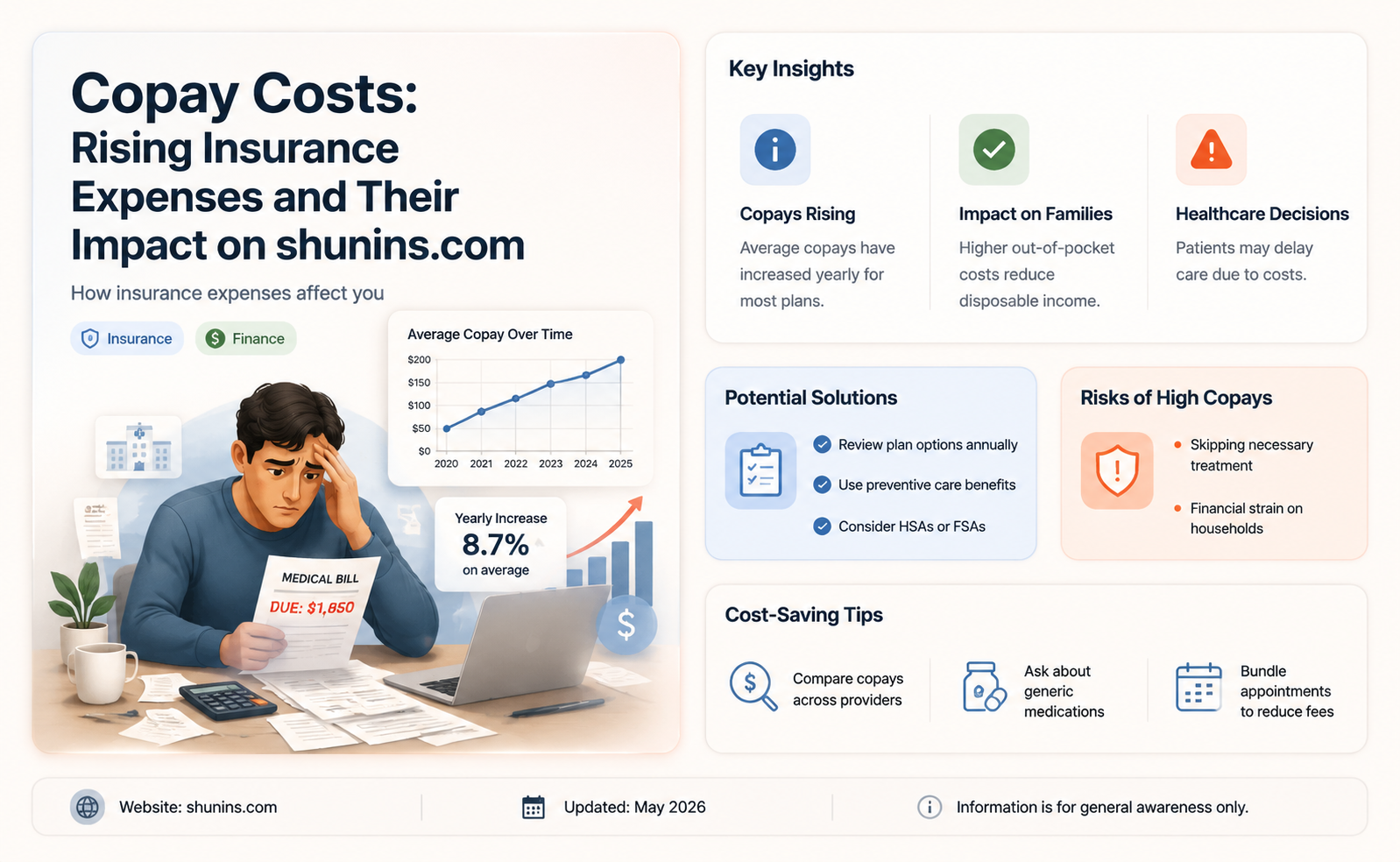

Health insurance costs in the US have been steadily increasing, with employers bracing for the highest spike in 15 years in 2025. This will inevitably lead to employees shelling out more for healthcare from their paychecks, including higher copays, deductibles, and premiums. This trend is attributed to various factors, including advances in medical science, increased market concentration among insurance providers, rising prescription drug prices, and the lingering effects of the pandemic. With costs expected to continue rising, employers and employees alike are seeking ways to manage the financial burden.

