Out-of-pocket expenses are costs that an individual must pay for themselves, and they may or may not be reimbursed later. In the context of medical insurance, out-of-pocket expenses refer to the portion of medical costs that the insurance company does not cover. These expenses can include deductibles, copays, and coinsurance, and they vary depending on the insurance plan and the type of care received. Out-of-pocket costs can be significantly higher when using out-of-network providers, and some plans do not cover out-of-network care at all unless it is an emergency. It is important to understand out-of-pocket medical expenses to choose the right coverage and budget for healthcare costs to avoid unexpected bills. There are also out-of-pocket maximums or limits set by law, after which the insurance company covers all costs for the rest of the plan year.

| Characteristics | Values |

|---|---|

| Definition | Out-of-pocket expenses are costs that an individual is responsible for paying and that may or may not be reimbursed later. |

| Application | The term is used in health insurance policies to refer to the portion of a medical cost that the insurance company doesn't cover. |

| Examples | Deductibles, copays, and coinsurance. |

| Out-of-pocket maximum | Health insurance plans have out-of-pocket maximums that are set by federal law. These are caps on the amount of money that a policyholder must spend each year on healthcare expenses. |

| Non-ACA plans | With the changes in the health insurance industry, there could be non-ACA plans that do not meet the same standards. |

| Individual and family out-of-pocket maximums | Health plans that cover more than one person often have individual out-of-pocket maximums, as well as a family out-of-pocket maximum. |

| Out-of-network care | Out-of-pocket costs can be considerably higher when using out-of-network providers. Some plans do not cover out-of-network care at all unless it is an emergency situation. |

| Plan year | The 12 months between the date your coverage is effective and the date your coverage ends. |

| Out-of-pocket costs in 2024 | For 2024, the maximum out-of-pocket for an individual is $9,450, and for a family, it's $18,900. |

| Out-of-pocket costs in 2025 | For 2025, the maximum out-of-pocket for an individual is $9,200, and for a family, it's $18,400. |

Explore related products

What You'll Learn

- Out-of-pocket expenses include deductibles, copayments, and coinsurance

- Out-of-pocket costs are higher for out-of-network providers

- Out-of-pocket expenses are typically reimbursed by employers for work-related expenses

- Out-of-pocket maximums are set by federal law and vary by plan

- Out-of-pocket costs for Medicare in 2025 include Part A, Part B, and Part D

![]()

