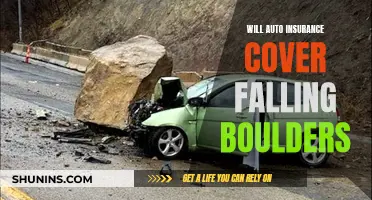

If you're wondering whether your auto insurance will cover damage to your car from a rock slide, the answer depends on your specific insurance policy and coverage. In general, car insurance does cover damage caused by road hazards, which can include rocks or other objects on the road. However, it's important to distinguish between collision and comprehensive insurance claims. If you hit a rock on the road, it's typically considered a collision claim, while if a rock falls onto your car, it's usually covered by comprehensive insurance. It's worth noting that comprehensive insurance generally doesn't raise your rates, but collision insurance claims often do. Additionally, if the cost of repairs is minimal, it might be more cost-effective to pay out of pocket rather than filing a claim, depending on your deductible. Keep in mind that standard homeowners insurance typically excludes coverage for movements of the earth, which includes landslides and mudslides. To insure against these events, you may need to purchase separate difference in conditions (DIC) coverage.

| Characteristics | Values |

|---|---|

| Will auto insurance cover a rock slide? | It depends on the type of insurance |

| Types of insurance that cover rock slides | Full Coverage Car Insurance, Collision Insurance, Comprehensive Insurance |

| Types of insurance that do not cover rock slides | Liability-Only Car Insurance |

Explore related products

What You'll Learn

![]()

Collision insurance covers objects hitting your car

If you're wondering whether your auto insurance will cover a rock slide, the answer depends on the type of insurance you have. Collision insurance, for example, covers a wide range of incidents, including objects hitting your car.

Collision insurance is a type of auto insurance that covers the cost of repairs to your vehicle if it collides with another vehicle or object. It applies whether you are at fault or not and can be used to cover accidents involving only your car, such as rollovers, as well as accidents with other vehicles or objects, like a phone pole or fence. It's important to note that collision insurance only reimburses you for damage to your car and not for any damage to other vehicles, objects, or bodily injuries. Additionally, it does not cover all types of damage to your vehicle, and each insurance company will have its own exclusions and limitations.

In the case of a rock slide, if rocks hit your car and cause damage, collision insurance would typically cover the cost of repairs. This is because collision insurance covers accidents involving objects, and a rock slide would fall under this category. However, it's important to review your specific policy and understand any exclusions or limitations that may apply.

It's worth noting that collision insurance is not required by law, but it is often a good idea to have it, especially if you drive frequently or in areas with high-volume traffic. If your car is leased or financed, your lender or lessor may require you to have collision insurance to protect their investment.

Comprehensive insurance is another type of auto insurance that covers non-accident incidents, such as theft, vandalism, flooding, and accidents with animals. In some cases, comprehensive insurance may also cover debris damage, depending on the source of the debris. For example, if a rock falls onto your vehicle and causes damage, comprehensive insurance may cover the repairs.

To ensure you have the right coverage in the event of a rock slide or other unexpected incidents, it's important to carefully review your insurance policy and understand the types of incidents and damages that are covered.

Competitive Auto Insurance Options Compared to Hartford

You may want to see also

Explore related products

![]()

Comprehensive insurance covers objects falling onto your car

If you're unfortunate enough to have an encounter with a rock slide, the damage to your car could be extensive. So, will your auto insurance cover this? The answer is yes, but only if you have comprehensive insurance.

It's important to note that comprehensive insurance covers a wide range of situations where your car is damaged by an object or force while it is parked. For example, it covers damage caused by natural disasters like hurricanes, floods, and earthquakes, as well as falling objects like trees or rocks. It also covers damage caused by animals, such as a deer colliding with your car, or a squirrel chewing through your wiring.

While comprehensive insurance does provide valuable protection, it's not always necessary. If you live in an area with a low risk of natural disasters or animal-related incidents, you may decide that the cost of comprehensive coverage is not worth the benefit. Additionally, if the repairs to your car are minimal, it might be more cost-effective to pay for them out of pocket rather than filing a claim with your insurance provider, especially if the cost is below your deductible amount.

Ultimately, the decision to opt for comprehensive insurance depends on your individual circumstances, including the value of your car, the likelihood of it being damaged by a covered peril, and your financial situation. It's always a good idea to carefully review your insurance policy and understand what is and isn't covered, so you can make informed decisions about your coverage.

Auto Insurance and Relationships: Am I Covered if My Girlfriend Drives My Car?

You may want to see also

Explore related products

![]()

Home insurance doesn't cover landslides

Standard homeowners insurance does not cover landslides or mudslides. These are considered "movements of the earth", which are explicitly excluded from coverage. The rarity of landslides and the extensive damage they cause also make it difficult for insurance companies to offer coverage. The damage caused by a landslide can amount to serious structural problems in a home, and the average damage caused by landslides in the US is estimated to be $3 billion annually.

