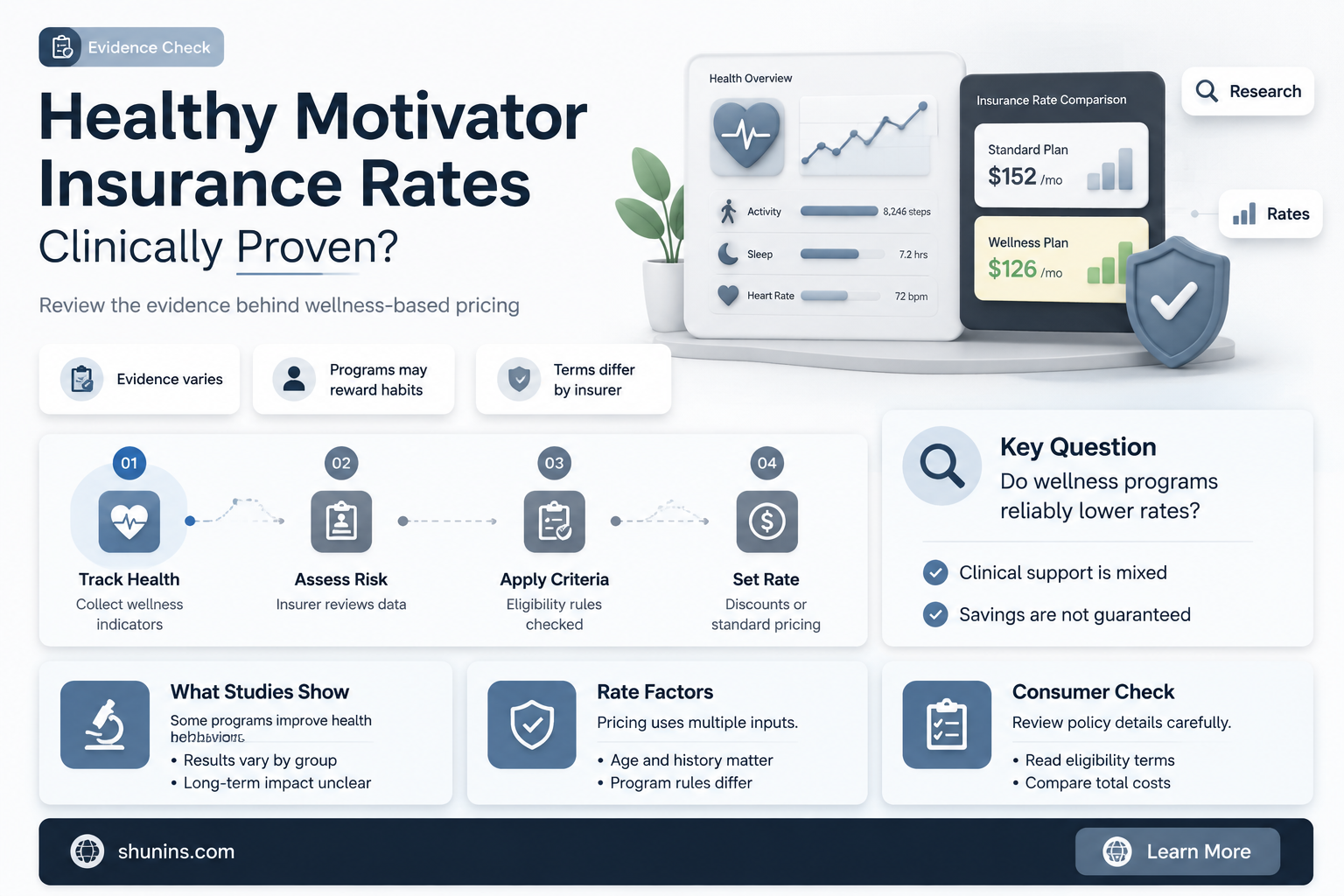

Health insurance companies are increasingly offering rewards programs to incentivize healthy behaviors and activities among their members. These programs are designed to motivate policyholders to adopt healthier lifestyles, improve their overall well-being, and reduce their healthcare costs. While the specific incentives vary, they often include rewards for achieving health-related goals, such as quitting smoking, losing weight, or increasing physical activity. Some companies also offer cash rewards, gift cards, or discounts on wellness-related resources for members who complete health assessments or biometric screenings. Additionally, there are insurance companies that combine an individual's current health, health literacy, and active lifestyle to offer lower insurance rates. These companies take into account factors such as BMI, cholesterol levels, and resting heart rate to better predict long-term health and offer rates that are up to 41% lower.

