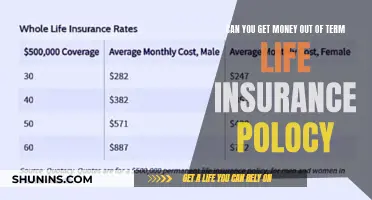

Life insurance companies evaluate an applicant's health and lifestyle when offering a rate, and weight is one of the factors they consider. While being overweight doesn't automatically disqualify you from getting life insurance, it might affect your rate and the type of policy you qualify for. Life insurance companies use height-to-weight ratios to determine whether someone is overweight or obese, and this, in turn, helps them assess whether the applicant might be a high-risk applicant.

| Characteristics | Values |

|---|---|

| Can you get life insurance if you're overweight? | Yes, but it might affect your rate and the type of policy you qualify for. |

| How do insurers determine your rating category? | Insurers use a build chart that's similar to a BMI calculation. |

| What are the rating categories? | Preferred Plus, Preferred, Standard Plus, Standard, Table Ratings |

| What are the characteristics of each rating category? | Preferred Plus: Excellent health with no history of medical issues. Preferred: Minor medical issue or a family history of moderate conditions but otherwise in great health. Standard Plus: Good health with a negative family history or a single condition. Standard: Average health with a couple of common but manageable issues. Table Ratings: High-risk applicants. |

| What are the weight limits for each rating category? | It depends on the insurer and policy, but generally, Preferred Plus is for those within a few pounds of their ideal weight. |

| Are there exceptions to the weight and BMI guidelines? | Yes, insurers may make exceptions for athletes or fit people with a high chest-to-waist ratio. |

| How can you get the best life insurance rates if you're overweight? | Be honest about your health and lifestyle, follow a healthy diet and exercise program, and be monitored by your doctor regularly. |

| What are weight-related life insurance application questions? | Current weight and height, weight changes in the past year, smoking status, last doctor's appointment, and any health or mobility issues related to weight. |

| What is the impact of weight loss on life insurance rates? | Losing weight can improve your rating, but insurers focus on longer-term weight trends rather than recent weight loss. |

| Can you be denied life insurance due to your weight? | You're unlikely to be denied coverage solely due to your weight, but you may be denied if you have serious health complications related to your weight. |

| What are the alternatives if you can't get standard life insurance due to your weight? | Guaranteed acceptance life insurance policies offer limited coverage at a higher cost, with partial payouts for non-accidental deaths within the first few years. |

Explore related products

What You'll Learn

![]()

How weight impacts life insurance rates

Life insurance companies evaluate an applicant's health and lifestyle to determine their eligibility and risk. While being overweight doesn't automatically disqualify you from getting life insurance, it might affect your rate and the type of policy you qualify for.

Insurers group applicants into rate classes based on their health, such as standard, preferred or super preferred. The name given to each class can vary among insurers, but the goal is the same: to categorize the risk of insuring you based on your life expectancy.

Insurance companies determine your rating category and the price you pay. They base it in part on a build chart that's similar to a BMI (body mass index) calculation. Typically, the rating categories are:

- Preferred Plus: People in excellent health with no history of medical issues. If you're over the ideal weight for your height by more than a few pounds, you're unlikely to receive this rating.

- Preferred: If you have had a minor medical issue or a family history of moderate conditions, but are otherwise in great health, you'll likely qualify for a Preferred rating. There's often a Preferred category for smokers who would qualify for the best rates, except for their tobacco usage.

- Standard Plus: Typically includes people in good health who have a negative family history or a single condition that exempts them from qualifying for a Preferred rating.

- Standard: People of average health who may have a couple of common but manageable issues, such as high cholesterol or blood pressure. There's also a Standard rating for smokers. If you are overweight, and particularly if you are obese, you'll likely receive a Standard rating.

- Table Ratings: High-risk applicants. Unless you have a very high BMI, it's unlikely you'd receive a Table Rating for life insurance based on your weight alone.

Weight-Related Health Conditions

Having overweight or obesity can put you at higher risk of developing potentially life-shortening conditions, such as heart disease or diabetes. Even if you don't currently have one of these conditions, the company may not offer you a Preferred rating if you fall outside their recommended weight limits, because a high BMI increases your risk of a serious medical issue later.

