Life insurance is a necessity for most people, but do life insurance policies count towards net worth? The answer is: it depends. Net worth is calculated by subtracting the value of your liabilities (money owed) from your assets (things you own that have monetary value). While the death benefit of a life insurance policy is not considered an asset, some policies have a cash value that can be accessed and used for liquidity and estate planning. This cash value component is considered an asset and can increase your net worth. Term life insurance, which only pays out to dependents in the event of death, does not have a cash value and is therefore not counted towards net worth. On the other hand, whole life insurance and other types of permanent life insurance with a cash value component are considered assets and can boost your net worth.

| Characteristics | Values |

|---|---|

| Do life insurance policies count towards net worth? | Yes, life insurance policies are counted towards net worth. |

| What is net worth? | Net worth is the combined value of assets (things of monetary value that are owned) minus liabilities (accounts or loans that are being paid off). |

| What types of life insurance policies count towards net worth? | Only permanent life insurance policies, such as whole life insurance, are counted towards net worth as they can accumulate cash value over time. Term life insurance policies do not count as they do not accumulate cash value. |

| What is the benefit of life insurance policies that count towards net worth? | These policies can provide financial stability to families and beneficiaries, help with retirement savings, and assist in debt repayment. |

Explore related products

What You'll Learn

![]()

Life insurance as a financial asset

Life insurance is a necessity for most people, but only some types are classified as a financial asset. The primary goal of life insurance is to provide financial stability for your family or beneficiaries after you die. However, some policies have a cash value component, which is considered an asset.

Whether a life insurance policy is an asset depends on whether you can benefit financially from your policy while you’re alive. Term life insurance, which only pays out to your dependents in the event of your death, is not an asset. Whole life insurance and other types of permanent life insurance with a cash value component are considered assets because you can withdraw funds from your policy while you’re alive.

The death benefit of a life insurance policy is not considered an asset, but some policies have a cash value, which is. Only permanent life insurance policies, like whole life, can grow cash value. Some types of permanent life insurance have an additional living benefit, called cash value. If your life insurance policy accumulates cash value, the cash value is considered an asset because you can access it.

There are two main types of permanent life insurance that can be used as an asset: whole life insurance and universal life insurance. Whole life insurance is the most common type, which, in addition to a death benefit, offers the policyholder the ability to accumulate cash value. A portion of the premium you pay every month goes into a cash value account. Your cash value will accumulate over time at a minimum guaranteed rate indicated by your policy. The premiums on these policies typically won't increase over the life of the policy.

Universal life insurance functions similarly to whole life—they allow policyholders to grow an asset by accruing interest over time that can be borrowed against. However, the premiums aren't set and are subject to change, and there are no guarantees on the rate your money will earn over time. Under the universal life umbrella is variable universal life insurance, which enables policy owners to invest their earnings into the accounts of their choosing, so you have the potential to earn more over time.

Chest Pain: Can It Impact Your Life Insurance Eligibility?

You may want to see also

Explore related products

$33.99 $50

![]()

Life insurance and wealth building

Life insurance is often viewed as a crucial form of protection, helping family members cushion the financial impact of losing a loved one. However, it can also be used as an effective strategy to build wealth.

There are two main types of life insurance: term and permanent. Term life insurance covers the policyholder for a set period, typically 10 to 30 years, and pays out a death benefit if the insured dies within this time. Permanent life insurance, on the other hand, provides lifetime coverage and can be used as an investment tool to accumulate wealth.

One of the main advantages of permanent life insurance is that it can help you grow your wealth in a tax-efficient way. Unlike traditional investment portfolios, there is generally no taxation on growth within a permanent life insurance policy unless you withdraw money. This makes it a great option for investors looking to incorporate more tax-efficient options into their asset mix.