| Characteristics | Values |

|---|---|

| Company | Health IQ |

| Combines | Current health, health literacy, and active lifestyle |

| Predicts | Long-term health |

| Reduces | Chance of being penalized for poor family history |

| Has | BMI buffer for clients with above-average muscle mass |

| Recognizes | Low resting heart rate as a sign of excellent health and fitness |

| Type of program | Health insurance rewards program |

| Purpose | Motivate policyholders to adopt healthy habits |

| Example | Incentivize policyholders to take active steps to quit smoking or lose weight |

Explore related products

What You'll Learn

![]()

Health literacy and active lifestyle

Health literacy is a critical component of an individual's overall health and well-being. It encompasses the personal knowledge and competencies that individuals accumulate through their daily activities, social interactions, and across generations. Health literacy enables people to access, understand, and utilise information and services that promote and maintain good health. This includes knowledge about health promotion, disease prevention, mental health, nutrition, physical activity, and the healthcare system.

Active learning programs have been shown to promote a healthy lifestyle among older adults with low health literacy. These programs focus on behaviour change, diet, education, and mobility, empowering individuals to take control of their health and make positive changes. For example, a study among older adults with low health literacy found that an active learning program improved their communicative health literacy, step count, engagement in physical activity, dietary variety, social network size, and grip strength, among other outcomes.

Health IQ is an insurance company that recognises the link between health literacy and active lifestyle, offering rates that are up to 41% lower for individuals who demonstrate healthy behaviours. They take into account factors such as BMI, total cholesterol, and heart rate, rewarding individuals for their healthy lifestyle choices rather than solely relying on traditional insurance risk factors.

Additionally, MotivHealth is an insurance company that aims to make healthcare more affordable and accessible. They offer HSA-based insurance plans with lower premiums and enhanced benefits, helping members save on healthcare expenses. MotivHealth also provides tools like SmartPay, which allows members to compare prices before choosing care, and MotivRx, which has eliminated out-of-pocket prescription costs for many members.

In conclusion, health literacy and an active lifestyle are crucial for maintaining good health and can even impact insurance rates. Active learning programs can effectively improve health literacy and promote healthier behaviours, empowering individuals to take charge of their health and make informed decisions. Insurance companies like Health IQ and MotivHealth are revolutionising the industry by rewarding healthy lifestyles and providing more affordable and accessible healthcare options.

Progressive Auto Insurance: ID Numbers Explained

You may want to see also

Explore related products

![]()

Poor family history

A poor family history can be a powerful motivator for healthy behaviour. While a family history of illness can impact insurance rates, some providers will reduce the chance of penalisation if you are otherwise healthy.

During the life insurance application process, you will be asked to provide information about your personal medical history and your family's health history. This is because an early death in your family or a diagnosis of a genetic condition could increase your insurance risk.

The most common health conditions that insurance providers ask about include cancer (especially breast, colon, lung, melanoma, and prostate cancer), heart disease, kidney disease, and diabetes. If a parent or sibling has passed away from one of these issues, you will likely pay more for your insurance premiums. Insurance companies will also take into consideration how many family members were affected by the condition and their age when it was diagnosed.

If you have a rare hereditary condition in your family, an insurer might ask your consent to contact your healthcare professionals to find out more information before deciding on cover. They may also ask you to consent to a medical examination by their own expert.

It is important to be honest and open about your personal and family medical history. If you are found to have lied or omitted details, this will invalidate your insurance and it will not pay out.

Carvana: Gap Insurance Included?

You may want to see also

Explore related products

![]()

BMI buffer

Health IQ is a company that combines an individual's current health, health literacy, and active lifestyle to better predict their long-term health. The company offers insurance rates that are up to 41% lower than average. Health IQ also takes into account other factors that are not considered by traditional insurance companies.

