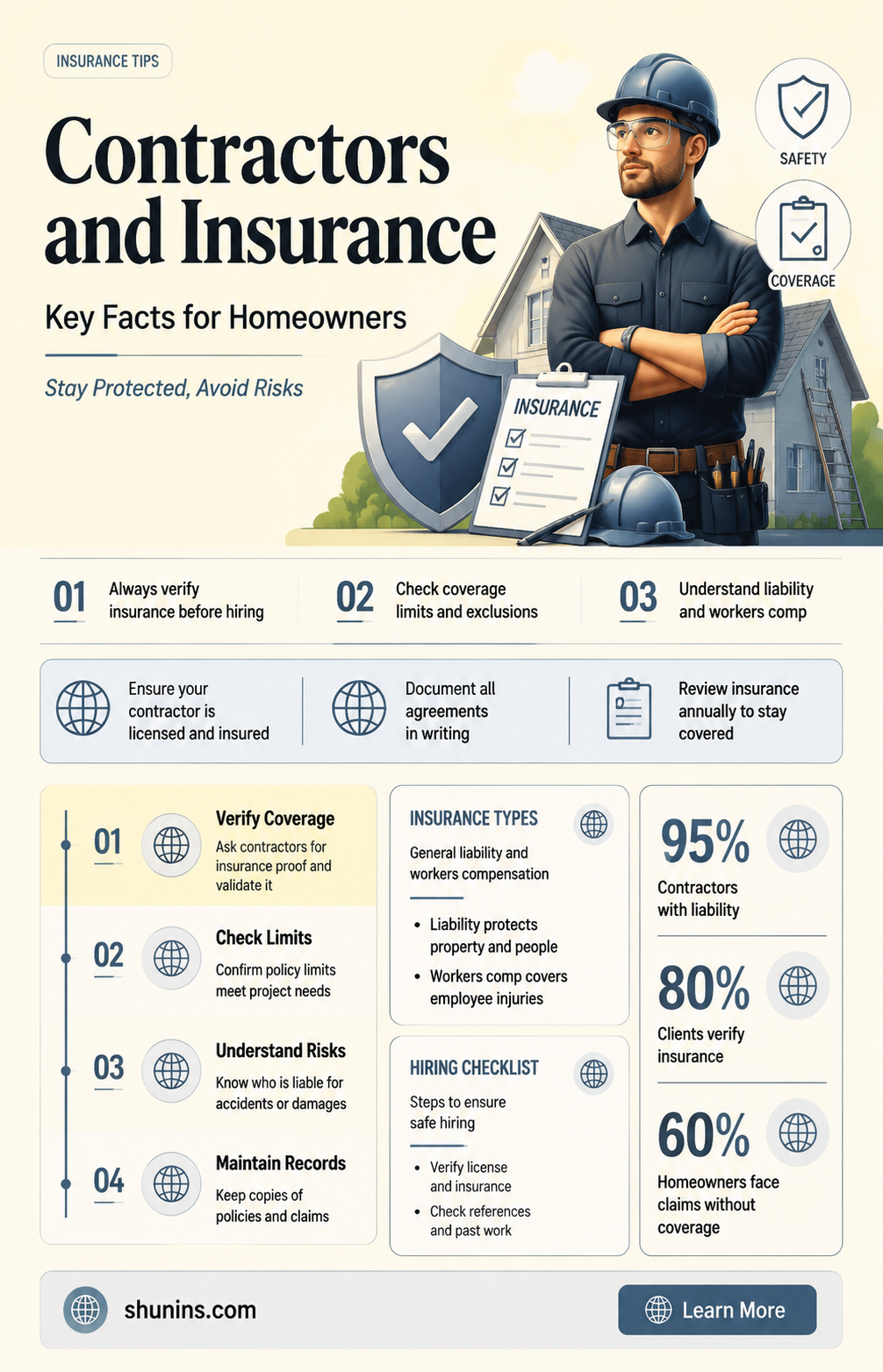

Contractors are often required to have insurance to protect themselves, their clients, and their employees. The type of insurance and level of coverage vary depending on the contractor's business structure, the size and scope of the project, and the requirements of the client or project owner. General liability insurance, for example, protects contractors from claims of property damage or personal injury that may occur during their work. Worker's compensation insurance, on the other hand, covers employees' medical expenses and lost wages if they are injured on the job. Other types of insurance that contractors may need include auto liability insurance, errors and omissions (E&O) insurance, and specialty insurance for specific industries or risks. While insurance is not a legal requirement for all contractors in all locations, it is essential for risk management and provides peace of mind for both the contractor and the client.

| Characteristics | Values |

|---|---|

| Are contractors insured? | It depends on the contractor and the location. Most reputable contractors have insurance. However, some contractors do not have insurance, which can be a red flag. |

| Why do contractors need insurance? | Insurance provides financial security and peace of mind, covering the costs of legal defence, repairs or replacements, medical expenses, and lost wages in the event of an accident or property damage. It also protects clients from potential liabilities. |

| Types of insurance for contractors | General liability insurance, worker's compensation insurance, auto liability insurance, errors and omissions insurance, and property insurance are some common types of insurance for contractors. |

| Verifying contractor's insurance | Request a certificate of insurance from the contractor and verify the details, including the contractor's name, date of issue, and your name as the certificate holder. |

| Risks of hiring uninsured contractors | If something goes wrong during a construction project, you may be held liable for any accidents, property damage, or injuries that occur. This could result in significant financial burden and legal consequences. |

Explore related products

$9.99 $15.99

What You'll Learn

![]()

Why contractors need insurance

Contractors need insurance to protect themselves, to work legally in some locations, and to give clients peace of mind.

Contractors must ultimately customise their coverage to meet their specific needs and risks. However, the most common types of insurance for contractors are general liability insurance, workers' compensation insurance, and auto liability insurance.