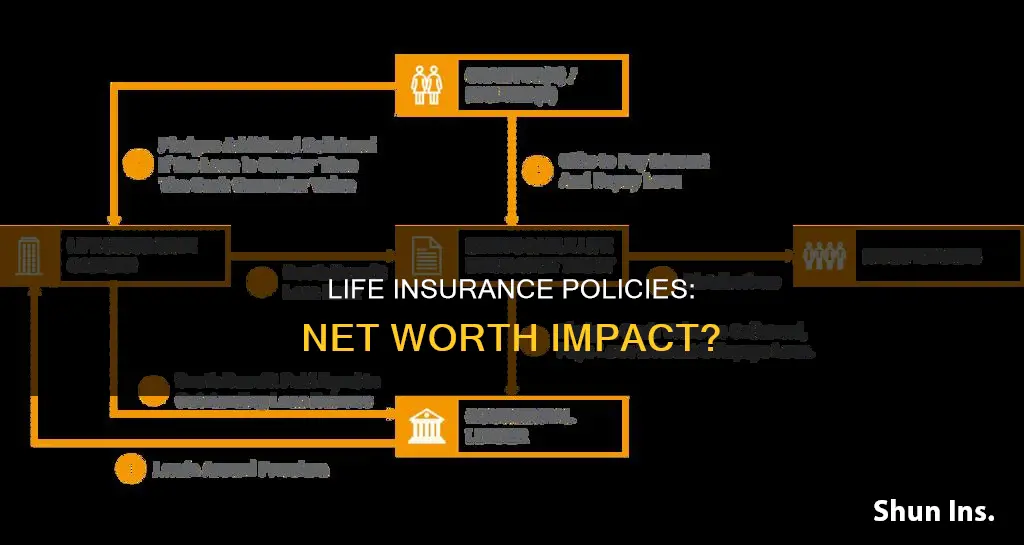

Another benefit of permanent life insurance is that it can provide supplemental retirement income. You can draw down on the cash value of your policy, although you would have to pay tax on this. Alternatively, you could use the cash value as collateral for a line of credit, which can provide income during retirement.

In addition, permanent life insurance can help you distribute wealth to your family in a tax-efficient manner. The death benefit payouts are typically not taxable, meaning your beneficiaries will receive the full amount. With permanent life insurance, you can also grow the money you want to leave to your loved ones over time, without having to pay taxes on that growth annually.

Permanent life insurance can also be a useful tool for business owners who want to capitalize on the wealth they have built up in their business or fund an eventual ownership transfer. It can also help protect assets from creditors in the event of a worst-case scenario.

However, it's important to consider the drawbacks of permanent life insurance. It requires higher premiums compared to term life coverage and can have tax implications if beneficiaries surrender coverage or if the insured dies with outstanding loans. Additionally, borrowing from the cash value or accessing accelerated benefits can reduce the payout amount.

In conclusion, while life insurance is primarily a form of protection for your loved ones, it can also be a valuable tool for wealth building, particularly when used in conjunction with other investment strategies.

Life Insurance: Maximizing Benefits for Peace of Mind

You may want to see also

Explore related products

$77.89 $89.99

![]()

Life insurance as a retirement savings tool

Life insurance can be used as a retirement savings tool, but it is not always the best option. The primary goal of life insurance is to provide financial stability for your family and beneficiaries after you die. However, some life insurance policies have a cash value component, which can be beneficial for retirement savings.

Term life insurance is the least expensive type of life insurance and does not accumulate cash value. It provides financial protection for a specified term, such as 10, 20, or 30 years, and has no investment component. On the other hand, permanent life insurance, such as whole life insurance and universal life insurance, offers a death benefit and also includes a savings component. Part of the premium payments goes towards the death benefit, while another portion builds up a cash-value account that grows on a tax-deferred basis.

The cash value within a permanent life insurance policy can be a useful source of funds during retirement. It can be withdrawn tax-free, up to the amount of the premiums paid, or borrowed against. However, withdrawals and loans will reduce the death benefit and cash surrender value. Additionally, loans will accrue interest.

While life insurance with a cash value component can be a way to save for retirement, it is important to consider the significant costs associated with these policies. Permanent life insurance policies tend to have high upfront costs, investment fees, and surrender charges. For this reason, life insurance as a retirement savings tool may primarily benefit wealthy individuals or those who have already maxed out other retirement savings options, such as 401(k)s and IRAs.

For most people, a dedicated retirement account, such as a 401(k) or IRA, will provide better returns than a permanent life insurance policy. These accounts offer tax advantages and higher contribution limits. Therefore, it is generally recommended to buy a simple term life insurance policy and invest any disposable income in tax-advantaged retirement accounts.

Navigating Life Insurance: Your Guide to Parent's Policies

You may want to see also

Explore related products

![]()

Life insurance for debt repayment assistance

Whether or not life insurance policies count towards net worth depends on the type of policy. Whole life insurance and other types of permanent life insurance with a cash value component are considered assets because you can withdraw funds from your policy while you're alive. On the other hand, term life insurance is not considered an asset because you can't benefit from it while you're alive.

Now, let's discuss life insurance for debt repayment assistance in more detail:

Life insurance can be a useful tool for debt repayment assistance, providing financial stability for your loved ones after your death. While debts are rarely inherited, there are instances when outstanding balances can become the responsibility of others, such as cosigners or joint owners of debt. Here's how life insurance can help:

- Mortgage debt: If someone cosigned your mortgage or is a co-borrower, they would typically be responsible for the debt if you pass away. By making them the beneficiary of your life insurance policy, they can use the payout to settle the debt and keep the house.

