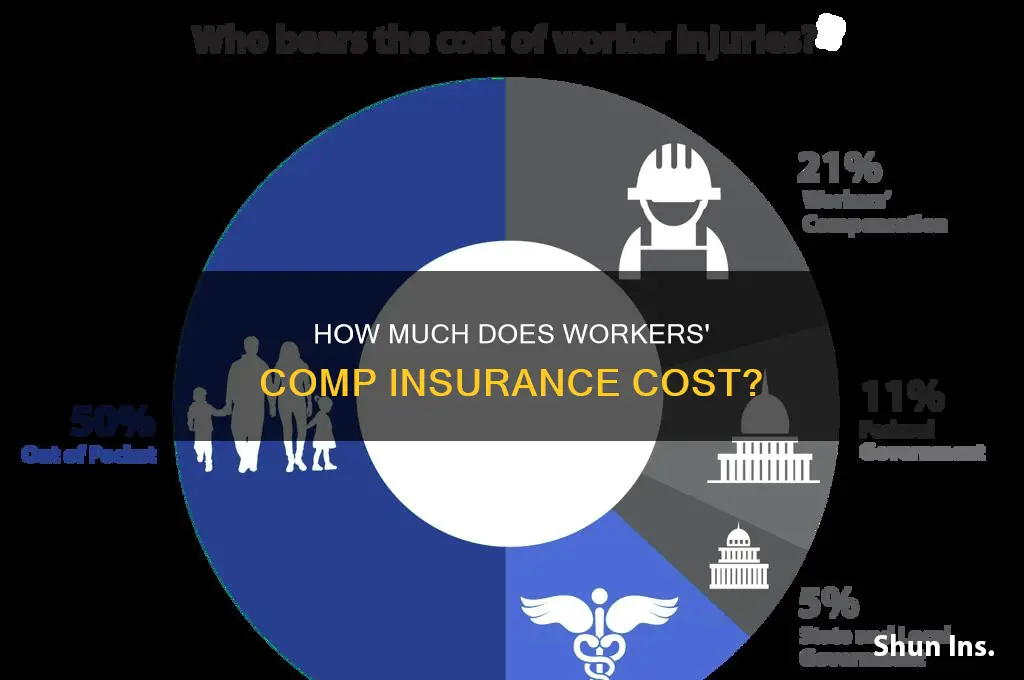

Workers' compensation insurance is an important aspect of doing business, as it provides protection for both employers and employees in the event of workplace injuries or illnesses. The cost of workers' compensation insurance varies depending on factors such as business size, location, industry, and claims history. While it can be expensive, employers can manage these costs by obtaining quotes from multiple insurance carriers, ensuring proper employee classification, and exploring alternative plans. Licensed insurance companies or state-run insurance funds typically provide this type of insurance, and it is available to businesses of various structures, including sole proprietorships and partnerships. Workers' compensation insurance is a long-standing social safety net, protecting workers and their dependents from financial devastation due to work-related injuries or illnesses.

| Characteristics | Values |

|---|---|

| Workers' compensation insurance rate | $0.50 for every $100 of payroll |

| Annual workers' compensation premium | $250 for a $50,000 payroll |

| Premium for workers' compensation insurance | Based on risk |

| Premium costs | Lower for employers with coverage from an insurance company that uses a network |

| Licensed insurance companies | Claims paid by the Texas Property and Casualty Guaranty Association if they become insolvent |

| Self-insurance | Allowed for large private employers |

| Self-insurance groups | Allowed, must be in the same or similar business and meet other requirements |

| Workers' compensation benefits | Medical care, temporary disability benefits, permanent disability benefits, supplemental job displacement benefits, and death benefits |

| Workplace safety training | Can affect insurance pricing |

Explore related products

$9.99 $31.95

What You'll Learn

- Workers' compensation insurance protects employers from lawsuits by injured employees

- Employers must purchase workers' compensation insurance from a licensed insurance company

- The cost of workers' compensation insurance depends on business size, location, industry, and claims history

- Workers' compensation insurance covers medical expenses and provides wage replacement for injured employees

- Employers can self-insure their workers' compensation claims by meeting certain requirements

![]()

Workers' compensation insurance protects employers from lawsuits by injured employees

Workers' compensation insurance is a state-mandated insurance program that provides benefits to employees who are injured or become ill due to job-related activities. It assures that injured workers get medical care and compensation for a portion of the income they lose while they are unable to return to work. It also usually protects employers from lawsuits by injured workers.