| Characteristics | Values |

|---|---|

| Health insurance costs | Increasing |

| Copayments | Increasing |

| Cost-sharing between insurance providers and patients | Increasing |

| Average deductibles | Increased from $303 in 2006 to $1,200 in 2016 |

| Average copayments | Decreasing |

| Average coinsurance | Increased from 28% of total employee cost-sharing in 2006 to 31% in 2016 |

| Health benefit cost trend components | Healthcare price and utilization |

| Factors contributing to higher insurance costs | Inflation, virtual healthcare adoption, medical advancements, market concentration, prescription drug prices |

| Percentage of employers intending to make cost-cutting changes to health insurance plans in 2026 | 59% |

| Projected increase in total health benefit costs per employee in 2026 | 6.5% |

| Projected increase in health insurance costs for companies in 2026 | 7.6% |

Explore related products

What You'll Learn

![]()

Rising prescription drug prices

One of the primary reasons for the increase in prescription drug prices is the existence of monopolies. Certain pharmaceutical companies hold a significant market share for specific drugs, such as insulin, and this lack of competition allows them to maintain high prices. Additionally, there are often no alternative treatments for serious illnesses like cancer, giving these companies even more pricing power. Furthermore, the development of new drugs is a lengthy and costly process, with only a small percentage of drugs tested becoming successful and reaching the market. This dynamic justifies, to some extent, the high prices charged for these drugs. However, it is important to note that public funding contributes significantly to the science behind most new drugs, giving the public a legitimate right to ensure that life-saving medications are priced fairly.

The high launch prices of new brand biologics and year-over-year price increases for brand-name drugs that face little to no competition due to abuses of the patent system are also significant contributors to rising prescription drug costs. Brand-name drugs now account for 77% of all spending on prescription drugs, resulting in higher pharmacy costs, premiums, and deductibles for patients. This has led to a situation where many patients are unable to afford their medication, negatively impacting their health and well-being.

Another factor influencing prescription drug prices is the increased utilization of healthcare services. The rise of virtual healthcare has removed geographic barriers and made it more convenient for patients to seek treatment. As a result, more people are using various health services, including mental health services, driving up overall utilization and, consequently, prescription drug costs.

To address the issue of rising prescription drug prices, increasing patient access to more affordable, FDA-approved generic and biosimilar medicines has been suggested as a proven solution. When generic alternatives are available, prices can be 80-85% lower than brand-name drugs. While the FDA has approved several biosimilars, only a few are currently available to patients. Additionally, regulating monopolies and implementing value-based pricing can help control prescription drug prices and protect citizens from unreasonable costs.

Life Insurance: A Wealthy Person's Guide to Financial Security

You may want to see also

Explore related products

![]()

Higher healthcare utilisation

The rising cost of healthcare insurance is a cause for concern for many. Health insurance prices in the US have been increasing for four consecutive years, and employers are now facing the highest spike in 15 years, according to a survey of over 1,700 employers.

There are several factors contributing to this surge in healthcare costs, and one of the primary factors is higher healthcare utilisation. Sunit Patel, Mercer's US Chief Actuary for Health and Benefits, stated that "health benefit cost trend has two primary components - healthcare price and utilisation. Right now, both are rising."

Additionally, the rise of virtual healthcare has played a significant role in increasing utilisation. The pandemic accelerated the adoption of virtual healthcare options, making it more convenient for people to seek medical attention. Virtual healthcare removes geographic barriers and allows patients to access care from the comfort of their homes. This has resulted in higher overall utilisation, driving up aggregate claims and contributing to the surge in healthcare costs.

Furthermore, there has been an increase in the use of specific medications and treatments that contribute to escalating costs. For example, GLP-1 drugs, which are used for diabetes and weight loss, are covered by many employers and have led to higher expenses. Similarly, advancements in medical science, such as new cancer treatments and weight-loss medications, come at steep costs compared to previous therapies. These cutting-edge treatments are often life-changing but can significantly impact the overall cost of healthcare.

While higher healthcare utilisation is a significant factor in rising insurance costs, it is not the sole reason. Other factors, such as inflation, increased wages in the healthcare sector, and the consolidation of providers into large health systems, also contribute to the increasing financial burden on individuals and employers.

Group Variable Universal Life Insurance: What You Need to Know

You may want to see also

Explore related products

$8.99 $10.99

![]()

Inflation and wage increases

The COVID-19 pandemic has also played a role in increasing healthcare costs. Firstly, there has been a rise in virtual healthcare, which has made it more convenient for people to seek care, leading to higher overall utilisation. Secondly, there has been an increase in the number of people with chronic illnesses and mental health conditions, which has resulted in inflated health spending. Additionally, there has been a rise in the use of expensive specialty drugs, such as GLP-1 medications, which employers are now covering for diabetes and obesity.

