part D plan. Additionally, Medigap policies are generally only available to those who have Original Medicare Part A and Part B.

The best time to purchase a Medigap policy is when an individual turns 65 and enrolls in Medicare Part B. During this six-month Medigap open enrollment period, insurance companies cannot use medical underwriting to charge higher premiums or deny coverage based on health history. After this period, insurance companies may ask about health and medical history and can increase premiums or deny coverage for pre-existing conditions.

In summary, Medicare Supplement Insurance (Medigap) is a valuable option for individuals with Original Medicare to protect against high out-of-pocket costs. It fills the gaps in Medicare Part A and Part B coverage, helping to cover deductibles, coinsurance, and other expenses. However, it is important to understand the limitations of Medigap policies and to compare plans from different insurance companies to find the best coverage for one's needs.

Travel Insurance: Medical Records and Their Importance

You may want to see also

Frequently asked questions

Medicare Supplement Insurance, also known as Medigap, is extra insurance that can be purchased from a private health insurance company to help pay for out-of-pocket costs in Original Medicare.

Medicare Supplement Insurance helps to fill the "gaps" in Medicare Part A and Part B, which could otherwise result in costly expenses. It offers financial protection for deductibles, coinsurance, and other medical expenses not fully covered by Medicare.

The best time to buy a Medicare Supplement Insurance policy is when you turn 65 and enroll in Medicare Part B. During this six-month Medigap open enrollment period, insurance companies cannot use medical underwriting to charge higher premiums or deny coverage based on health history.

Medicare Supplement Insurance helps cover out-of-pocket costs such as deductibles, coinsurance, and other expenses not fully covered by Original Medicare. Some Medigap policies also offer coverage for additional benefits, like healthcare during foreign travel. However, they typically do not cover prescription drugs, long-term care, vision, dental, hearing aids, or private-duty nursing.

To choose a Medicare Supplement Insurance plan, it is important to compare policies from different companies, as costs can vary. Medigap policies are standardized, with plans labelled with letters indicating the benefits included. The benefits are the same across insurance companies, with price being the main differentiating factor.