How to Get the Best Life Insurance Rates if You Are Overweight

When applying for life insurance, be honest about your health and lifestyle, which the company will check against any medical records and exams. If you follow a healthy diet and a consistent exercise program, are monitored by your doctor on a regular basis and have had no weight-related health issues, you'll likely qualify for a good life insurance rating.

Weight Loss and Life Insurance Rates

If you intentionally lose weight in the 12 months before applying for a policy, you'll get better life insurance rates, but you'll probably only receive credit for half of the weight you've lost. Insurance companies want to know that your weight loss is sustained, so they focus on your longer weight trends, as opposed to a single snapshot.

Denial of Coverage Due to Weight

In most cases, you won't be denied life insurance coverage solely due to a high BMI. Even if one company refuses to cover you, another would likely offer you a policy. Failing to qualify for life insurance with multiple companies usually only happens if you are morbidly obese and have other health conditions.

Life Insurance and Suicidal Death: What's Covered?

You may want to see also

Explore related products

$43.3

![]()

Weight-related health complications

Heart Disease

Being overweight or obese increases the risk of heart disease by elevating blood pressure and cholesterol levels. This, in turn, increases the likelihood of a heart attack, angina, or an abnormal heart rhythm. Losing excess weight can help lower these risk factors.

Type 2 Diabetes

Nearly 9 in 10 people with type 2 diabetes are overweight or obese. Over time, high blood glucose resulting from this condition can lead to heart disease, stroke, kidney disease, eye problems, nerve damage, and other health issues. Losing weight can help prevent or delay the onset of type 2 diabetes.

High Blood Pressure

Carrying extra weight, especially around the waist, can lead to high blood pressure as the heart needs to work harder to pump blood throughout the body. High blood pressure strains the heart, damages blood vessels, and increases the risk of heart attack, stroke, and kidney disease. Losing weight can help lower blood pressure and prevent related health issues.

Stroke

Being overweight or obese increases the risk of stroke as it is a leading cause of high blood pressure, which is the primary cause of strokes. Losing weight can help lower blood pressure and reduce the risk of stroke.

Metabolic Syndrome

This syndrome is a group of conditions, including high triglyceride levels, high blood glucose, and low HDL ("good") cholesterol levels, that increase the risk of heart disease, diabetes, and stroke. Weight loss and healthy lifestyle changes can help prevent and reduce metabolic syndrome.

Fatty Liver Diseases

Nonalcoholic fatty liver disease (NAFLD) and nonalcoholic steatohepatitis (NASH) are more common in people who are overweight or obese. Losing weight can help reduce fat in the liver and lower the risk of severe liver damage, cirrhosis, or liver failure.

Cancer

Being overweight or obese may increase the risk of certain types of cancer, such as colon, rectum, prostate, breast, uterus, and gallbladder cancers. Maintaining a healthy weight can help lower the risk of these cancers.

Respiratory Issues

Excess weight can affect lung function and increase the risk of breathing problems, such as asthma and sleep apnea. Losing weight can improve asthma symptoms and reduce the severity of sleep apnea.

Osteoarthritis

Obesity is a leading risk factor for osteoarthritis, especially in weight-bearing joints like the knees, hips, and ankles. Losing weight can decrease stress on these joints and reduce inflammation, improving osteoarthritis symptoms.

Gallbladder and Pancreas Issues

Being overweight or obese increases the risk of gallbladder diseases, such as gallstones and cholecystitis, as well as inflammation of the pancreas (pancreatitis). Weight loss can help lower the risk of these conditions.

Kidney Disease

Obesity increases the risk of diabetes and high blood pressure, which are the most common causes of chronic kidney disease. Losing weight can help prevent or delay the progression of kidney disease.

Pregnancy Complications

Overweight and obese women are at higher risk of developing gestational diabetes, preeclampsia, requiring a caesarean delivery, and experiencing complications during pregnancy. Losing weight before pregnancy can help reduce these risks.

Infertility

Obesity has been linked to lower sperm count and quality in men and menstrual cycle and ovulation issues in women, making it more difficult to conceive. Losing weight can improve fertility and increase the chances of a healthy pregnancy.