As a result of these factors, employers are expecting a significant increase in health benefit expenses, with Mercer projecting a 6.5% hike for 2026. This will lead to higher out-of-pocket expenses for employees, including higher copays and deductibles. While some employers may try to limit the increase in premiums, they often do so by shifting costs elsewhere, such as increasing copays. Therefore, it is essential for employees to carefully review their health insurance plans and select the most suitable option for their needs.

Spouse Insurance: Dependent Life Coverage Explained

You may want to see also

Explore related products

$49.16 $54.97

![]()

Market concentration

The US health insurance industry is highly concentrated, and insurance premiums are rising rapidly. The link between market concentration and premiums is complex. While higher concentration can lead to increased insurer market power and higher profit margins, it may also provide insurers with stronger bargaining power to negotiate lower payment rates with hospitals, potentially offsetting higher premiums. However, the overall effect is that of higher costs for consumers.

Consolidation in the insurance industry, through mergers and acquisitions, has contributed to market concentration. This consolidation reduces the number of issuers available to consumers and creates barriers to new entrants, perpetuating the issue. The impact of market concentration is not limited to premiums but also affects the accessibility and affordability of healthcare. Insurance companies' expanding influence allows them to enforce narrow provider networks, demand high deductibles and copays, and deny coverage for essential services, hindering timely and affordable care.

To address these challenges, administrative professionals and policymakers must develop strategies to enhance market competition, improve price transparency, and curb the growth rate of healthcare prices. The Patient Protection and Affordable Care Act (ACA) includes provisions to increase insurer competition and address the level of competition in the industry. However, progress has been slow due to the market's complexity.

Athene Life Insurance: A Giant in the Industry

You may want to see also

Explore related products

![]()

Advanced medical treatments

The cost of advanced medical treatments is a pressing issue, with countries striving to balance healthcare expenses and the need for quality care. The global medical treatment market involves substantial investments in research, advanced technology, and expenses related to medical personnel and equipment.

The cost of advanced medical treatments is influenced by several factors, including the complexity of the procedure, the use of advanced medical equipment, and the expertise of the medical staff. For instance, a double lung transplant, which involves a highly skilled team of surgeons, pulmonologists, and other specialists, can cost approximately $850,000. Intestinal and small bowel transplants are also among the most expensive procedures, ranging from $275,000 to $1,147,300 due to their complexity and post-transplant care requirements.

The cost of advanced treatments is further impacted by the facility where the treatment is administered. For example, treatments for peripheral artery disease (PAD) can vary in cost depending on whether they are performed at a specialized cardiovascular centre or a general clinic. Diagnosis and testing for PAD can cost around $1000-$3000, while treatment may involve lifestyle changes, medications, exercise therapy, or surgical interventions.

The increasing cost of advanced medical treatments has contributed to rising health insurance prices. According to surveys, health insurance costs in the United States are projected to increase by 6.5% in 2026, with employers and employees facing higher premiums, deductibles, and out-of-pocket expenses. This trend is influenced by advancements in medical science, increased utilization of healthcare services, and rising wages in the healthcare sector.

The rising costs of advanced medical treatments and insurance have sparked concerns about affordability and cost-sharing between insurance providers and patients. As expenses continue to climb, managing the financial burden of these treatments becomes a critical challenge for individuals and healthcare systems worldwide.

How to Cash Out Whole Life Insurance Policies?

You may want to see also

Frequently asked questions

Yes, copayments for insurance are increasing. This is due to a variety of reasons, including the rising cost of prescription drugs, inflation, and increased market concentration among insurance companies.

A copay is a fixed amount that you pay for health services, such as doctor visits or prescriptions. Copayments are a form of cost-sharing between insurance providers and patients.

It is difficult to say exactly as this will depend on the insurance provider and the specific plan. However, some sources suggest that copays could increase by as much as 6% to 7% on average.

There are several reasons why copays are increasing. One factor is the rising cost of healthcare, including the cost of prescription drugs. Another factor is increased market concentration among insurance companies, which may result in higher premiums and decreased access to affordable health insurance. Additionally, inflation and increased wages in the healthcare sector have contributed to higher overall costs.

The increase in copays is likely to result in higher out-of-pocket costs for individuals. This means that people may have to pay more for their healthcare services, adding to the financial burden on consumers.