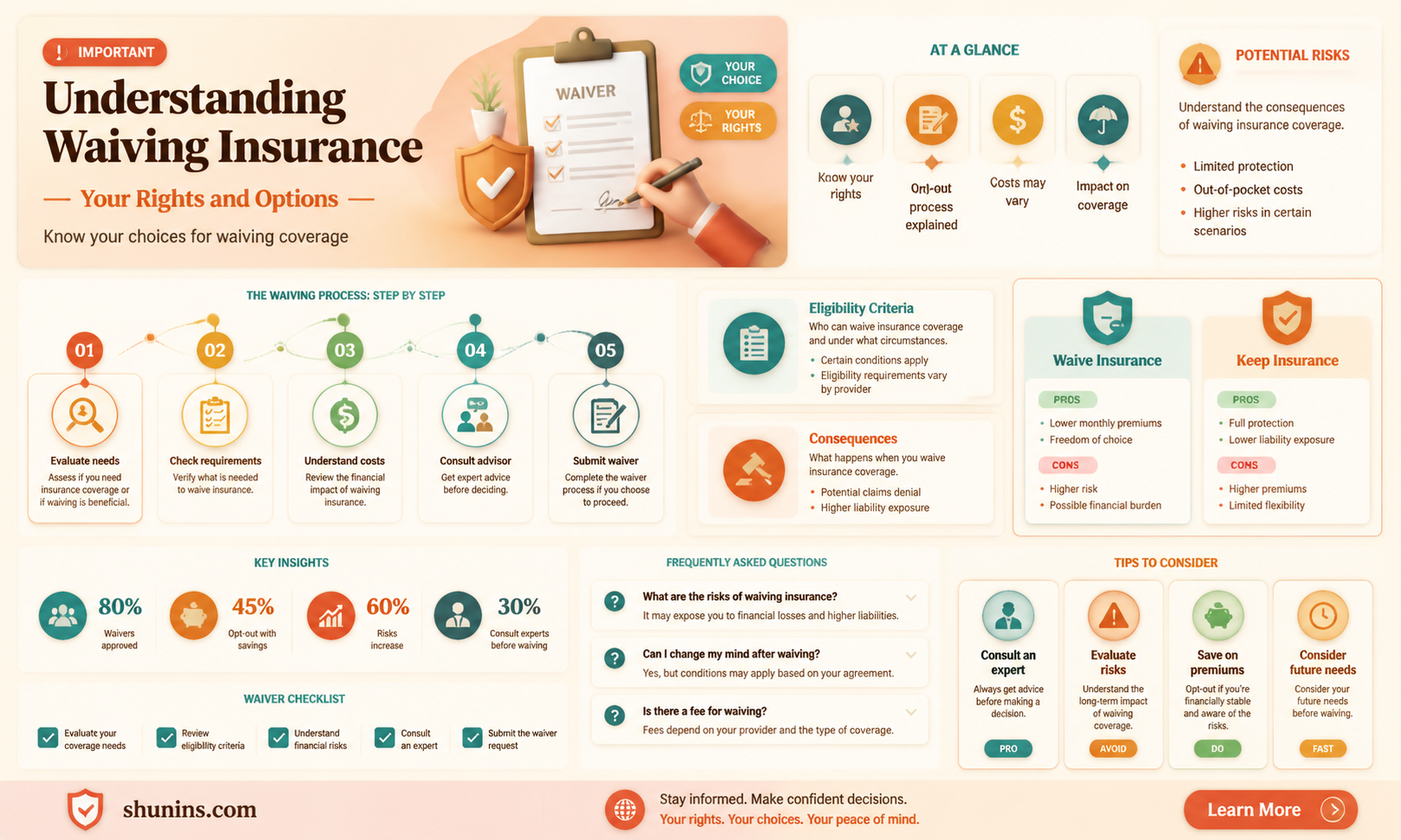

There are various scenarios in which someone might consider waiving their insurance. For example, a student may wish to waive their health insurance plan if they are already covered by their parent's insurance. Employees may also decline health insurance offered by employers, which is called a waiver of coverage. However, it is important to note that there may be consequences for doing so. For example, in 2014, employees who declined coverage under the Patient Protection and Affordable Care Act did not qualify for government subsidies to purchase individual health insurance. Additionally, if an employee waives coverage without having alternative insurance, they may be subject to a pre-existing condition limitation when they eventually enroll in an insurance plan.