Sexual Function Problems

Obesity has been associated with an increased risk of sexual dysfunction in both men and women. Weight loss, healthy eating, and increased physical activity can help reduce these issues.

Mental Health Problems

Being overweight or obese can impact mental health and increase the risk of depression, affecting quality of life and self-esteem. Losing weight can improve body image, self-esteem, and reduce symptoms of depression.

Paid-Up Additions: Life Insurance's Bonus Feature Explained

You may want to see also

Explore related products

![]()

BMI and weight limits

Life insurance companies use a variety of methods to determine an applicant's risk profile, including their Body Mass Index (BMI). They will compare your BMI against their own "build chart" to determine how your BMI will affect your eligibility and rate. While there is no industry standard for how insurers use BMI to make application decisions and determine rates, they will also take into account your age, sex, and other health factors.

The higher your BMI, the more your life insurance is likely to cost, but the cutoff point and other factors for each rating category vary between companies. For example, a 200-pound man who is considered overweight might get a "Preferred" rating from John Hancock but a "Standard" rating from Primerica.

Insurance companies may make exceptions to their weight and BMI guidelines for athletes or fit people with a high chest-to-waist ratio. The weight tables are only approximate guidelines, as companies don't want to exclude people who are very fit despite having a high BMI. If there's a healthy reason for your high BMI, notify the company when applying so they can confirm whether you qualify for a "Preferred" rating.

BMI categories

According to the National Heart, Lung, and Blood Institute, the BMI categories are as follows:

- Underweight: Below 18.5

- Healthy weight: 18.4–24.9

- Overweight: 25.0–29.9

- Obese: 30 and above

How BMI affects life insurance rates

Insurance companies determine your rating category and the price you pay. They base it in part on a build chart that's similar to a BMI calculation. The rating categories are typically as follows:

- Preferred Plus: People in excellent health with no history of medical issues. If you're over the ideal weight for your height by more than a few pounds, you're unlikely to receive this rating.

- Preferred: If you have had a minor medical issue or a family history of moderate conditions but are otherwise in great health, you'll likely qualify for a "Preferred" rating. There's often a "Preferred" category for smokers who would qualify for the best rates except for their tobacco usage.

- Standard Plus: Typically includes people in good health who have a negative family history or a single condition that exempts them from qualifying for a "Preferred" rating.

- Standard: People of average health who may have a couple of common but manageable issues, such as high cholesterol or blood pressure. There's also a "Standard" rating for smokers. If you are overweight, and particularly if you are obese, you'll likely receive a "Standard" rating.

- Table Ratings: High-risk applicants. Unless you have a very high BMI, it's unlikely you'd receive a "Table Rating" for life insurance based on your weight alone.

Weight-related life insurance application questions

When applying for life insurance, you will be asked about your health and lifestyle, which the company will check against any medical records and exams. Be honest about your current weight and height, but make sure to include any other relevant information. For instance, if you have a high BMI but a particularly low body fat percentage, the company may give you credits and improve your rating.

You will also be asked about weight changes in the past year. A crash diet is unlikely to help you get the best life insurance rating, as companies get concerned about sudden changes in weight. They will only credit you with half of any recent weight loss. However, if you've begun an exercise or diet regimen that has helped you start to lose weight, make sure you disclose this in your application, even if the company doesn't specifically ask about it.

What to do if you're denied life insurance due to your weight

In most cases, you won't be denied life insurance coverage solely due to a high BMI. Even if one company refuses to cover you, another would likely offer you a policy. Failing to qualify for life insurance with multiple companies usually only happens if you have morbid obesity and other health conditions.

If you can't get a standard term or permanent life insurance policy due to issues linked to your BMI, try losing weight and then reapplying for coverage. Even though life insurance companies will only give you partial credit for major weight loss in the previous 12 months, you're more likely to qualify for the policy of your choice.

If you need coverage immediately and are unable to qualify elsewhere, you may want to consider a guaranteed acceptance life insurance policy. However, these policies tend to be more expensive and provide very limited coverage—usually no more than $25,000. They also come with a graded benefit, meaning that if you die of natural causes within a few years of buying the policy, your beneficiaries will only receive a partial payout.

