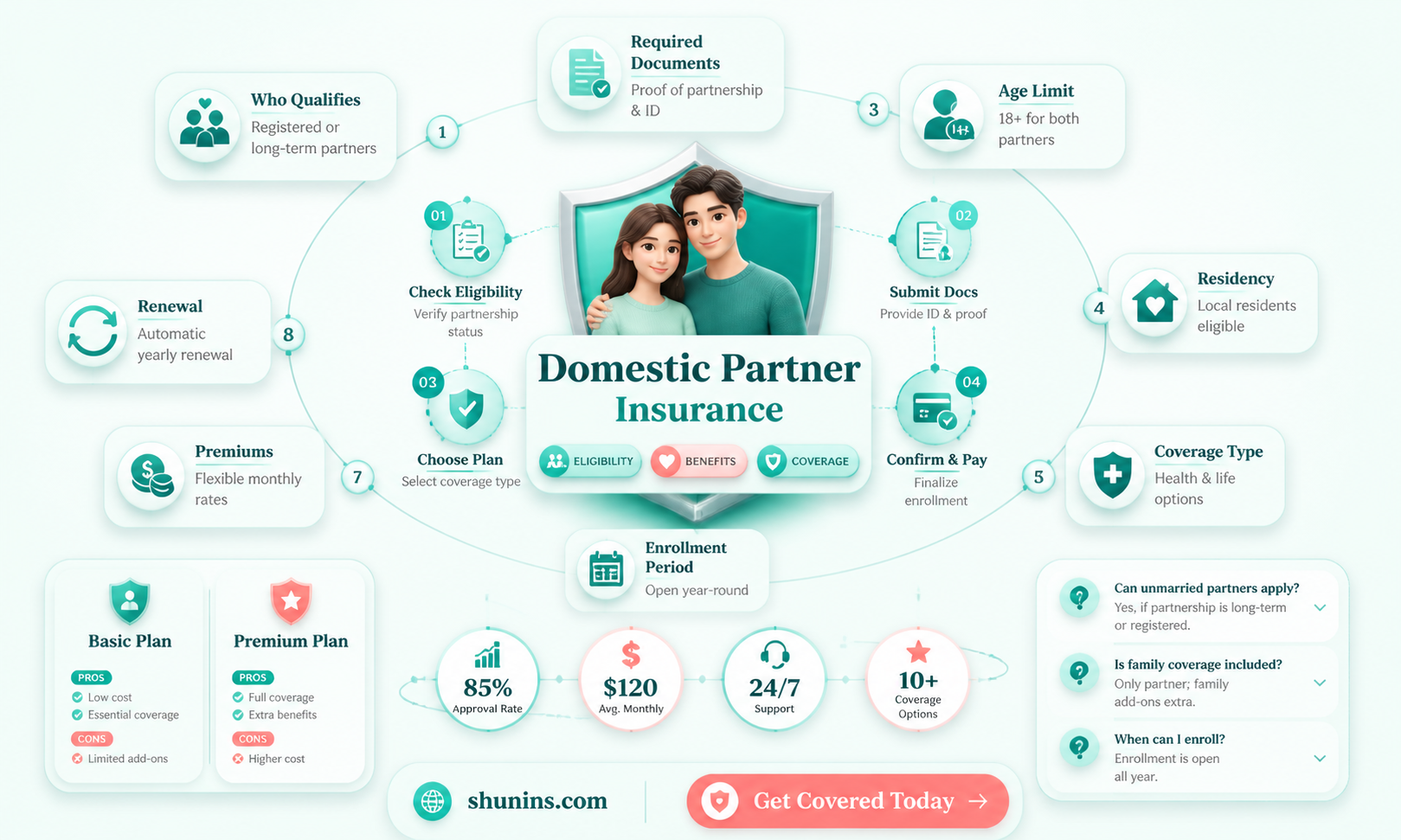

Domestic partner health insurance is an option for those who are not married but share a household with a committed, long-term partner. Domestic partnerships are committed relationships between two unmarried partners of the same or opposite sex, who live together, share financial responsibility, and are both over the age of 18. Domestic partner health insurance extends health insurance benefits to a domestic partner, much like they are often offered to married spouses. This benefit typically also extends to the domestic partner's children.