To insure your home against landslides, you will need to purchase a separate policy, known as a Difference in Conditions (DIC) or "gap coverage" policy. DIC policies cover perils that a standard insurance policy won't, including floods, earthquakes, and landslides. DIC coverage can be purchased as a standalone policy or as an endorsement from your current insurance provider. The cost of DIC coverage is typically a few hundred dollars more than standard homeowners insurance.

If you live in an area prone to landslides, it may be worthwhile to invest in DIC coverage. Landslides are more likely to occur in coastal and mountainous areas, and some states are more prone to severe landslides than others, including California, Oregon, and Washington.

It's important to note that mudslides are also not typically covered by homeowners insurance. However, if a mudslide is the result of an earthquake, your home may be covered if you have supplemental earthquake insurance on your homeowners policy.

Kansas Auto Insurance: Minimum Liability Requirements Explained

You may want to see also

Explore related products

![]()

DIC insurance covers landslides

Standard auto insurance policies may not cover damage from natural disasters such as rockslides or landslides. However, Difference in Conditions (DIC) insurance can provide coverage for such events.

DIC insurance is a type of policy that fills in the gaps in standard insurance coverage. It is designed to protect against catastrophic perils and is often used by larger organisations. DIC insurance is flexible and can be tailored to the needs of the policyholder. It can be purchased as an addition to a standard insurance policy or through a policy endorsement that provides similar coverage.

DIC insurance provides coverage for perils that are typically excluded from standard policies, such as floods and earthquakes. It can also be used to fill in coverage gaps between different types of policies, such as a contractor's policy and a project owner's policy. In the case of landslides, DIC insurance can provide coverage for property damage or other losses incurred.

Several insurers in the United States offer DIC policies, including the California Automobile Insurance Company (Mercury Insurance Group) and the California Capital Insurance Company. To obtain DIC insurance, it is recommended to discuss your specific needs with an insurance agent or broker, who can help determine if DIC insurance is necessary and provide options for obtaining the appropriate coverage.

Expedia's Auto Insurance: Worth the Detour?

You may want to see also

Explore related products

![360 Privacy for iPhone 16 Pro Max Screen Protector 2 Pack, [Auto Alignment Dust Free] Full Coverage Easy Install 4 Way Anti Spy Tempered Glass for Apple 16 Pro Max](https://m.media-amazon.com/images/I/71SGHoejPfL._AC_UL320_.jpg)

![]()

Flood insurance is needed for mudflow cover

If you're looking for auto insurance coverage for rockslides, it's important to note that this typically falls under comprehensive insurance. However, for homeowners, renters, and business owners, the story is a little different when it comes to natural disasters like mudflows and landslides.

Mudflows, which are different from mudslides, occur when heavy rainfall falls on land lacking adequate vegetation, turning soil into a river of mud that can cause significant and costly damage to properties. This is often the case after wildfires, where vegetation that once held the soil together has been destroyed.

To protect against mudflow damage, you will need to purchase flood insurance separately. Standard homeowners, renters, and business insurance policies do not cover mudflows. FEMA's National Flood Insurance Program (NFIP) offers flood insurance that includes mudflow coverage if it meets the general definition of flooding. Private insurance companies also offer this coverage.

It's important to note that there is usually a 30-day waiting period for NFIP policies to become effective, so those at risk of mudflows or flooding are encouraged to purchase insurance as soon as possible. Additionally, reviewing your policy carefully and understanding what it includes or excludes regarding land movement, flood, and rain is crucial.

In summary, while auto insurance may cover rockslide damage under comprehensive coverage, homeowners, renters, and business owners need to purchase separate flood insurance to ensure protection against mudflow damage, as it is not included in standard policies.

Auto Insurance: Is It Mandatory?

You may want to see also

Frequently asked questions

Auto insurance will cover damage to your vehicle from a rock slide, as long as you have the right coverage and it is over your deductible.

A rock slide is considered a "movement of the earth" and is typically excluded from standard homeowners insurance policies.

To protect your vehicle from a rock slide, you will need comprehensive insurance coverage, which covers incidents where an object hits your vehicle.

If you hit a rock on the road and it damages your car, this would typically be covered by collision insurance, which covers incidents where you collide with an object.

Yes, you may be able to purchase a separate policy, known as a difference in conditions (DIC) or "gap coverage" policy, which covers perils that a standard insurance policy doesn't, including movements of the earth like rock slides.

![For iPhone 17 Pro Max Privacy Screen Protector [Auto Dust Install] 6.9 inch Tempered Glass Full Coverage Anti-Blue Light Anti Spy No-Bubble Gradient Green Easy Installation[HD Clarity]](https://m.media-amazon.com/images/I/71BwbVowbZL._AC_UL320_.jpg)