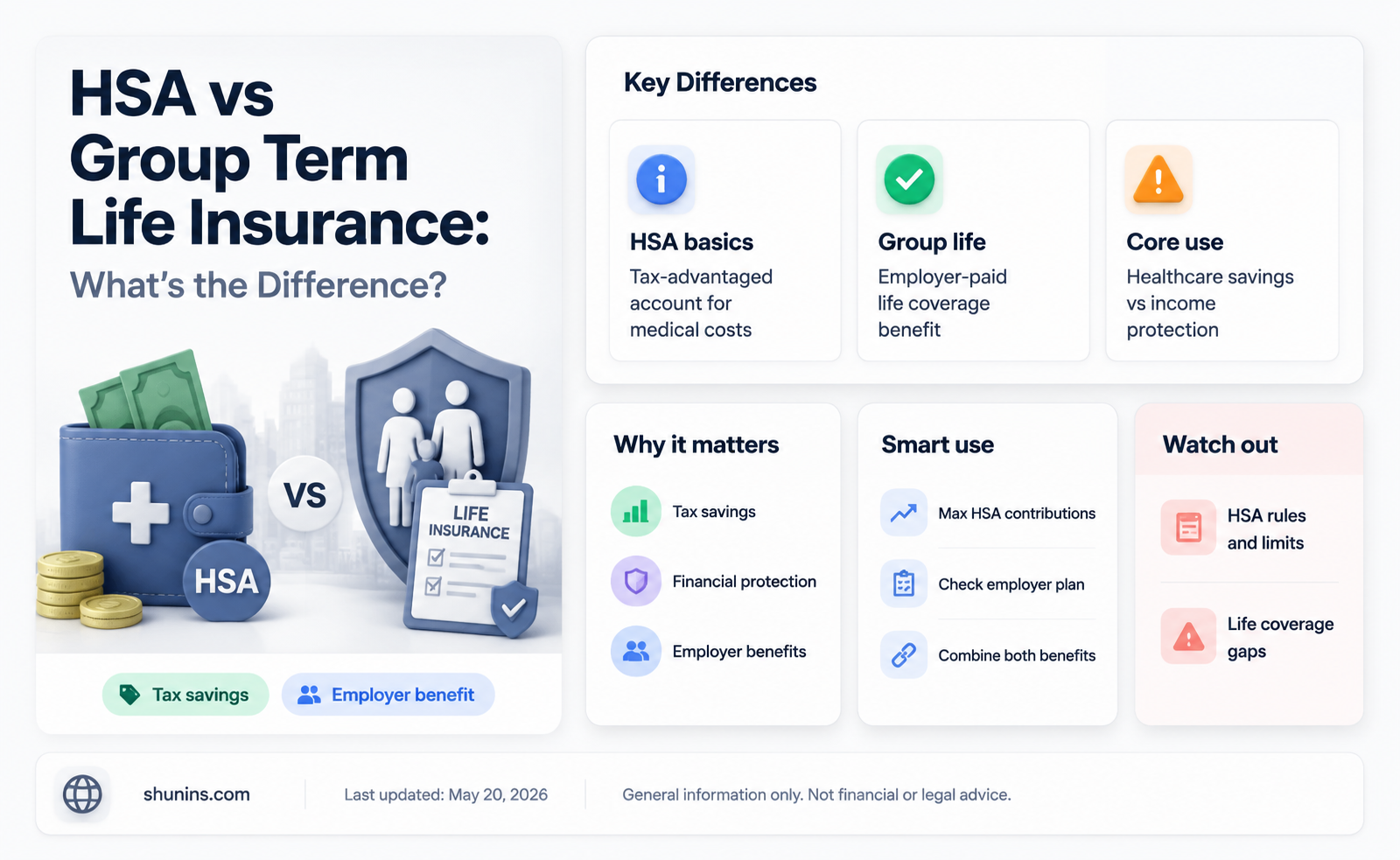

Group term life insurance and health savings accounts (HSAs) are very different things. Group term life insurance is a type of insurance policy that covers a group of people, usually employees of a company or members of an organisation. It is typically offered as an employee benefit, with the employer paying most or all of the premiums. HSAs, on the other hand, are individual accounts that allow people to pay for certain medical expenses, including some insurance premiums, with tax-free funds. While group term life insurance provides a death benefit to the insured's beneficiaries, an HSA is a tool for managing healthcare costs while potentially receiving tax benefits.