Out-of-pocket expenses include deductibles, copayments, and coinsurance

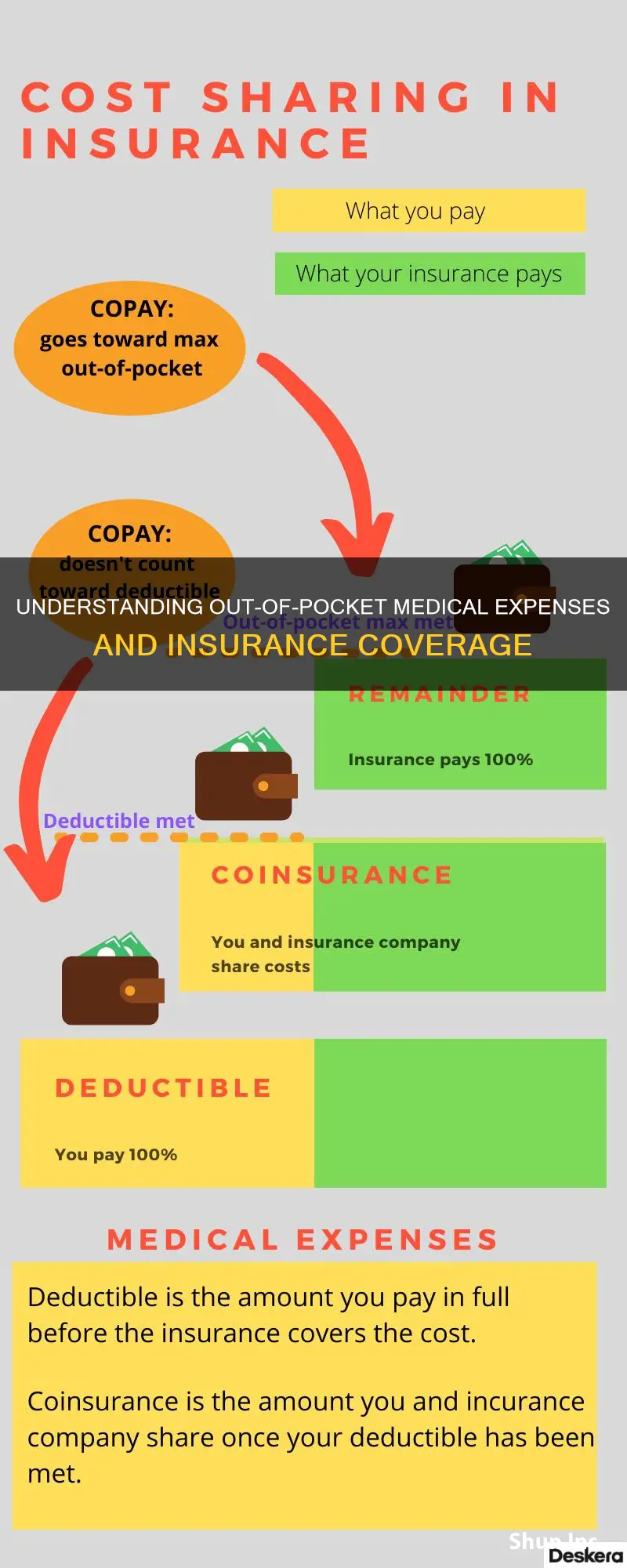

Out-of-pocket expenses refer to the portion of covered medical expenses that you can expect to pay during a plan year. These costs are typically for in-network services deemed essential health benefits. Out-of-pocket costs can include deductibles, copayments, and coinsurance.

A deductible is the amount you pay each year for eligible medical services or medications before your health plan begins to share in the cost of covered services. For example, if you have a $2,000 yearly deductible, you'll need to pay the first $2,000 of your total eligible medical costs before your plan helps to pay.

A copayment, or copay, is a fixed amount you may pay for a covered health care service, usually at the time you receive the service. Copay amounts can vary depending on the provider and service. With health plans that have copays, you’ll know exactly what you have to pay ahead of time, which can help you budget your health care costs.

Coinsurance is a percentage of the cost of a covered service. Until you reach your deductible, you’ll pay 100% of out-of-pocket costs. After you meet your deductible, you and your insurance company each pay a share of the costs that add up to 100%. Typical coinsurance ranges from 20% to 40% for the member, with the health plan paying the rest.

The out-of-pocket maximum is the highest amount of money you could pay during a 12-month coverage period for your share of the costs of covered services. Once you reach this limit, you will not be responsible for cost-sharing on covered services for the rest of the year.

Adding Dependents to Your Medical Insurance: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Out-of-pocket costs are higher for out-of-network providers

Out-of-pocket costs refer to the portion of covered medical expenses that a patient can expect to pay during a plan year. These costs can include a combination of a health plan's deductible, copays, and coinsurance for any covered, in-network services.

Out-of-pocket costs are generally higher for out-of-network providers. Out-of-network doctors or facilities have no contractual obligation to accept discounted rates for services covered under a health plan and can, therefore, charge full price. This is usually much higher than the in-network discounted rate. As a result, out-of-pocket costs can be considerably higher for out-of-network providers, and on some plans, they are double the in-network limits. In other cases, out-of-pocket costs can be unlimited for out-of-network providers.

It is important to note that there are no regulations in place to cap how much individuals spend on out-of-network care, and insurers are not required to cover services that are not considered essential health benefits. While emergency services are typically covered, eligible out-of-network emergency services are covered at the in-network benefit level.

To save on out-of-pocket costs, it is advisable to visit in-network providers. Most health plans provide access to a network of doctors, facilities, and pharmacies that offer discounted rates. By choosing in-network providers, individuals can keep their out-of-pocket expenses within the stated limits and avoid unexpected medical bills.

The out-of-pocket maximum, also known as the out-of-pocket limit, is the most a health insurance policyholder will pay each year for covered healthcare expenses. Once this limit is reached, the health plan will cover 100% of the remaining qualified expenses for the rest of the plan year. It is important to note that out-of-pocket costs for out-of-network providers may not be applied to the out-of-pocket maximum.

Canceling Medical Insurance: A Step-by-Step Guide to Policy Termination

You may want to see also

Explore related products

![]()

Out-of-pocket expenses are typically reimbursed by employers for work-related expenses

Out-of-pocket expenses refer to the portion of covered medical expenses that someone has to pay during a plan year. These costs can include a combination of a health plan's deductible, copays, and coinsurance for any covered, in-network services. The monthly premiums paid to have coverage are not included in out-of-pocket costs. Out-of-pocket costs can be significantly higher when using out-of-network providers, and some plans do not cover out-of-network care unless it is an emergency.

In the context of employment, out-of-pocket expenses refer to any business expenses incurred by an employee that are not reimbursed by their employer. These can include costs related to business travel, meals with clients, hotel rooms for business trips, office supplies, and transportation to work conferences. While some employees may be happy to use their own credit cards for work-related expenses, provided they are reimbursed promptly, others may feel financially strained and undervalued by their employer. This can lead to low employee engagement and even turnover.

To avoid placing a financial burden on employees, many companies provide company credit cards or implement expense reimbursement policies. Employees can submit expense reports to be reimbursed for their out-of-pocket expenses, and these reimbursed expenses can be claimed as deductions on business tax returns. This also provides a more accurate view of the company's financial operations and profitability.

However, some employers may stall or dismiss reimbursement requests, which can be challenging for employees, especially if they have incurred substantial expenses. In such cases, employees may need to advocate for themselves and seek support to ensure they receive the reimbursements owed to them.