- Student loans: While student debt is often forgiven after death, there are cases where a cosigner may be responsible for private student loans. A life insurance payout can help cover the debt in your absence.

- Credit card debt: If you have a joint owner or cosigner on your credit card account, the remaining balance may become their responsibility. A life insurance policy can help them pay off the debt.

- Business loans: Life insurance can help your business partners pay off any loans they may be solely responsible for after your death. It can also fund a buy-sell agreement, allowing partners to buy out your stake in the company.

When considering life insurance for debt repayment assistance, you have two main options: term life insurance and permanent life insurance. Term life insurance is designed for temporary coverage over a set period, such as 10 or 20 years. Permanent life insurance, on the other hand, is open-ended and lasts your entire life. It includes policies such as whole life insurance and universal life insurance, which accumulate cash value over time. This cash value can be accessed while you're alive and used for various purposes, including debt repayment.

To decide which type of life insurance is best for your needs, consider the following:

- Duration of coverage: Term life insurance is sufficient for most families and is commonly used to cover debt. You can choose a term that matches the length of the loan, such as a 20-year term for a 20-year mortgage. Permanent life insurance, on the other hand, is designed to last your entire life and may be suitable if you want lifelong coverage.

- Cost: Term life insurance is generally more affordable than permanent life insurance, which tends to have higher premiums.

- Cash value: Permanent life insurance policies accumulate cash value, which can be accessed while you're alive. This feature provides flexibility and can be useful for debt repayment, but it also adds to the cost of the policy. Term life insurance does not accumulate cash value.

- Beneficiary flexibility: With term life insurance, the payout goes to your chosen beneficiary, who can use it for any purpose, including debt repayment. With permanent life insurance, the death benefit may be used specifically to pay off a particular debt, such as a mortgage.

In summary, life insurance can be a valuable tool for debt repayment assistance, especially when others may be responsible for your debts after your death. The type of life insurance you choose will depend on your specific needs, including the duration of coverage, cost, and flexibility in using the payout. It's always a good idea to consult a financial advisor to determine the best option for your unique situation.

Suing Life Insurance Brokers: Misleading Policy Information

You may want to see also

Explore related products

![]()

Life insurance for primary earners

Whether a life insurance policy is considered an asset depends on whether the policyholder can benefit financially from it while they are alive. Term life insurance, which only pays out to dependents in the event of the policyholder's death, is not considered an asset. In contrast, whole life insurance and other types of permanent life insurance with a cash value component are considered assets because the policyholder can withdraw funds from the policy while they are alive.

Life insurance is particularly important for primary earners, as it can provide financial stability for their family or beneficiaries after they are gone. It can help cover funeral and burial expenses, pay off remaining debts, and make managing daily living expenses less burdensome for those left behind. When determining the amount of coverage needed, it is important to consider the primary earner's current and future income, as well as any outstanding debts, such as mortgages, car loans, or credit card debt. The payout should be large enough to replace the primary earner's income and provide additional funds to hedge against inflation.

There are several types of life insurance policies available, each with its own benefits and drawbacks. Term life insurance is generally the most affordable option, providing coverage for a specific period, such as 10, 20, or 30 years. Whole life insurance offers lifelong coverage and guaranteed death benefits, but it is more expensive. Universal life insurance is also a form of permanent life insurance, offering flexible coverage and premiums but with fluctuating death benefits.

When choosing a life insurance policy, it is important to consider your financial goals and needs, as well as your age, health, and income stability. Consulting a financial advisor can help you make an informed decision about the type and amount of coverage that is right for you and your family.

Cancelling Colonial Life Insurance: A Step-by-Step Guide

You may want to see also

Frequently asked questions

Life insurance policies can be considered an asset that contributes to your net worth, but this depends on the type of policy. Term life insurance is not considered an asset as it does not accumulate cash value, whereas whole life insurance and other types of permanent life insurance with a cash value component are considered assets as you can withdraw funds while you are alive.

Term life insurance is designed for temporary coverage over a set period, usually 10-20 years, and does not accumulate cash value. Whole life insurance has a guaranteed death benefit that does not decrease, provided the premiums are paid, and the premiums themselves do not change over time.

Net worth is calculated by subtracting your liabilities (money owed) from your assets (things you own that have monetary value). Assets that count towards your net worth tend to be liquid assets, such as money in bank accounts, retirement accounts, and investments.