One such factor is an individual's Body Mass Index (BMI). BMI is a calculated measure of weight relative to height. It is often used as a health indicator and is categorized into underweight, healthy weight, overweight, and obesity. Obesity, in turn, is further divided into three classes. However, BMI does not differentiate between muscle and fat. This leads to misclassification, especially for athletes with above-average muscle mass, who may be categorized into weight classes considered risky by insurance companies.

Health IQ has introduced a "BMI buffer" to address this issue. The BMI buffer allows health-conscious individuals with above-average muscle mass to be eligible for preferred insurance rates, even if their BMI falls outside the standard range. For example, an individual who is 5'9" tall and weighs 208 lbs may still qualify for the preferred plus rate category, which typically has an upper weight limit of 198 lbs.

Another factor considered by Health IQ is an individual's resting heart rate. Endurance athletes often have lower resting heart rates, which can be misinterpreted by insurance companies as a heart abnormality. Health IQ recognizes that a low resting heart rate is a sign of good health and fitness in athletes and offers rates that account for this.

Gap Insurance: Why You Still Owe

You may want to see also

Explore related products

![]()

Low resting heart rate

A low resting heart rate is generally a sign of good health and fitness. It is common among physically active adults and athletes, who often have a resting heart rate slower than 60 BPM. This is because their hearts are more efficient at pumping oxygenated blood around the body, requiring fewer beats per minute.

However, a very low resting heart rate can sometimes be a cause for concern. The American Heart Association defines bradycardia as a heart rate that is too slow, which may be caused by problems in the heart's electrical conduction pathways, metabolic issues such as hypothyroidism, or damage to the heart from ageing, disease, or attack. Certain medications can also cause bradycardia as a side effect. Symptoms of bradycardia include nausea, dizziness, and heart palpitations, and it can result in insufficient blood flow to the brain. Treatment for bradycardia depends on its cause and severity and may include medication adjustments or the use of a temporary pacemaker.

It is important to note that a low resting heart rate can sometimes be misinterpreted by insurance companies as a heart abnormality. This is because the height/weight ratio used for BMI does not differentiate between muscle and fat mass, leading to the misclassification of strength athletes into weight classes considered risky by the insurance industry. However, a low resting heart rate in an athlete is generally a positive indicator of health and longevity. Studies have shown that runners have a 30% lower risk of overall death, with older marathon runners experiencing up to a 50% decreased risk of heart disease.

Overall, while a low resting heart rate is typically a sign of good health, it is important to consult with a medical professional if you have any concerns or experience any symptoms of bradycardia.

Lemonade: Auto Insurance Available?

You may want to see also

Explore related products

![]()

Health insurance reward programs

These programs are relatively new to individual plans on the Affordable Care Act (ACA) marketplaces, but they are becoming more popular. More insurance carriers are offering these programs to keep members healthy and reduce healthcare costs. Health insurance companies offer these programs at no additional cost, and they help keep existing customers happy and engaged while attracting new ones.

There are various types of health insurance rewards programs, and each has unique awards, activities, and restrictions. For example, policyholders may receive a $50 e-gift card after completing a personal health assessment on their insurer's secure portal. They can also earn up to $100 annually by hitting their daily step goals after syncing a step tracker with their insurance company's mobile app. Some programs offer reduced monthly premiums, cash rewards, prepaid debit cards, gift cards, or rewards cards that members can use to buy merchandise.

UnitedHealthcare, for instance, offers programs like Renew Active, which provides support and motivation to help keep members' minds and bodies active and healthy. Members can earn rewards for reaching activity and health goals. Similarly, MotivHealth offers HSA-based insurance plans that produce lower premiums, better benefits, and significant health savings for members. They also have programs like SmartPay, which allows members to compare prices before choosing care, and MotivRx, which has eliminated out-of-pocket prescription costs for thousands.

Primary Driver: Insurance Implications and Considerations

You may want to see also

![Pampers Baby Wipes, Sensitive, Water Based Wipe, Clinically Proven, Hypoallergenic, and Unscented for Babies, 1344 Wipes Total (16 Flip-Top Packs) [Packaging May Vary]](https://m.media-amazon.com/images/I/71r5y9tRDPL._AC_UL320_.jpg)