| Characteristics | Values |

|---|---|

| Type of Insurance | HSA is a health savings account, while group term life insurance is a type of life insurance. |

| Purpose | HSA is used to pay for medical expenses, while group term life insurance provides financial security to beneficiaries in the event of the insured's death. |

| Coverage | HSA covers medical costs, while group term life insurance provides a lump-sum payment to beneficiaries. |

| Tax Implications | HSA withdrawals for qualified medical expenses are often tax-free, while group term life insurance benefits may be taxable depending on the amount. |

| Ownership | HSA is owned by an individual, while group term life insurance is typically provided and owned by an employer or group. |

| Cost | HSA funds come from an individual's contributions, while group term life insurance is usually provided at no cost to employees, with premiums paid by the employer. |

| Portability | HSA is portable and can be used to pay for long-term care insurance, while group term life insurance may not be portable when changing jobs. |

Explore related products

What You'll Learn

![]()

Group term life insurance is a single contract that covers multiple people

Group term life insurance is a type of insurance that covers multiple people under a single contract. This type of insurance is typically offered by an employer to its employees as a benefit, although it can also be provided by other large-scale entities such as associations or labour organisations to their members. The employer or organisation purchases the policy and retains the master contract, while the covered individuals receive a certificate of coverage. This certificate is needed if the individual leaves the company or organisation and needs to provide proof of coverage to a subsequent insurance company.

Group term life insurance is a common employee benefit, with around two-thirds of Americans relying on it. It is usually offered as part of a larger benefits package and is relatively inexpensive compared to individual life insurance. In some cases, it may be provided to employees at no cost. The cost of coverage for each individual is much lower than if they were to purchase an individual policy.

The standard amount of coverage is usually tied to the covered employee's annual salary, with premiums primarily based on the insured's age. Employers typically pay most or all of the premiums for basic coverage, with the option for employees to purchase additional coverage for themselves and their families. This additional coverage is often available at a lower rate than individual policies and can be deducted directly from the employee's paycheck.

While group term life insurance is a valuable benefit, it has some limitations. The coverage amount is often relatively low and may not be sufficient to meet the financial needs of the insured's family. Additionally, the coverage is usually tied to employment, meaning that if an individual leaves their job, their coverage ends. However, some employers may allow former employees to maintain their coverage or convert their group policy to an individual policy, although this may result in higher premiums.

Life Insurance and the IRS: What Employees Need to Know

You may want to see also

Explore related products

![]()

It is a temporary type of insurance

A health savings account (HSA) is a tax-advantaged savings account that allows you to set aside money on a pre-tax basis to pay for qualified medical expenses. This means that you can save money in the account without being taxed on it, and you also won't be taxed when you take money out, as long as it's used for qualified medical expenses. You can only contribute to an HSA if you have an HSA-eligible plan, which is usually a health plan that only covers preventive services before the deductible.

Group term life insurance, on the other hand, is a type of temporary life insurance that is offered by an employer or another large-scale entity, such as an association or labor organization, to a group of people, usually its employees or members. It is typically inexpensive or even free for the individuals covered, and it provides a death benefit to each member's beneficiaries for a specific amount of time, such as 20 or 30 years.

Group term life insurance is a common benefit offered by employers, and it is often provided at a discounted rate or even for free. One of its key advantages is that individuals do not have to go through an underwriting process or medical exam to be covered, making it a popular choice for those who are medically unable to qualify for individual coverage. However, the amount of coverage offered by group term life insurance may not be sufficient for many families, and it is usually not portable, meaning that if an individual leaves the group, they will lose their coverage.

In summary, while both HSAs and group term life insurance offer financial benefits, they serve different purposes. HSAs are tax-advantaged savings accounts for medical expenses, while group term life insurance provides temporary coverage and a death benefit.