Workers' compensation insurance serves two purposes. Firstly, it ensures that injured workers get the medical care and compensation they need. Secondly, it protects employers from lawsuits by injured workers, providing protection from most lawsuits by injured employees. This means that injured employees cannot sue their employers for negligence, although there are some exceptions. For example, in Texas, if an employee died because of an employer's negligence, they can be sued.

By accepting workers' compensation benefits, employees typically relinquish their right to sue their employer for negligence. This concession helps protect both workers and employers. Employees give up further recourse in exchange for guaranteed compensation, while employers consent to a degree of liability while avoiding the potentially greater cost of a negligence lawsuit. This is known as a no-fault contract, where workers receive benefits regardless of who was at fault in the accident.

Workers' compensation insurance is required for all employers operating in states like Colorado, with limited exceptions. Employers are legally obligated to take reasonable care to ensure their workplaces are safe. However, accidents happen, and workers' compensation insurance provides coverage for these incidents. It covers injuries sustained on the workplace premises or anywhere else while the employee is acting in the "course and scope" of employment. This includes traffic accidents that occur when an employee is driving for work purposes, as well as workplace violence, terrorist attacks, and natural disasters.

Beneficiary and Life Insurance: Understanding the Key Differences

You may want to see also

Explore related products

![]()

Employers must purchase workers' compensation insurance from a licensed insurance company

Employers must purchase workers' compensation insurance to provide benefits like medical care for employees who are injured or become ill because of their jobs. It might also pay for some of their lost income. If an employee dies due to a work-related injury or illness, workers' compensation insurance covers burial expenses and provides benefits to the employee's family.

In the United States, workers' compensation insurance is mandatory for employers with at least one employee, including part-time, full-time, or family members. It is essential to purchase this insurance from a licensed insurance company, as it provides legal protection against most lawsuits by injured employees. If an employer does not provide workers' compensation coverage, they lose this legal protection, and an injured employee can sue over a workplace injury or illness.

Licensed insurance companies are certified by the state, and claims are guaranteed by entities like the Texas Property and Casualty Guaranty Association. This ensures that claims will be paid even if the insurance company becomes insolvent. On the other hand, unlicensed insurance companies do not offer the same protections, and alternative policies may have dollar and time limits, leaving employers financially vulnerable.

To verify if an insurance company is licensed, employers can refer to state resources, such as the Help Line provided by the Texas Department of Insurance or the California Department of Insurance website for those in California. Employers can also seek guidance from a licensed commercial broker-agent or casualty broker-agent to navigate the complexities of coverage eligibility and insurance rates.

While workers' compensation insurance is a requirement for most employers, there are some exceptions and variations to consider. For example, in certain states like Texas, private employers are not required to have this insurance, and large private employers may have the option to self-insure their workers' compensation claims. Additionally, contractors without employees can choose to reject coverage by meeting specific criteria and submitting the necessary forms.

Thai Life Insurance Commercials: Evoking Sadness for Attention

You may want to see also

Explore related products

![Auxiliary Interest Tables ... for the ... Calculation of Interest at Any Rate Per Annum, on $1, $10, $100, Etc., Up to $1,000,000 ... Comp. and Pub. by R. Reussner 1900 [Leather Bound]](https://m.media-amazon.com/images/I/617DLHXyzlL._AC_UY218_.jpg)

![]()

The cost of workers' compensation insurance depends on business size, location, industry, and claims history

The cost of workers' compensation insurance is dependent on a variety of factors, including business size, location, industry, and claims history.

Firstly, business size matters. The bigger the staff, the more it will cost for workers' comp coverage. This is because business payroll is part of the premium (annual cost) calculation. Jobs with higher levels of risk, such as those involving physical labour or machinery, will also result in higher workers' comp costs.

Secondly, location plays a role. The cost of workers' comp insurance is influenced by state regulations and the population of the area. For example, a business in a highly populated city will likely pay a higher premium than a business in a small town.

Thirdly, the industry a business operates in is significant. Some industries, such as construction, are inherently riskier and more prone to workers' compensation claims, resulting in higher premiums.

Lastly, claims history impacts the cost of workers' compensation insurance. Businesses with a track record of fewer or zero workers' comp claims will generally receive better rates. Conversely, a history of frequent and severe claims will lead to higher costs.

It is worth noting that workers' compensation insurance laws vary by state, and certain states, such as Colorado, mandate this insurance for all employers. Failure to carry insurance in these states can result in fines. Additionally, businesses with contractors must ensure that the contractors meet the necessary workers' compensation requirements.