| Characteristics | Values |

|---|---|

| Definition of a Domestic Partnership | Two people live together and share a domestic life as if married but are not married or joined by a civil union |

| Who Counts as a Domestic Partner? | A couple that is not married but lives together and shares a domestic life |

| Who Qualifies for Domestic Partner Health Insurance? | There are no universal qualifications; it depends on the state and employer |

| How to Prove You're a Domestic Partner | Lease, deed or mortgage in both names; joint bank and credit card accounts; driver's licenses bearing the same home address; life insurance policy, retirement benefits, or a last will and testament where you're each other's primary beneficiary; assignment of power of attorney |

| Children of Domestic Partners | Covered under health insurance plans |

| How to Add a Partner to Your Health Plan | Contact your plan administrator to understand the process and requirements |

| How to Choose Domestic Partner Insurance | Research your options, including premium costs, deductibles, and level of coverage |

| Employers and Domestic Partner Benefits | Employers are not required to offer domestic partner benefits but may choose to do so |

| Domestic Partner Health Insurance Tax | The portion of the insurance premium paid by the employer is taxed as income |

Explore related products

What You'll Learn

![]()

What defines a domestic partnership?

A domestic partnership is a legally recognised relationship between two people who live together and share a domestic life but are not married or joined by a civil union. Domestic partnerships are composed of two people of any gender, and there are no universal qualifications for what defines a domestic partnership as it is not federally recognised in the US. Instead, each state sets its own definition and decides on the legal benefits partners can receive.

In general, a domestic partnership is a committed relationship between two unmarried and unrelated adults of the same or opposite sex. They live together in a shared residence, share financial responsibilities, and are not married or in a civil union with anyone else.

To qualify as domestic partners, couples typically need to meet certain requirements, including:

- Living together for at least six months to a year

- Intending to continue living together

- Being at least 18 years old

- Sharing basic living expenses

- Not being married or in a domestic partnership with anyone else

- Being unrelated by blood

- Being financially interdependent

The Intricacies of CPI in Insurance: Unraveling the Complexities of Coverage and Protection

You may want to see also

Explore related products

![]()

How do you prove a domestic partnership?

To prove a domestic partnership, you must submit an affidavit of domestic partnership. This affidavit should be provided by your employer or insurer and will outline the eligibility requirements. These requirements can vary, but generally, to be considered a domestic partnership, you and your partner must:

- Not be related to each other

- Not be currently in a domestic partnership, civil union, or marriage with a different person

- Be mutually responsible for each other financially and legally

- Be in an intimate, committed relationship of at least six months

- Be living together

To prove these requirements are met, you will need to submit various forms of documentation. For example, to prove financial interdependence, you may need to provide documentation such as joint bank accounts, joint ownership of property, or shared budgeting. To prove cohabitation, you may need to provide documentation such as a lease agreement, driver's license, or utility bill that lists both names and a shared residential address.

It is important to note that the specific requirements and acceptable forms of documentation may vary depending on your employer, insurer, or the state in which you reside. For example, in New York State, proof of financial interdependence is a necessary criterion for domestic partnership eligibility. Therefore, it is essential to carefully review the eligibility requirements and acceptable forms of documentation before submitting your application.

Additionally, some sources suggest that registering your domestic partnership with your city or state can make it easier to prove your partnership. This process can vary depending on your location, so be sure to check the specific requirements in your area.

Understanding Rebating in Insurance: Unraveling the Practice and Its Implications

You may want to see also

Explore related products

![]()

What is domestic partner health insurance?

Domestic partner health insurance is an insurance plan that extends health insurance benefits to a domestic partner, much like they are often extended to married spouses. Domestic partnerships are committed relationships between two unmarried people of the same or opposite sex, who live together and share a domestic life. They are not joined by blood, marriage, or civil union.

The term "domestic partner" is often used in health insurance to describe who may be covered by a family health policy. Insurance companies typically require proof of a domestic partnership, such as a lease, deed, or mortgage in both names, as well as joint bank and credit card accounts.

Domestic partner health insurance covers both partners as if they were married, and it also covers their children. This type of insurance is becoming more common as marriage rates decline and cohabitation increases.

There is no universal qualification for domestic partner health insurance, as federal law does not define or recognize domestic partnerships. The qualifications vary by state, insurance provider, and employer.

If you are considering domestic partner health insurance, it is important to research the specific requirements and benefits offered by your state, insurance provider, and employer.