General liability insurance covers third-party claims of bodily injury, property damage, and personal injury. It covers the cost of repair for damages caused by the contractor while doing work on a client's property. For example, if a landscaper loses control of their lawnmower and damages a parked car, liability insurance would cover the damage and any legal costs the contractor experiences from the accident. It also covers injury claims, such as medical or funeral expenses if anyone gets injured while on duty. However, it does not cover poor workmanship or professional negligence.

Workers' compensation insurance is designed to protect workers if they are injured on the job and reimburse them if they are unable to return to work. For contractors, this type of coverage can prevent a costly lawsuit and hefty legal fees. It is required in most jurisdictions.

Auto liability insurance is important for contractors who transport equipment and materials in their trucks. If there is an accident while loading or unloading materials, this would be an auto insurance claim and not a general liability claim.

Life Insurance with HIV: Is It Possible?

You may want to see also

Explore related products

![]()

Types of insurance coverage

Contractors are generally required to have insurance to protect themselves, to work legally in some locations, and to give clients peace of mind. There are various types of insurance coverage that contractors may need to consider, depending on the nature of their work and the specific requirements of the state or location in which they operate. Here are some common types of insurance coverage for contractors:

- General Liability Insurance: This type of insurance provides protection against claims arising from bodily harm or property damage that occurs during the course of business. It covers accidents, such as a contractor accidentally spraying paint onto neighbouring properties, or a landscaper losing control of their mower and damaging a parked car. It also covers any legal costs arising from such incidents.

- Workers' Compensation Insurance: This type of insurance is designed to protect contractors' workers or employees if they are injured on the job. It provides compensation for medical expenses and lost wages while they are unable to work. In some states, this type of insurance is required for businesses with a certain number of employees, and it may also be mandatory for independent contractors.

- Commercial Auto Insurance: This type of insurance covers company-owned vehicles and equipment from damages caused by motor vehicle accidents, theft, and vandalism. It helps businesses avoid high vehicle repair costs and medical expenses resulting from auto accidents. This type of insurance is required in every state when a company purchases a vehicle for employee or owner use.

