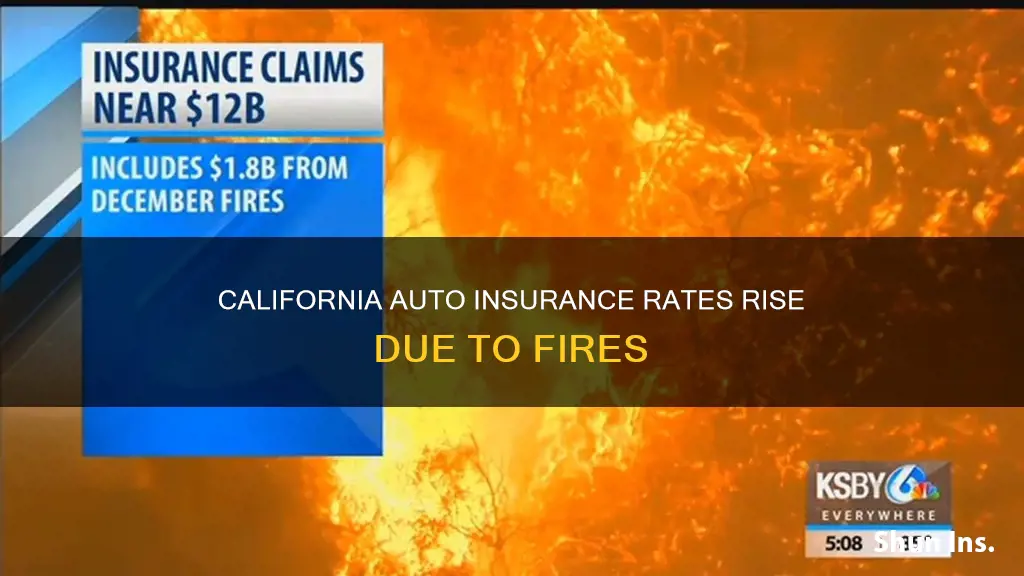

California's insurance crisis has led to cancelled policies and increased rates for customers. The state's insurance department has approved a total of 111 rate increases so far this year, with 58 of those from requests filed in 2023. The average premium for full-coverage auto insurance in California is $2,110 per year, compared to the national average of $1,583. The rising costs of insurance are attributed to increased liability due to inflation, climate change risk, and the high costs of car repairs.

Explore related products

What You'll Learn

![]()

California's insurance crisis

California is facing an insurance crisis, with customers experiencing cancelled policies, higher rates, and delays in obtaining new coverage. This crisis is affecting both homeowners and drivers, with auto insurance rates increasing across the state.

The Impact on Homeowners

Homeowners in California are finding it increasingly difficult or even impossible to maintain insurance coverage for their properties due to skyrocketing rates and policy cancellations. Many customers, such as Steve Besbeck, have been dropped by their insurance companies after years of loyal service. Besbeck, for example, had to switch to the California FAIR plan for fire coverage, which is intended for homeowners who are unable to find insurance through traditional means. Even with this alternative, Besbeck faced a 30% increase in his premium year over year.

The Impact on Drivers

Drivers in California are also facing challenges when it comes to auto insurance. They are encountering delays in obtaining coverage and higher premiums. Willis Lai, a 36-year-old driver from the Bay Area, shared his experience of spending three weeks trying to find insurance for his new car. He contacted all the major insurance providers he could think of and ended up talking to multiple agents before finally securing a policy.

Factors Contributing to the Crisis

There are several factors contributing to California's insurance crisis:

- Wildfire Risks and Climate Change: Insurance companies have cited the increased risk of wildfires and the impacts of climate change as reasons for pulling out of the state or raising rates.

- Rising Costs: Insurers argue that their costs are rising, including the prices of cars and parts, repair costs, and construction costs. They claim that these increased expenses must be passed on to consumers through higher premiums.

- Regulatory Challenges: Insurance companies have criticised California's regulatory system as archaic and cumbersome, blaming it for hindering their ability to set rates that keep pace with inflation and the changing risk landscape.

- Pandemic-related Refunds: During the pandemic, insurers were required to refund a total of $2.5 billion to California drivers due to reduced driving and lower claims during lockdown periods. Insurers argue that these refunds have contributed to their financial strain and the need for rate increases now that driving habits have returned to pre-pandemic levels.

- Economic Realities: The economic climate, including inflation and supply chain disruptions, has impacted the insurance industry, leading to higher costs for both insurers and consumers.