Pacific Life Insurance: Mail Payment Reminders?

You may want to see also

Explore related products

![]()

Workers' compensation insurance covers medical expenses and provides wage replacement for injured employees

Workers' compensation insurance, also known as workman's comp, is a form of insurance that provides financial protection to employers and employees in the event of a work-related injury or illness. It is designed to cover medical expenses and provide wage replacement for injured employees, reducing the financial burden of workplace injuries.

In the United States, workers' compensation is a mandatory form of insurance for businesses with employees, although the specific requirements vary from state to state. For example, in Texas, workers' compensation insurance is not required by law, but it offers legal protection against lawsuits by injured employees. On the other hand, states like Colorado mandate workers' compensation insurance for all employers, with fines imposed for non-compliance.

Workers' comp insurance covers medical expenses related to work-related injuries or illnesses, including emergency room visits, surgeries, prescriptions, and ongoing care costs such as physical therapy. It also provides wage replacement for employees who need time off to recover, helping to mitigate the financial impact of lost income. Additionally, workers' compensation insurance can provide death benefits and funeral costs in the unfortunate event of a work-related fatality.

The cost of workers' compensation insurance is typically paid by the employer and can vary based on industry, occupational classifications of workers, and past claims experience. Large private employers may choose to self-insure their workers' compensation claims, provided they meet certain financial requirements. Alternatively, they can join a self-insurance group within the same or similar business.

Workers' compensation insurance is an essential safeguard for both employers and employees, providing peace of mind and financial security in the event of work-related injuries or illnesses. By understanding the requirements and benefits of workers' comp insurance, businesses can ensure they are compliant and offering the necessary protection to their employees.

Life Insurance Loans vs Dividends: What's the Difference?

You may want to see also

Explore related products

![]()

Employers can self-insure their workers' compensation claims by meeting certain requirements

In the United States, workers' compensation insurance requirements differ from state to state. While most states require employers to have workers' compensation insurance, some states allow employers to self-insure their workers' compensation claims by meeting specific requirements.

In Texas, large private employers have the option to self-insure their workers' compensation claims. To do so, they must obtain approval from the Division of Workers' Compensation (DWC) and demonstrate their financial capability to cover the costs of claims. Alternatively, employers can join a self-insurance group, which must be approved by the Texas Department of Insurance (TDI). Self-insured employers may establish their own health care networks or contract with existing ones to treat injured workers.

Similarly, in Alabama and Indiana, employers have the option to self-insure their workers' compensation claims. In Alabama, businesses must meet specific financial criteria, including a net worth of at least $5 million, positive income over the last three years, and an assets/liabilities ratio of one or greater. In Indiana, employers who fail to provide workers' compensation coverage or self-insurance may face civil and criminal penalties, including fines and potential jail time.

In New York, employers seeking to self-insure their workers' compensation claims must meet several requirements, including having three years of business experience, providing proof of current workers' compensation coverage, maintaining a safety program, and meeting specific financial criteria. Failure to meet the reporting and security deposit requirements may result in the termination of an employer's status as a self-insurer.

It is important to note that self-insuring workers' compensation claims is a significant financial responsibility for employers, and they should carefully consider their ability to cover the costs of potential claims. Additionally, requirements and regulations for self-insurance may vary by state, so employers should consult their state's specific guidelines to ensure compliance.

Life Insurance Apps: Why So Many Screens?

You may want to see also

Frequently asked questions

Workers' compensation insurance ensures that employees who suffer job-related illnesses and injuries can get medical care by covering the cost of medical expenses. It also covers wage replacement until they’re able to return to work.

The cost of workers' compensation insurance depends on the business size, location, industry, and claims history. The premium for workers' compensation insurance is based on risk. For example, a business with a $100,000 employee payroll and a workers' compensation insurance rate of $1.50 would mean that the business would pay $1,500 per year in workers' comp premiums.

The premium for workers' compensation insurance is calculated based on the business's annual employee payroll and workers' compensation insurance rate. The basic formula is: (Annual employee payroll/100) x workers' compensation insurance rate = estimated workers' compensation cost.

The cost of workers' compensation insurance is based on a classification system. All employers in the same industry with the same functions will have the same classification. These classifications are assigned workers' comp rates based on the history of occupational risk.

To estimate the cost of workers' compensation insurance, you can use the basic formula mentioned earlier. Additionally, you can get quotes from a variety of insurance carriers through your agent and discuss alternative plans and pricing options.