Understanding Short-Term Medical Insurance Coverage Options

You may want to see also

Explore related products

![]()

Out-of-pocket maximums are set by federal law and vary by plan

Out-of-pocket expenses refer to the portion of covered medical expenses that you are expected to pay during a plan year. These typically include in-network costs for essential health benefits, such as medical services, prescription drugs, and medical supplies. Deductibles, copayments, and coinsurance for in-network care also count towards your out-of-pocket expenses. However, it is important to note that out-of-network care is not regulated by these caps, and insurers are not obligated to cover non-essential health benefits.

Out-of-pocket maximums, also known as out-of-pocket limits, are the most you will have to pay per year for covered healthcare services. Once you reach this limit, your health insurance plan will cover 100% of your qualified healthcare expenses for the remainder of the year. These maximums are set to help individuals and families avoid financial hardship due to high healthcare costs in years when they require extensive treatment.

Federal law establishes the highest out-of-pocket maximum that health insurance plans can impose, and these limits change annually. For example, in 2022, the federal maximum out-of-pocket limit for an individual was $8,700, while for a family, it was $17,400. However, it's important to note that these limits apply to non-Medicare and non-Medicaid health insurance plans.

While federal law sets the upper limit, health insurance plans can set their own out-of-pocket maximums within these constraints. For instance, the 2025 out-of-pocket maximum for an individual is $9,200, and for multiple family members on the same plan, it is $18,400. Additionally, HSA-qualified high-deductible health plans often have lower out-of-pocket maximums, such as $8,300 for an individual and $16,600 for a family in 2025.

The out-of-pocket maximums can vary based on the type of plan and the income of the enrollee. For example, the ACA's maximum out-of-pocket limit for non-grandfathered private health plans is projected to be $12,500 for single coverage in 2030. In contrast, the maximum out-of-pocket limit for HSA-qualified plans is expected to be $8,750 for single coverage in the same year. Furthermore, cost-sharing reductions based on income can result in lower out-of-pocket maximums for eligible enrollees who select specific plans, such as silver-level plans.

Get Medical Insurance in Florida: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Out-of-pocket costs for Medicare in 2025 include Part A, Part B, and Part D

Out-of-pocket costs refer to the portion of covered medical expenses that you're expected to pay during a plan year. These costs can include a combination of your health plan's deductible, copays, and coinsurance for any covered, in-network services. Typically, the monthly premiums you pay for coverage are not included in out-of-pocket costs. If you use out-of-network providers, your out-of-pocket costs can be significantly higher or even unlimited, depending on your plan.

In the context of Medicare in 2025, out-of-pocket costs will vary depending on whether you have Part A, Part B, or Part D. Here's a breakdown of each part:

Part A (Hospital Insurance):

Most individuals don't pay a premium for Part A due to their work history and Social Security tax payments. However, if you don't qualify for premium-free Part A, you may pay up to $518 monthly in premiums. For a hospital stay in 2025, there's a $1,676 deductible per benefit period. This covers the beneficiary's share of costs for the first 60 days of inpatient hospital care. For days 61-90, the coinsurance amount is $419 per day, and for lifetime reserve days, it's $838 per day.

Part B (Medical Insurance):

The standard monthly premium for Part B in 2025 is $185, with an annual deductible of $257. The Part B coinsurance is 20% of the cost for each Medicare-approved service or item, which can be a significant portion of your out-of-pocket costs.

Part C (Medicare Advantage):

Part C plans cover everything original Medicare covers and often provide extra benefits like dental, hearing, and vision care. The average monthly premium for Part C in 2025 is projected to range from $0 to over $240. Most plans have cost-sharing in the form of a fixed co-payment for doctor's visits.

Part D (Prescription Drug Coverage):

Annual premiums for Part D plans vary and are estimated to average around $46.50 per month in 2025 for standard coverage. The deductible can be up to $590 per year. In 2025, the coverage gap will be eliminated, and annual out-of-pocket costs are capped at $2,000. After reaching this limit, you pay nothing for covered drugs for the rest of the year.

Medical Evacuation Insurance: Your Essential Travel Companion

You may want to see also

Frequently asked questions

Out-of-pocket expenses in medical insurance are costs that the policyholder must pay for a service or item that their health insurance plan doesn't cover. These expenses may include deductibles, copays, and coinsurance.

The out-of-pocket maximum is a cap or limit on the amount of money a policyholder must pay for covered health care services in a plan year. Once the policyholder reaches this limit, the insurance company will pay 100% of all covered health care costs for the rest of the plan year.

Common out-of-pocket expenses include deductibles, copayments, and coinsurance. Deductibles are the amount a policyholder pays each year for covered costs before insurance coverage kicks in. Copayments are fixed amounts that a policyholder must pay for a covered service at the time of purchase. Coinsurance is the percentage of the cost that the policyholder pays, with the insurance company paying the rest.

![Receipt Organizer Envelopes. 3-Way Organizers that Store Receipts, Track Expenses & Let You Find Receipts Fast. Includes an Expense Ledger + Mileage Log. 12 Pack. [6.5x9.5"] Made in USA.](https://m.media-amazon.com/images/I/71crDiqBzUL._AC_UL320_.jpg)