Responses to the Crisis

In response to the insurance crisis, California's Department of Insurance is taking several actions:

- Investigating Complaints: The department is looking into complaints from consumers about higher premiums, delayed quotes, and questionable insurer behaviour.

- Setting New Regulations for Fire Insurance: With some of the biggest insurers pulling out of California due to wildfire risks, the department is working to address the issue of skyrocketing premiums for homeowners.

- Enforcing Regulations for Auto Insurance: The department has issued an enforcement bulletin to address complaints about auto insurers implementing waiting periods, using questionnaires, and employing other stalling tactics to delay providing coverage.

- Approving Rate Increases: While the department has been cautious about approving rate hikes, it has recently approved increases for several major insurers, including State Farm, Allstate, and Geico. These increases are expected to impact millions of Californians.

Automated Auto Insurance Payments: Afternoon Debit?

You may want to see also

Explore related products

![]()

The impact of wildfires

Wildfires in California have had a significant impact on insurance rates and availability, with some of the biggest insurers pulling out of the state due to increased risks and costs. This has resulted in skyrocketing premiums for homeowners, with some residents even being priced out of insurance altogether. The insurance crisis in California has led to a situation where residents are struggling to find affordable coverage, with long wait times and upfront payment requirements becoming common.

The state of California has taken steps to mitigate the impact of wildfires on insurance rates and availability. For example, Insurance Commissioner Ricardo Lara has implemented new regulations that allow insurers to use catastrophe models in rate-making, taking into account mitigation efforts such as home-hardening and creating defensible spaces. Additionally, lawmakers have introduced bills such as Senate Bill 1060 and Assembly Bill 2983, which aim to incorporate mitigation efforts into insurance companies' underwriting decisions and evaluate the effectiveness of these measures in improving insurance availability.

Despite these efforts, insurance companies argue that the state's cumbersome regulations and slow approval process for rate increases have made it difficult for them to keep up with rising costs. They claim that the lack of approved rate increases for over two years has resulted in financial strain, especially with the increasing frequency and severity of wildfires.

Insurance Gap: Covering a Month-Long Gap

You may want to see also

Explore related products

![]()

The role of the California Department of Insurance

The California Department of Insurance (CDI) is the largest consumer protection agency in the state. It was established in 1868 and is responsible for overseeing insurance regulations, enforcing statutes that mandate consumer protections, educating consumers, and fostering the stability of insurance markets in California. The CDI has the authority to license and regulate the rates and practices of insurance companies, agents, and brokers in the state. The department has over 1,300 employees dedicated to protecting consumer interests.

One of the key roles of the CDI is to ensure that insurance companies conduct their business in an honest, open, and fair manner. This includes regulating how insurance companies market and administer their policies, as well as reviewing proposed personal auto and homeowners insurance rates to ensure they are fair, reasonable, and adequate. The CDI also has the power to approve or deny requests from insurance companies to raise their rates. This process is meant to balance the need for insurance companies to remain solvent while also protecting consumers from excessive price increases.

The CDI also plays a crucial role in investigating and prosecuting insurance fraud. In the early 1900s, the California State Legislature transformed the CDI into a law enforcement agency by passing new anti-fraud insurance legislation. The department's Enforcement Branch is responsible for detecting, investigating, and arresting those who commit insurance fraud, protecting the public from economic loss and distress.

In addition, the CDI provides consumer education and outreach to help Californians understand their rights and make informed insurance decisions. They publish brochures, maintain a website, and participate in public events to educate consumers about insurance-related issues.

The current California Insurance Commissioner is Ricardo Lara, who has been at the forefront of several initiatives to protect California consumers, including ordering insurance companies to refund drivers during the COVID-19 pandemic and working to address the issue of rising insurance rates in the state.

Gap Insurance: Monthly Payment or One-Time Fee?

You may want to see also

Explore related products

![Fire Color Changing Packets,Color Fire Packets for Outdoor Campfires, Fire Pits, Fireplaces, Colorful Flames, Long Burn Time, Safe, Magic for Child [24Pack]](https://m.media-amazon.com/images/I/81Ri3X8DhkL._AC_UY218_.jpg)

![]()

The effect on consumers

California's insurance crisis is causing a lot of distress to consumers, with many customers being dropped by their insurance companies or facing higher rates. The crisis is affecting both homeowners and drivers, with coverage becoming more expensive and harder to obtain. This is due to a combination of factors, including wildfires, climate change, inflation, supply chain issues, and the high cost of cars and car repairs.

