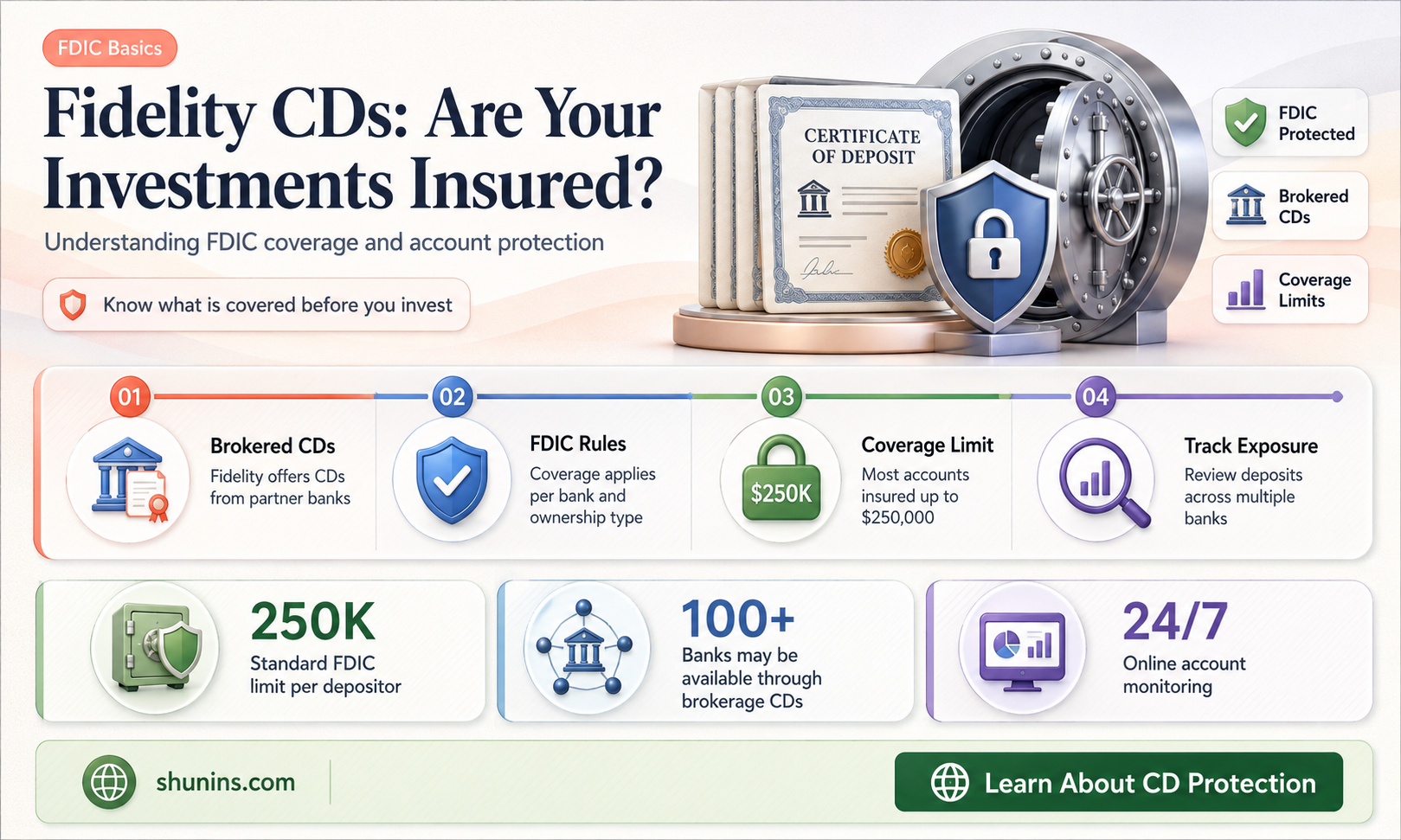

Certificates of deposit (CDs) are a type of fixed-income investment offered by Fidelity. CDs are issued by banks for customers of brokerage firms and typically come with a set interest rate. Brokered CDs are FDIC-insured up to $250,000 per account owner, per issuer. This limit was made permanent in 2010 and provides coverage for deposits in the event of bank insolvency. By purchasing brokered CDs from multiple banks, investors can expand their FDIC coverage beyond the $250,000 limit. It's important to note that FDIC insurance does not cover market losses or premiums paid above par value for secondary market CDs.