- Errors and Omissions (E&O) Insurance: Also known as professional liability insurance, this type of insurance covers financial losses arising from claims of errors, mistakes, or omissions made by the contractor or their subcontractors in the course of conducting business. It is particularly relevant for businesses that provide construction consulting services or regularly hire subcontractors.

- Builder's Risk Insurance: This type of insurance, also known as course-of-construction insurance, provides protection for buildings that are under construction or remodelling. It typically covers damages caused by fire, weather, vandalism, or theft. Some insurers also offer "premium coverage" options that extend protection to include damages from earthquakes or flooding.

- Specialized Contractor Insurance: Depending on the nature of their work, contractors may require specialized insurance policies. For example, electrical contractors may need completed operations insurance to cover claims arising from electrical fires after a project is completed. Similarly, pollution liability insurance may be necessary for contractors who frequently work with or dispose of hazardous waste.

It is important for contractors to carefully review the specific insurance requirements for their industry and location, as well as the scope of coverage provided by each policy, to ensure they have adequate protection.

Life Insurance Proceeds: Texas Tax Laws Explained

You may want to see also

Explore related products

![]()

Verifying a contractor's insurance

Research and Licensing:

Start by conducting thorough research to find qualified and experienced contractors in the specific type of work you require. Verify their licenses and bonds, as these indicate that the contractor is authorised to operate and is committed to delivering a reasonable standard of work. Check with your local authorities to ensure the contractor has the necessary permits and licensing requirements for your area.

Request for Proof of Insurance:

Ask the contractor to provide proof of their insurance coverage. A reputable contractor should be willing to share their insurance certificates and policies upon request. Request an ACORD Certificate of Insurance (COI), which will list their liability insurance underwriters. Ensure that the contractor's name on the COI matches the name of the contractor or company you are hiring. Check the date of issuance to ensure that the insurance is still valid, and verify that your name is listed as the certificate holder.

Verify the Insurance Policy:

Don't just take their word for it; verify the insurance policy by contacting the insurance companies listed on the COI. Provide them with the policy number and confirm the stated coverage, limits, and effective dates. You can also contact the contractor's insurance broker directly to obtain a Certificate of Insurance, which confirms their coverage.

Additional Considerations:

In addition to general liability insurance, consider other types of insurance relevant to the project. For example, if the contractor will be using their vehicles for loading and unloading, you may want to require auto liability insurance. Also, remember to review your own insurance coverage to ensure you are protected in case the contractor's insurance is insufficient or expired.

Subcontractors:

If the contractor hires subcontractors, ensure they are also insured. Ask the contractor for proof of insurance for all subcontractors or request certificates directly from the subcontractors.

By following these steps, you can be confident that you are hiring a contractor who is properly insured, reducing potential risks and providing peace of mind.

Life Insurance and THC: What You Need to Know

You may want to see also

Explore related products

![]()

Risks of uninsured contractors

Contractors are typically required to have insurance to protect themselves, to work legally in some locations, and to give clients peace of mind. However, some contractors may choose to operate without insurance, which can pose significant risks to both the contractor and the client. Here are some key risks associated with hiring uninsured contractors:

Financial Risk

If an uninsured contractor causes damage to property or injuries to others, the financial burden may fall on the client or project owner. Homeowner's insurance policies often do not provide sufficient coverage for construction-related accidents, leaving the property owner liable for any damages. This can result in unexpected expenses and even financial ruin if the client is unable to cover the costs.

Legal Consequences

Hiring uninsured contractors can lead to legal non-compliance and penalties for the client or project owner. Specific laws and regulations require certain types of insurance coverage on job sites. Failing to ensure that contractors are properly insured can result in fines and other legal repercussions for non-compliance.