Characteristics of Insurance Waiving

| Characteristics | Values |

|---|---|

| Who can waive insurance | Students, employees |

| Requirements | Proof of other insurance, employer plan through a US-based insurance company |

| Deadlines | Deadlines vary by institution and semester; typically before the start of the semester or year |

| Consequences | May save employer money, but will not result in a higher salary; may be subject to a penalty if not covered under another plan |

| Process | Online or paper forms; must be completed annually or before the deadline |

| Verification | Log back into the portal to check insurance status |

Explore related products

What You'll Learn

![]()

Students with existing coverage

If you are a student with existing health insurance coverage, you may not need to purchase additional insurance through your school. Many colleges and universities offer student health insurance plans (SHIP) that can provide basic, affordable coverage for students who need it. However, if you already have adequate coverage through a parent's plan, a private plan, or a government-sponsored program like Medicaid, you may be able to waive the school's insurance plan.

It's important to note that the requirements and processes for waiving student health insurance vary from school to school. Some schools may require you to complete a waiver form annually, while others may have different deadlines and requirements. It's essential to review your school's specific policies and procedures for waiving insurance coverage. This information is usually available on the website of your school's student health center or insurance office.

To waive your school's insurance plan, you will typically need to provide proof of your existing coverage. This may include presenting your current health insurance card or policy documents. In some cases, you may also need to demonstrate that your current coverage meets certain minimum requirements or standards set by the school. Additionally, international students on specific visa types may have different requirements for waiving school insurance, so it's important to review the regulations that apply to your specific situation.

If you decide to keep your existing coverage and waive your school's insurance, be sure to understand the benefits and limitations of your plan. Pay close attention to factors such as deductibles, copays, provider networks, and coverage for specific services or treatments. It's also a good idea to familiarize yourself with the rules and guidelines of your insurance plan to maximize your benefits and avoid unexpected costs. Additionally, consider the accessibility of your insurance plan in your school's location, as some plans may have limitations on out-of-network coverage.

While maintaining existing coverage may be a viable option for some students, it's important to periodically review your insurance needs. As a student, your healthcare requirements may change over time, and you may find that your existing plan no longer adequately meets your needs. In such cases, you can explore alternative options, such as enrolling in your school's SHIP or purchasing a separate health insurance plan that better suits your circumstances. Remember to stay informed about open enrollment periods and special enrollment periods, as these provide opportunities to adjust your insurance coverage as needed.

How to Turn Your Life Insurance into Cash

You may want to see also

Explore related products

$8.69

![]()

International students

At the University of Washington, F and J international students who are enrolled in classes are automatically registered for the International Student Health Insurance Plan (ISHIP). Students who meet certain eligibility criteria and have comparable insurance that is valid in the U.S. may be eligible for a waiver of enrollment in ISHIP.

At the University of Minnesota, international students are automatically enrolled in the Student Health Benefit Plan (SHBP) and are not eligible to waive out of it. However, eligible students can waive enrollment in the SHBP if they have other health insurance for the entire semester.

At Washington University in St. Louis, students who plan to enroll or remain enrolled in health insurance through a parent, spouse/partner, or employer that meets waiver requirements should use the UHC website to complete the insurance waiver process. Students with an F-1 or J-1 visa must ensure that their insurance policy offers medical evacuation and repatriation benefits.

At the University of Southern California, students with their own health insurance through a family member or other qualified plan can submit a waiver request via MySHR in the Insurance Waiver/Enrollment tab.

At Binghamton University, international students can submit a request to waive their international health insurance by completing an International Student Insurance Waiver e-form by October 15 for the fall semester and by February for the spring semester.

Life Insurance Post-Heart Attack: Is It Possible?

You may want to see also

Explore related products

![]()

Waiver deadlines

Waiving your insurance is a viable option if you already have qualifying health insurance from a parent, spouse/partner, or employer. However, it is important to be aware of the waiver deadlines to ensure you do not miss out on the opportunity to opt-out of insurance provided by your educational institution or employer.

For students at the University of Florida, the deadline for health insurance waivers is the fee payment deadline, and reminders are sent out via email and notifications. Students at WashU have a deadline of September 5 for the fall semester and February 12 for the spring semester. These deadlines are applicable for students on an F-1 or J-1 visa who are on a US-based employer plan.

In the context of employee insurance, there are various scenarios that impact waiver deadlines. For instance, if an employee gains a new dependent through birth, adoption, or marriage, they have 30 days to enroll themselves, the new dependent, and their family. Missing this deadline results in having to wait until open enrollment. Additionally, employees who decline coverage under the Patient Protection and Affordable Care Act will not qualify for government subsidies for individual health insurance.