| Characteristics | Values |

|---|---|

| Type of insurance | FDIC insurance |

| Coverage limit | USD 250,000 per account owner, per issuer |

| Coverage limit made permanent | 2010 |

| Coverage limit per account type | USD 250,000 |

| Coverage limit per institution | USD 250,000 |

| Coverage limit per category of account | USD 250,000 |

| Coverage for market losses | Not covered |

| Coverage for premium to principal value | Not covered |

| Coverage for secondary market CDs | Not covered |

Explore related products

What You'll Learn

- Brokered CDs are FDIC-insured up to $250,000 per account owner

- Fidelity offers brokered CDs from multiple banks, allowing expanded FDIC protection

- FDIC insurance does not cover market losses

- CDs may be purchased on the secondary market, but the premium is not eligible for FDIC insurance

- CDs are debt instruments, so there is credit risk associated with their purchase

![]()

Brokered CDs are FDIC-insured up to $250,000 per account owner

Brokered CDs are issued by banks for the customers of brokerage firms. They are usually issued in large denominations, and the brokerage firm divides them into smaller denominations for resale to its customers. Because the deposits are obligations of the issuing bank, FDIC insurance applies. Brokered CDs are similar to traditional bank CDs in many ways. They both pay a set interest rate that is generally higher than a regular savings account, and they both repay your principal with interest if they are held to maturity.

One key advantage of brokered CDs is that they allow investors to buy CDs from multiple banks in one place, letting investors expand their FDIC coverage beyond the $250,000 limit in a single account registration type. By combining CDs from different FDIC-insured banks, investors can expand their protection while keeping their assets consolidated in one account. This is a significant benefit that is not possible with traditional bank CDs.

It is important to note that while brokered CDs offer FDIC insurance, there is still credit risk associated with their purchase. Customers are responsible for evaluating both the CDs and the creditworthiness of the underlying issuing institution. In the event of insolvency, the CD may be placed in regulatory conservatorship, with the FDIC typically appointed as the conservator.

Federal Life Insurance: Open Season Timing and Details

You may want to see also

Explore related products

$6.37

![]()

Fidelity offers brokered CDs from multiple banks, allowing expanded FDIC protection

Certificates of deposit (CDs) are debt instruments, meaning there is credit risk associated with their purchase. The insurance offered by the Federal Deposit Insurance Corporation (FDIC) helps to mitigate this risk. FDIC insurance covers up to $250,000 per account owner, per issuer, per institution. This coverage limit was made permanent in 2010.

Fidelity offers brokered CDs, which are issued by banks for the customers of brokerage firms. Brokered CDs are similar to bank CDs in many ways, but they are purchased through a broker. Brokered CDs can be bought from multiple banks in one place, allowing investors to expand their FDIC coverage beyond the $250,000 limit in a single account registration type. This is because each bank provides FDIC protection up to the current FDIC limits, so combining CDs from different banks in a Fidelity account expands the overall protection.

For example, an investor could combine CDs from four different banks, each providing FDIC protection up to $250,000, in their Fidelity account. This would result in a total FDIC protection of $1,000,000. It is important to note that FDIC insurance does not cover market losses or any price above par that is paid for a secondary market CD.

By offering brokered CDs from multiple banks, Fidelity provides investors with expanded FDIC protection options, allowing them to increase their coverage beyond the limits of a single bank. This can be a valuable feature for those looking to protect larger investments.

Life Insurance Limits: Why the Cap?

You may want to see also

Explore related products

![]()

FDIC insurance does not cover market losses

Certificates of deposit (CDs) offered by Fidelity are FDIC-insured up to $250,000 per account owner, per issuer. FDIC insurance covers par value plus any accrued and unpaid interest for the CD. However, it's important to note that FDIC insurance does not cover market losses.

FDIC insurance is designed to protect depositors' funds in the event of a bank failure. It does not cover losses incurred due to market fluctuations or the performance of the CD. The FDIC insurance coverage limit of $250,000 is per account owner, per institution. This means that if an individual has multiple accounts at different banks, each account is insured up to $250,000. Similarly, if a joint account is held by multiple people, each account owner is insured up to $250,000 for their portion of the account.

While FDIC insurance provides peace of mind for depositors, it is not meant to be a substitute for prudent investment decisions. As with any investment, there is a degree of risk associated with purchasing CDs, and investors should carefully consider their options before making a decision. It's important to remember that FDIC insurance does not guarantee profits or protect against all possible losses.

In the case of market losses, the FDIC will not provide coverage. Market losses refer to situations where the value of the CD decreases due to market conditions or other economic factors. Investors should be aware that the performance of their CDs may vary, and there is always the possibility of losing money. While FDIC insurance protects against the failure of the issuing bank, it does not guarantee the performance or profitability of the investment itself.