Liability for Workplace Injuries

If an uninsured contractor or their employee is injured on the job, the project owner or client may be held responsible for covering medical expenses and lost wages. This is especially true in states with workers' compensation laws, which stipulate that the responsibility for these costs falls on the hiring entity if the contractor is uninsured.

Compromised Safety Standards

Uninsured contractors may be more likely to cut corners and compromise safety standards to reduce costs. This can lead to unsafe working conditions, higher accident rates, and potential violations of industry regulations or OSHA guidelines. Ensuring contractors have adequate insurance helps maintain high safety standards on the job site.

Substandard Work

Uninsured contractors may be more prone to delivering substandard work or using poor-quality materials. If the work is not up to code, the client may have to disclose this to potential homebuyers, affecting the property's value. Licensed and insured contractors are more likely to perform quality work and provide long-term savings by avoiding costly corrections.

Hiring uninsured contractors can expose clients to financial, legal, and safety risks. It is crucial for clients to verify that contractors have adequate insurance coverage to protect themselves from these potential pitfalls.

Printing Your Life Insurance License: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Insurance and legal requirements

Contractors are usually required to have insurance to protect themselves, their clients, and their employees. The specific insurance requirements for contractors can vary depending on the location and the size and scope of the project. Here are the key insurance and legal requirements for contractors:

General Liability Insurance

General liability insurance is essential for contractors as it covers claims arising from property damage or personal injury caused by their operations. This insurance protects both the contractor and the client by covering the costs of repairs, medical bills, and legal defence in case of an accident or incident during the project. It is important to note that general liability insurance does not cover professional negligence, and separate coverage may be needed for that.

Worker's Compensation Insurance

Worker's compensation insurance is crucial for contractors with employees. It covers medical expenses and lost wages for employees who are injured on the job or unable to work due to a work-related injury. This type of insurance can vary based on location and the specific contracting trade. It helps protect both the contractor and the client from costly lawsuits and legal fees arising from workplace injuries.

Commercial Auto Insurance

Commercial auto insurance is important for contractors who use vehicles for their operations. It covers property damage or bodily harm caused by vehicles involved in an accident. This type of insurance is particularly relevant during loading and unloading materials and equipment, as these incidents would fall under auto insurance claims rather than general liability claims.

License and Bonding Requirements

In addition to insurance, contractors may need to obtain licenses and bonds to operate legally. Licenses are often required for contractors to bid on certain projects and provide assurance of their qualifications. Bonds are sometimes necessary to guarantee the contractor's performance and protect clients from financial loss if the contractor fails to complete the job or does a substandard job.

Proof of Insurance and Verification

Contractors should be able to provide proof of insurance, typically in the form of a certificate of insurance. This document should include the contractor's name, the types of coverage they have, policy limits, and the dates of coverage. It is important to verify that the insurance is valid, up to date, and applicable to the specific project.

Additional Specialty Insurance

Depending on the nature and scope of the project, contractors may need additional specialty insurance. This could include umbrella insurance to extend liability limits beyond the standard cap, errors and omissions (E&O) insurance to cover professional negligence or mistakes, and equipment coverage to protect their machinery and tools from damage or theft.

Universal Life Insurance: More Problems Than Solutions?

You may want to see also

Frequently asked questions

Hiring insured contractors is a way to protect yourself from liability in case something goes wrong during the project. For example, if a worker accidentally punctures a water line, the contractor's insurance will cover the repair bills. Insured contractors are also more likely to do a quality job to avoid losing their license.

The two main types of coverage to look for are general liability insurance and workers' compensation insurance. General liability insurance protects contractors from claims of property damage or personal injury that could occur during their work. Workers' compensation insurance covers employees in case they are injured while working, reimbursing them for medical bills and lost wages. Depending on the project, you may also want to look for auto liability insurance, errors and omissions insurance, and equipment coverage.

Ask the contractor for a certificate of insurance and verify that it applies to your specific project. Check that the contractor's name on the certificate matches, the date is recent, and your name is listed as the certificate holder. You can also contact the insurance agency to verify that the policies are still in effect.