The Language of Insurance: Understanding the Concept of a "Carrier

You may want to see also

Explore related products

![]()

What are the tax implications of domestic partner health insurance?

Domestic partnerships are when two people live together and share their lives as if married, but they are not married or in a civil union. People in domestic partnerships enjoy the same rights and benefits as married couples, including health insurance coverage. However, there are some tax implications to consider when it comes to domestic partner health insurance.

Tax Implications of Domestic Partner Health Insurance

While federal law dictates that spouses' and dependents' health insurance premiums are not taxed, domestic partnerships are not recognized by the federal government. This means that the premiums paid for a domestic partner and their dependents are considered taxable income for the employee. This includes both the portion paid by the employer and the portion paid by the employee. The employee will have to pay income tax and Social Security taxes on the premium every paycheck.

However, there are a few ways to avoid these adverse tax consequences:

- Tax Dependent: If your domestic partner qualifies as your tax dependent under Internal Revenue Code §152 (as modified by §105(b)), their coverage will be treated the same as a spouse for federal and state income tax purposes.

- Registered Domestic Partnership: If your non-tax dependent domestic partner is registered as such under state law, their coverage will be treated as a spouse for state income tax purposes. However, post-tax payment and imputed income will still apply for federal income tax purposes.

It's important to note that each state has its own definition of a domestic partnership, and some states do not recognize them at all. Therefore, it's crucial to understand the laws and requirements of your specific state when considering domestic partner health insurance and the associated tax implications.

Child's Education and Insurance: Navigating the Complexities of Change

You may want to see also

Explore related products

![]()

How do you get domestic partner health insurance?

Domestic partner health insurance is when health insurance benefits are extended to a domestic partner, much like they are to married spouses. Generally, this benefit will also extend to the domestic partner's children.

Who Qualifies as a Domestic Partner?

There is no single rule that defines a domestic partnership across all states. Each state sets its own definition, and employers may also have their own definitions.

In general, a domestic partnership is when two people live together and share a domestic life as if married but are not married or joined by a civil union. Domestic partners must be a couple for insurance purposes and cannot be married to a third person.

How to Get Domestic Partner Health Insurance

If you and your partner want to get domestic partner health insurance, here are the steps you can follow:

- Check your state's laws and your employer's policies: The first step is to determine if your state and employer recognize domestic partnerships and offer domestic partner health insurance. You can start by checking with your employer's human resources department and reviewing your employee benefits package.

- Prove your domestic partnership: If your state and employer recognize domestic partnerships, you will need to meet certain criteria and provide proof of your partnership. This could include documentation such as a lease, deed, mortgage, joint bank accounts, driver's licenses, or an affidavit certifying your relationship.

- Sign up for domestic partner benefits: Once you have confirmed that you meet the criteria and provided the necessary documentation, you can sign up for domestic partner benefits through your employer or your partner's employer. You may need to fill out forms and provide additional information as required by your employer or insurance provider.

- Explore other options: If your employer does not offer domestic partner health insurance, you can explore other options such as private insurance companies or insurance exchanges. You can also consider asking your employer to add domestic partner benefits to their health insurance plan, as studies have shown that the costs of offering these benefits are usually negligible for employers.

It is important to note that federal law does not recognize domestic partnerships, so there may be tax implications for employees who choose to enrol their domestic partners in their health insurance plans. It is recommended to consult a lawyer or tax professional before signing up for domestic partner benefits to fully understand your rights and any potential tax consequences.

The Renewal Riddle: Unraveling the Mystery of Level Term Insurance

You may want to see also

Frequently asked questions

A domestic partnership is when two people live together and share their domestic life as if married, but they are not married or joined by a civil union. Domestic partnerships are composed of two people of any gender.

There is no universal rule for who qualifies as a domestic partner for health insurance. The definition varies from company to company and state to state. However, some common criteria include:

- Living together for at least six months

- Being 18 or older

- Sharing a close personal relationship and being responsible for each other's welfare

- Not being married to anyone else

- Sharing the same residence and intending to continue doing so

- Being financially interdependent

The process for adding a domestic partner to your health insurance will depend on your insurance provider. You will likely need to provide proof of your domestic partnership, such as a lease, deed, mortgage, joint bank accounts, or credit card statements. You may also need to sign an affidavit confirming that you meet the requirements for a domestic partnership.