It's worth noting that there are ways to mitigate the risk of market losses. Diversifying one's investments across different types of assets and industries can help spread out the risk. Additionally, conducting thorough research and due diligence before investing can help investors make more informed decisions. While FDIC insurance provides a safety net for certain types of losses, it's important for investors to understand the limitations of this protection and take responsibility for managing their investment risks.

Colorado Life Insurance Exam: Challenging or Easy?

You may want to see also

Explore related products

![]()

CDs may be purchased on the secondary market, but the premium is not eligible for FDIC insurance

Certificates of deposit (CDs) are debt instruments, and as such, there is credit risk associated with their purchase. The FDIC insurance coverage limit is $250,000 per account owner, per issuer, for each applicable category of account. This limit was made permanent in 2010. The FDIC insurance covers the principal amount of the CD and any accrued interest.

Fidelity offers brokered CDs, which are CDs issued by banks for the customers of brokerage firms. Brokered CDs are similar to bank CDs in many ways. Both pay a set interest rate that is generally higher than a regular savings account, and both are debt obligations of an issuing bank. Brokered CDs, however, can be purchased from different issuing banks, allowing investors to expand their FDIC protection beyond the $250,000 limit in a single account registration type.

While brokered CDs can be sold on the secondary market, there are some drawbacks. Firstly, there may be a trading fee for selling CDs on the secondary market. Secondly, the market value of a CD in the secondary market may be influenced by factors such as interest rates, provisions such as call or step features, and the credit rating of the issuer. Lastly, and most importantly, CDs purchased on the secondary market may reflect a premium to their principal value, and this premium is not eligible for FDIC insurance. This means that if you purchase a CD on the secondary market at a price above par value, the amount above par value will not be covered by FDIC insurance.

Therefore, while brokered CDs offer advantages such as expanded FDIC protection and the ability to sell before maturity, it is important to carefully consider the potential drawbacks, especially the ineligibility of the premium for FDIC insurance.

Canceling CMFG Life Insurance: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

CDs are debt instruments, so there is credit risk associated with their purchase

Certificates of deposit (CDs) are debt instruments. This means that there is credit risk associated with their purchase. However, the insurance offered by the Federal Deposit Insurance Corporation (FDIC) can help mitigate this risk. It is important to note that customers are responsible for evaluating both the CDs and the creditworthiness of the underlying issuing institution.

The FDIC insurance covers the par value, which is usually $1,000 for most CDs, plus any accrued and unpaid interest for the CD. Therefore, any price above par that is paid for a secondary market CD would not be covered by FDIC insurance. Brokered CDs offered by Fidelity are FDIC-insured up to $250,000 per account owner, per institution. This means that if the issuing bank becomes insolvent, the FDIC may be appointed as the conservator, and the CDs may be paid off prior to maturity or transferred to another depository institution.

It is worth noting that there are some risks associated with CDs, such as call risk, where the issuer of a callable CD has the right to redeem the security before maturity and pay back the owner either the full value or a percentage of the value. Additionally, selling CDs before maturity may result in a substantial gain or loss due to interest rate changes and other factors. The market value of a CD in the secondary market may be influenced by factors such as interest rates, call features, and the credit rating of the issuer.

Fidelity offers brokered CDs, which are issued by banks but purchased through a broker. These CDs can be bought from multiple banks in one place, allowing investors to expand their FDIC coverage. Brokered CDs have some advantages over traditional bank CDs, such as the ability to sell them to another investor in the secondary market without paying an early withdrawal penalty. However, there can also be drawbacks to selling in the secondary market.

Answering Life Insurance Health Questions: A Step-by-Step Guide

You may want to see also

Frequently asked questions

Yes, Fidelity offers FDIC-insured brokered CDs up to $250,000 per account owner, per account type, per institution.

FDIC insurance covers the par value plus any accrued and unpaid interest for the CD. FDIC insurance does not cover market losses.

Brokered CDs are obligations of the issuing bank, so FDIC insurance applies. Brokered CDs can be insured beyond $250,000 by combining CDs from different FDIC-insured banks in one brokerage account.

Brokered CDs are purchased through a broker and held with the brokerage firm, while bank CDs are purchased directly from a bank. Brokered CDs offer more liquidity and can be sold on a secondary market.

If the issuer becomes insolvent, the CD may be placed in regulatory conservatorship, with the FDIC typically appointed as the conservator. The CDs may be paid off early or transferred to another institution.