Term Life Insurance: Auto-Renewal and You

You may want to see also

Explore related products

![]()

It is often provided by an employer as part of an employee benefits package

Group term life insurance is often provided by an employer as part of an employee benefits package. It is a single contract that covers multiple people, usually a company's employees. This type of insurance is relatively inexpensive compared to individual life insurance, and it is often provided by employers at no cost to the employees. The cost of the premiums for basic coverage is typically paid for by the employer, with employees given the option to purchase additional coverage for themselves or their family members for an extra premium.

The standard amount of coverage is usually equal to the annual salary of each employee, though employers can choose different benefit levels, such as a flat amount like $50,000. The benefit is tax-free for the employee up to $50,000, with any amount over that being considered a taxable benefit.

Group term life insurance is a good benefit for employees, providing financial security and peace of mind, especially for those with families. It is also a valuable tool for employers to attract and retain talent. However, it is important to note that group term life insurance is not always portable, meaning that if an employee leaves their job, they may lose their coverage.

While group term life insurance is a valuable benefit, it may not provide sufficient coverage for all families. The amount of coverage offered may not be enough to meet the financial needs of the employee's loved ones in the event of their death. Therefore, it is often recommended to supplement this type of insurance with an individual life insurance policy.

Life Insurance and Grand Mal Seizures: What You Need to Know

You may want to see also

Explore related products

![]()

It is relatively inexpensive compared to individual life insurance

Group term life insurance is relatively inexpensive compared to individual life insurance. This is because group term life insurance is purchased by an employer or large-scale entity for a group of people, allowing them to secure costs for each individual that are much lower than if they were to purchase an individual policy. Typically, employers pay most or all of the premiums for basic coverage, with employees paying for any additional coverage. This means that group members pay very little, if anything at all, for their coverage.

Group term life insurance is also inexpensive because it does not require a medical exam or underwriting. All eligible employees are automatically covered, regardless of their health. This is in contrast to individual policies, which often require a medical exam and can be difficult to qualify for due to health issues.

The cost of group term life insurance is also kept low by the fact that it is usually temporary coverage, whereas individual life insurance policies are permanent. Group term life insurance is tied to employment, so coverage ends when an individual leaves their job. This means that the insurance company is not taking on the same level of risk as with a permanent policy.

Lastly, group term life insurance is often offered as a benefit by employers, who use it as a tool to attract and retain talent. By offering group term life insurance, employers can provide their employees with important financial security and peace of mind at a relatively low cost.

Life Insurance: Understanding Conversion Clause Benefits

You may want to see also

Explore related products

![]()

It is not always portable between jobs

Group life insurance is a single contract that provides coverage to a group of people, usually employees of the same company. It is often provided as a benefit by employers, but other large-scale entities such as associations or labor organizations may also offer it to their members.

Group life insurance is not always portable between jobs. Coverage is normally only valid for as long as a member is part of the group. Once the member leaves, whether through resignation or termination, the coverage ends. However, some insurance companies do offer the option to continue coverage by converting to an individual permanent life insurance policy. This means the policy is changed from a group life policy to an individual one, which comes with higher premiums. The new policy may also carry a much higher premium. The conversion options vary from plan to plan, may not be automatic, and could require underwriting.

If you are considering leaving your job, it is important to review your group life insurance policy carefully to understand your options for continuing coverage.

Exercise and Life Insurance: Is There a Catch?

You may want to see also

Frequently asked questions

Group term life insurance is a type of insurance that covers multiple people under a single contract. It is usually provided by an employer or a group such as a union. It is often included in employee benefits packages and is relatively inexpensive compared to individual life insurance.

Group term life insurance is offered by an employer or another large-scale entity to its workers or members. It is usually provided at no cost to the employee, but they may also have the option to buy additional coverage through payroll deductions. The insurance plan may also offer employees the option to buy coverage for their spouses and children.

Group term life insurance is inexpensive for companies and employees. It is easy to qualify for as there is usually no medical exam required, and all eligible employees are automatically enrolled. It can also provide important financial security and peace of mind for employees and their families.

Group term life insurance generally offers only basic coverage, which may not be sufficient for the policyholder's needs. It is also not portable, meaning that if an employee leaves their job, they will likely lose their coverage.

Yes, it may be prudent to have both types of policies at the same time. Group term life insurance may not provide a sufficient death benefit to meet all your family's financial needs, so combining it with an individual policy can ensure you have adequate coverage.