The impact on consumers has been significant. Many Californians are struggling to find affordable insurance, with some reporting delays, higher premiums, and difficulties in obtaining quotes from insurers. The situation is made worse by the fact that some insurance companies have pulled out of the state entirely due to the regulatory environment and the high costs of doing business in California. This has resulted in a reduced choice of insurers for consumers and, in some cases, the need to turn to the California FAIR plan, which offers bare-bones coverage for high-risk properties.

The insurance department's approval of rate increases has added to the burden on consumers. In 2023, the department approved 111 rate increases, with 58 of those coming from requests filed that year. The approved rate increases averaged 13.2%, compared to 10.6% in 2019 before the pandemic. The highest auto premium increase approved so far is a 62% hike from Root Insurance. These increases are expected to cost consumers hundreds of dollars more per person each year.

The situation is particularly challenging for those with higher-risk profiles, such as high-risk drivers or homeowners in wildfire-prone areas. For example, a single driver with less than four years of experience could pay anywhere from $2,000 to almost $20,000 a year for car insurance. Similarly, insurance policy costs for homeowners have increased steadily, with some customers reporting increases of 30% year over year.

The insurance crisis has also led to confusion and frustration among consumers, with reports of insurers using stalling tactics, such as waiting periods and questionnaires, to slow down the process of obtaining coverage. Some consumers have also expressed concerns about the lack of transparency and consistency in the quotes they receive from insurers.

Overall, the insurance crisis in California has had a significant impact on consumers, resulting in higher costs, reduced choices, and increased difficulties in obtaining coverage. While the state's regulations are intended to protect consumers from excessive price increases, the current situation highlights the challenges of balancing the needs of insurance companies with the needs of consumers.

Vehicle Loan and No Insurance: What Now?

You may want to see also

Explore related products

![]()

The future of insurance in California

California's insurance market is in a state of flux, with rising costs, an increasing number of natural disasters, and regulatory challenges all contributing to a challenging environment for insurers and consumers alike. The future of insurance in the state will depend on how these various factors play out in the coming years.

One of the key issues facing the insurance industry in California is the impact of natural disasters, particularly wildfires. In recent years, some of the biggest insurers have pulled out of the state, citing increased wildfire risks. This has led to skyrocketing premiums for homeowners, with some reporting increases of up to 30% year-over-year. The situation has become so dire that Governor Gavin Newsom has stepped in, directing the insurance commissioner to find a solution to the problem.

At the same time, auto insurance rates have also been on the rise in California. Several major insurers have sought and been granted premium increases by the state's Department of Insurance. These rate hikes have been driven by a variety of factors, including inflation, supply chain disruptions, and the high cost of car repairs. The average premium for full-coverage auto insurance in California is now $2,110 per year, significantly higher than the national average of $1,583.

The regulatory environment in California is also a key factor shaping the future of the insurance industry in the state. California has some of the strictest insurance regulations in the country, including Proposition 103, which requires hearings for any personal insurance rate increase requests above 7%. This has led to a backlog of rate increase requests, as insurers are reluctant to trigger a hearing by asking for an increase above 7%.

In response to the challenges facing the insurance industry in California, some insurers have called for deregulation, arguing that the current regulatory system is archaic and does not adequately account for the increased risks posed by inflation and climate change. However, consumer advocacy groups have pushed back against these calls, arguing that deregulation would lead to even higher rates for consumers.

Looking ahead, it is likely that insurance rates in California will continue to rise, particularly in areas affected by wildfires and other natural disasters. The state's insurance department will play a key role in balancing the needs of insurers and consumers, ensuring that rates are high enough to keep insurers solvent while also protecting consumers from excessive price increases.

In the meantime, consumers in California are encouraged to shop around for the best rates and take advantage of any discounts they may be eligible for. While the insurance market in the state is challenging, there are still options available for those seeking coverage.

Beneficiary Basics: Vehicle Insurance

You may want to see also

Frequently asked questions

Yes, insurance companies can raise auto rates in California because of fires. California regulates insurance companies and their rate increases, so some insurance companies have pulled out of the state.

The average cost of car insurance in California varies depending on the source. According to Credit Karma, the average cost is $265 per year. USAToday estimates an average of $2,476 per year, while NerdWallet puts the average at $1,659.

Auto insurance rates are increasing in California due to rising repair costs, inflation, supply chain disruption, new car technology, and the return to pre-pandemic driving routines.

California drivers can shop around for the best rates by getting quotes from different companies and looking for discounts such as bundling home and auto insurance, paying premiums upfront, taking a defensive driving course, or qualifying for good driver or good student discounts.