Contacting ReliaStar: A Guide to Reaching Their Life Insurance Team

You may want to see also

Explore related products

![]()

Getting denied life insurance for being overweight

Getting Denied Life Insurance Due to Weight

While it is rare to be denied life insurance coverage based on weight alone, it can happen. If you are denied life insurance due to your weight, it is likely that you have other health issues or complicating factors such as a pre-existing condition, risky hobbies, or a history of smoking.

What to Do if You're Denied Life Insurance Due to Your Weight

If you are denied life insurance due to your weight, there are a few things you can do:

- Lose weight and reapply: If you can't get a standard term or permanent life insurance policy due to your weight, losing weight and then reapplying for coverage may help. Even though life insurance companies will only give you partial credit for major weight loss in the previous 12 months, you're more likely to qualify for the policy of your choice.

- Consider a guaranteed acceptance life insurance policy: These policies guarantee acceptance regardless of weight, but they have limited coverage (usually no more than $25,000) and are more expensive than standard life insurance policies per dollar of coverage. They also come with a two- to three-year waiting period during which your beneficiaries would only receive a partial payout unless the death was accidental.

- Explore alternative options: If you need coverage immediately but are unable to qualify for a standard policy, consider alternative options such as group life insurance through your employer or accidental death and dismemberment insurance.

Tips for Buying Life Insurance if You're Overweight

- Be honest about your weight: Intentionally lying about your weight on a life insurance application could result in your application being denied for misrepresentation.

- Provide additional context: If you have a high BMI but a low body fat percentage, be sure to include this information in your application. The insurance company may give you credits and improve your rating.

- Disclose weight loss: If you've recently lost weight through a diet and exercise regimen, be sure to disclose this in your application, even if the company doesn't specifically ask about it.

- Don't crash diet: A crash diet is unlikely to help you get the best life insurance rating, and sudden weight loss may be seen as a point of concern. Companies are more interested in sustained weight loss.

- Work with an independent agent: An independent agent can help you compare quotes and find the best coverage and pricing for your medical condition.

PPI and Life Insurance: Are You Covered?

You may want to see also

Explore related products

![]()

Strategies for obtaining affordable coverage

If you are considered overweight or obese, you may face challenges in finding affordable life insurance coverage. Here are some strategies that may help you obtain a more favourable policy:

Work with an Independent Agent

An independent life insurance agent will be knowledgeable about which companies are more accommodating towards overweight and obese applicants. They can generate multiple quotes from different providers, giving you a comprehensive view of your options. These agents are also likely to know which insurers specialise in high-risk policies, increasing the likelihood of your application being accepted at a reasonable rate.

Shop Around for Quotes

If you prefer to do your own research, there are numerous resources available to help you find the most affordable life insurance. However, it is important to consider not just the price but also the customer service ratings, financial stability, and range of policy offerings of each insurer.

Look into Group Insurance

If your employer offers group life coverage, this may be a more affordable option for you, especially if you work in a high-risk occupation. Employers sometimes offer a small amount of life insurance coverage at no cost, but this may not be sufficient for your needs, and you may need to purchase an additional policy.

Be Mindful of Your Health

If you are accepted for coverage but are charged a high rate, you can ask for a re-evaluation of your health rating if your condition improves. Losing weight, especially in combination with other positive health changes, can help you obtain a better rate. However, insurers want to see sustained weight loss, so they will look at your overall health history rather than just a snapshot of your current weight.

Trustage Life Insurance: Legit or a Scam?

You may want to see also

Frequently asked questions

A preferred rate is a classification for applicants who may have some minor personal or family health concerns but are otherwise in good health. There is often flexibility around weight allowances in this category.

The standard rate is the category that the average American falls into. This refers to having average health and some general health concerns.

A substandard rate is for high-risk applicants who have significant health issues or lead a high-risk lifestyle. This category results in higher premiums.

Being overweight does not automatically disqualify you from getting life insurance. However, it might affect your rate and the type of policy you qualify for. If you have weight-related or other health complications, you may pay more for coverage.

Losing weight can help you get a preferred rate. However, insurers want to know that your weight loss is sustained, so they might focus on your weight trend instead of a single snapshot.