It is important to note that insurance plans that are not filed or approved in the United States or compliant with the Affordable Care Act will not qualify for a waiver. Thus, it is essential to carefully review the requirements and deadlines for insurance waivers to make an informed decision about your insurance coverage.

Life Insurance Rates: Understanding Term Policy Price Hikes

You may want to see also

Explore related products

![]()

Waiver approval

For example, in the context of student health insurance, many universities require students to either enrol in their insurance plan or complete a waiver process to opt-out annually. This typically involves providing proof of alternative insurance coverage, and there may be specific deadlines that must be adhered to. International students on specific visas may have additional restrictions on their ability to waive university-provided insurance plans.

In the context of employee health insurance, offered through an employer, individuals may choose to waive their employer's insurance coverage, particularly if they have alternative coverage, such as through a spouse's plan or a parent's plan. However, it is important to carefully consider the consequences of waiving employer-provided insurance. In some cases, employees who decline coverage may not qualify for government subsidies to purchase individual insurance. Additionally, they may be subject to penalties if they do not obtain alternative coverage. It is also worth noting that waiving insurance may not result in a higher salary or direct monetary compensation.

To initiate the waiver approval process, individuals typically need to complete specific forms or online portals, providing details of their current insurance coverage. Deadlines for submitting waivers vary and may be annual or tied to specific events, such as the start of a new semester or employment. It is essential to review the requirements and instructions provided by the relevant institution or organisation carefully.

Once a waiver is submitted, it goes through a verification and approval process. After approval, any insurance premiums or charges associated with the waived plan should be removed from the individual's account. It is good practice to log back into the portal and check the insurance status to ensure the waiver has been successfully processed.

Life Insurance for Disabled People: Is It Possible?

You may want to see also

Explore related products

![]()

Pros and cons

Waiving insurance means that you are giving up your right to claim certain benefits and services that you would otherwise be entitled to. This can be done voluntarily or by meeting certain requirements. In the context of health insurance in the United States, individuals may choose to waive their employer-provided insurance if they are already covered by their parent's or spouse's insurance plan. Students in college may also waive their university's health insurance plan if they already have comparable coverage.

Pros of Waiving Insurance:

- Cost savings: If you are already covered by another insurance plan, such as your parent's or spouse's plan, waiving additional insurance can save you money on premiums or contributions.

- Simplicity and convenience: Managing multiple insurance plans can be complicated and time-consuming. Waiving one of the plans can simplify your life and reduce administrative burdens.

- Customization: If you choose to purchase your own insurance plan instead of accepting employer-provided insurance, you have the flexibility to choose a plan that better suits your specific needs and preferences.

Cons of Waiving Insurance:

- Limited coverage: By waiving insurance, you may lose access to certain benefits and services that were provided by the waived plan. It is important to carefully review the coverage offered by both plans to ensure you are not losing essential benefits.

- Dependence on others: If you are relying on someone else's insurance plan (e.g., your parent's plan), you may be dependent on their continued enrolment and coverage. Any changes to their plan or circumstances could affect your coverage.

- Missed opportunities: Insurance plans offered through employers or educational institutions often come with group rates or discounted prices. Waiving this coverage means forfeiting these potential savings.

- Administrative burden: Waiving insurance often requires submitting paperwork, providing proof of alternative coverage, and keeping track of deadlines. It can be a hassle to manage, especially if you need to repeat the process annually.

Service-Disabled Life Insurance: Applying for Peace of Mind

You may want to see also

Frequently asked questions

A health plan waiver is a way for students with existing insurance coverage to prove that their insurance meets legal requirements.

To waive your student health insurance, you must submit a waiver form and provide information about your current insurance coverage. Your waiver will be reviewed, and you will receive a response within a few business days confirming if it is approved, denied, or if additional information is needed.

To be eligible for a waiver, your current insurance plan must have comparable coverage to the student health insurance plan. This includes coverage for a comprehensive set of services such as preventative and primary care, doctor visits, hospital admissions, surgical services, emergency services, mental health, and prescription drugs.

Yes, there are typically deadlines for submitting health insurance waivers. These deadlines vary depending on the school and the semester. It is important to check with your specific institution to determine the deadline for submitting a waiver.

International students with comparable health insurance coverage may be allowed to waive their school's health insurance plan. However, this may vary depending on the student's visa status and the specific requirements of the school.